Who Pays for Crypto Staking and Why?

Two days ago, Uphold announced plans to introduce XRP staking on the Flare Network. Some saw this as a promising opportunity to earn extra passive income from XRP, while others wondered:

- How is staking yield actually generated?

- Who’s willing to pay us just for locking up our assets?

- And does this really benefit the people who foot the bill?

I’m the kind of person who always digs deeper and tries to find real answers. And by 2025, there’s already been plenty of evidence — both transparent examples of how staking generates honest yield, and cautionary tales of promised returns that turned out to be illusions. So let’s break down exactly how stakers get paid in different models and who ultimately funds the party.

Proof-of-Stake: Rewards from Fees and Coin Issuance

Fees

The most straightforward case is staking in a Proof-of-Stake (PoS) blockchain. If no one locks up their coins, the blockchain simply doesn’t work. No transactions would ever get recorded, because you need validators to approve new blocks, and, in PoS systems, validators are those who stake their crypto as collateral to prove they’re acting in good faith when they help create blocks. If they’re caught acting dishonestly or stop doing their job, they risk losing part or all of their staked funds.

So, in PoS blockchains, the answers to those fundamental questions are pretty clear:

- The yield comes from transaction fees paid by users.

- Stakers aren’t being paid just for locking up coins — they’re paid for securing the network and creating new blocks. The locked coins are simply collateral to keep validators honest and ensure the network keeps running smoothly.

- Users pay those fees, because it’s the only way for them to move assets and interact with smart contracts on the blockchain.

