Why Stablecoins Are Better Than Bank Money

Nine or ten years ago, most crypto enthusiasts had no idea why stablecoins even existed. Back when Ethereum was gaining traction, I remember a post on a forum that captured the general confusion perfectly: “I sold ETH on Poloniex and got some weird dollars with a ‘T’ at the end. What am I supposed to do with them?”

Those “weird dollars” turned out to be USDT. Like many others back then, the author saw them as a pointless layer between crypto and real money — and not just pointless, but inconvenient. Bitcoin and Ether were liquid enough; you could easily find a buyer for either. But what on earth could you do with USDT once you had it?

I remember someone in that thread suggesting the obvious workaround: just trade the tokens back for ETH or BTC and then transfer your crypto to an exchange that supports fiat withdrawals.

A lot has changed since then. The combined market capitalization of stablecoins recently crossed $300 billion, and — more importantly — it keeps growing. That means users aren’t cashing out of stablecoins; they’re putting more money into them. Around the world, many people now prefer to sell crypto for stablecoins rather than for traditional electronic money.

So what makes stablecoins better than ordinary dollars in your bank account?

The Independence of Stablecoins From Their Collateral

When you keep money in a bank, you don’t actually own that money. What you really have is a promise from the bank to give it back to you — someday. And the more money you keep there, the more you start to realize how fragile that promise is. Everyone knows about fractional reserve banking: the simple truth that no bank ever holds all the money it owes to its customers.

Banks are masters at finding excuses not to give your funds back, and regulators often help them. “Anti-money-laundering measures,” withdrawal limits, endless verification — all designed to make it nearly impossible to take out a large sum.

At first glance, stablecoins look even worse. When you swap fiat money for a stablecoin, your cash ends up in the hands of the issuer — Tether, Circle, or someone else. The bank no longer owes you that money; it owes them. Instead of one entity that might refuse to give your money back, you’ve added a second — the stablecoin issuer — who might do exactly the same thing.

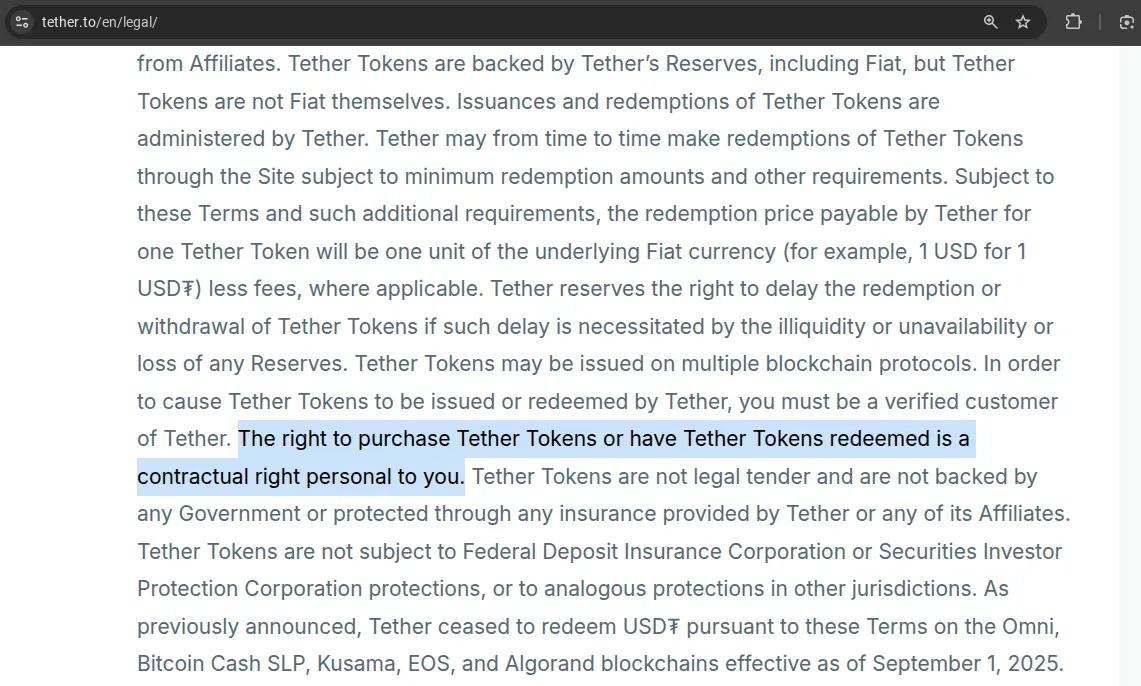

But in reality, almost no one ever buys stablecoins directly from the issuer. If you bought USDT with fiat, you probably got it from another user, not from Tether itself. And when you did, no “claim” to the dollars behind those tokens was transferred to you. Tether’s own terms say it clearly: only verified customers who signed a contract with Tether Limited have the right to redeem USDT for dollars. If you didn’t go through that process, Tether owes you nothing.

Circle’s rules for USDC are even stricter — you need to be a verified legal entity with an approved compliance profile.

And yet, nobody seems to care. Most people treat stablecoins not as “claims” on fiat, but as independent financial assets in their own right — something that holds value simply because everyone agrees it does.

It’s a bit like Somalia in the 1990s: when the government collapsed, the Somali shilling kept circulating for years. People kept using it, not because it was backed by anything, but because everyone agreed to keep accepting it.

1 USDT = 1 USD not because someone must give you a dollar for it, but because the market is full of people willing to do so. That’s the only backing that really matters.

USDC isn’t much different. And with crypto-collateralized stablecoins (for example, USDS — the successor to DAI), there isn’t a legally obligated counterparty at all. On the contrary, everyone involved in writing the smart contracts or running the protocol interfaces publicly disclaims any obligations.

Given that, you can look at stablecoins independently of their backing. From that angle, a lot of their advantages over ordinary bank money come into focus.

Fewer Freezes and Restrictions

At first, stablecoins might seem to increase the risk of getting your money frozen:

- The stablecoin issuer could block your wallet.

- Your bank could freeze funds you got from selling stablecoins (or other crypto).

- And regulators could shut down the bank itself — taking your assets down with it.

It seems that without stablecoins, you’re left with only the last two risks on that list.

But that logic only applies if you see stablecoins as a temporary stop before converting back to fiat. If you use them instead to avoid the banking system, the picture flips entirely. In that case, stablecoins remove two of those three risks — no bank to freeze your funds, no government to seize them.

In practice, the risk of a wallet freeze from Tether or Circle is far lower than the risk of your bank locking your account “for compliance reasons.” Stories about banks refusing to release funds are everywhere online; cases of stablecoin issuers freezing wallets are far rarer.

Besides, some stablecoins don’t even include a freeze function in their smart contracts at all — meaning the issuer literally can’t block your tokens. Examples include:

- USDT on the Liquid network

- USDT0 on Polygon and BNB Chain

- DAI

- Liquity USD

- FRAX

- and several smaller stablecoins like crvUSD, Freedom Dollar, and Ducat

Higher Yields

Money in the bank can earn interest — because the bank lends it out, trades currencies, and runs other licensed financial operations. Stablecoins let you do the same things without banks, licenses, or intermediaries.

People choose stablecoins because they make it possible to earn income on savings that would otherwise just sit still in a bank account. Of course, you can’t just keep them idle in your wallet — to get yield, you have to put them into DeFi protocols. There, lending, liquidity pools, and automated strategies all work without middlemen or regulatory overhead. That structural simplicity — no bank, no licensing, no permission — is what makes DeFi yields naturally higher.

In other words, stablecoins shift the margin that used to go to the financial system back to the user.

24/7 Access

Imagine it’s Saturday night, crypto prices start moving fast, and you want to buy in. If your funds are in a bank, good luck — large transactions outside business hours are either impossible or delayed “for security checks.” Even online banking systems aren’t truly 24/7 when it comes to significant sums.

With stablecoins, it’s different. You can go to rabbit.io, trade any amount, and the swap will settle instantly — wallet to wallet.

- Tens of thousands of dollars? No problem.

- Hundreds of thousands? Happens all the time.

- Need to move even more? We can handle that too.

No waiting for business hours. Just crypto-speed finance, anytime, anywhere.

Fast and Low-Cost Transactions

In many countries, for example in the United States, banking infrastructure is still slow and outdated. A wire transfer can take several business days. For businesses, that delay can mean missed opportunities and frozen cash flow. Stablecoins solve this instantly: any transfer takes seconds, costs a fraction of a cent, and works 24/7.

In Europe, where SEPA has long made transfers fast and reliable, this is far less relevant, which is why stablecoins are much less prevalent there. But in the Americas, Africa, and parts of Asia, stablecoins offer a real competitive edge — they make everyday business payments faster, simpler, and cheaper than banks ever could.

This is especially true for cross-border payments. Traditional international transfers are not only slow but also expensive — weighed down by correspondent banks and compliance checks. Yes, you could use Bitcoin or another cryptocurrency for that, since they’re also borderless and fast. But global commerce still runs on the U.S. dollar, and it’s far more convenient when your payment token tracks that same unit of account. That’s exactly what most stablecoins do: they give you crypto speed with dollar familiarity.

Programmability

In a way, stablecoins are similar to central bank digital currencies (CBDCs). Some governments are already experimenting with or rolling out such systems — mostly because programmable money gives them the ability to impose strict controls on how funds can be spent. For example, a government could issue welfare payments that can’t be used to buy alcohol or lottery tickets.

Stablecoins, however, open the door to the opposite idea — programming money to limit the state, not the citizen. In theory, taxpayers could use smart contracts to make sure their money is spent only on causes they support. Imagine paying taxes in stablecoins and placing them into a contract that defines a whitelist of recipients — hospitals, schools, or NGOs you personally trust. The government could then allocate funds only within those approved categories.

Of course, this is still closer to science fiction than financial reality. But it illustrates one of the key differences between bank money and stablecoins: the latter are programmable by their users, not only by institutions.

Conclusion

The advantages of stablecoins over traditional bank money are already hard to ignore. It’s no surprise that for many crypto users today, stablecoins have become a full-fledged alternative to withdrawing funds into the banking system.

Of course, to see their real value, you have to stop thinking of them as “promises” from issuers to redeem tokens for fiat. Instead, think of them as digital assets that maintain value because the market collectively treats them as such. As long as there’s enough liquidity and demand, you’ll always find someone willing to buy your stablecoins at face value. If that demand ever dries up, the question of “backing” will suddenly matter again — and not everyone will be able to redeem what’s supposedly behind those tokens.

But then again, isn’t that true for fiat currencies too? Anyone who spent their national currency fifteen years ago got more value from it than those spending it today — and those who wait another fifteen years will get even less. In a financial collapse, the last person holding their country’s currency ends up with nothing. By that logic, the entire fiat system is just another kind of pyramid.

And yet, history gives us counterexamples. Somalia’s shilling survived the collapse of its state in the 1990s because the free market — not the government — sustained its value. Maybe stablecoins will follow a similar path: money accepted freely by users, not imposed by states. It would be poetic if, someday, the U.S. dollar disappears — but the stablecoins pegged to it remain, still powering the decentralized economy.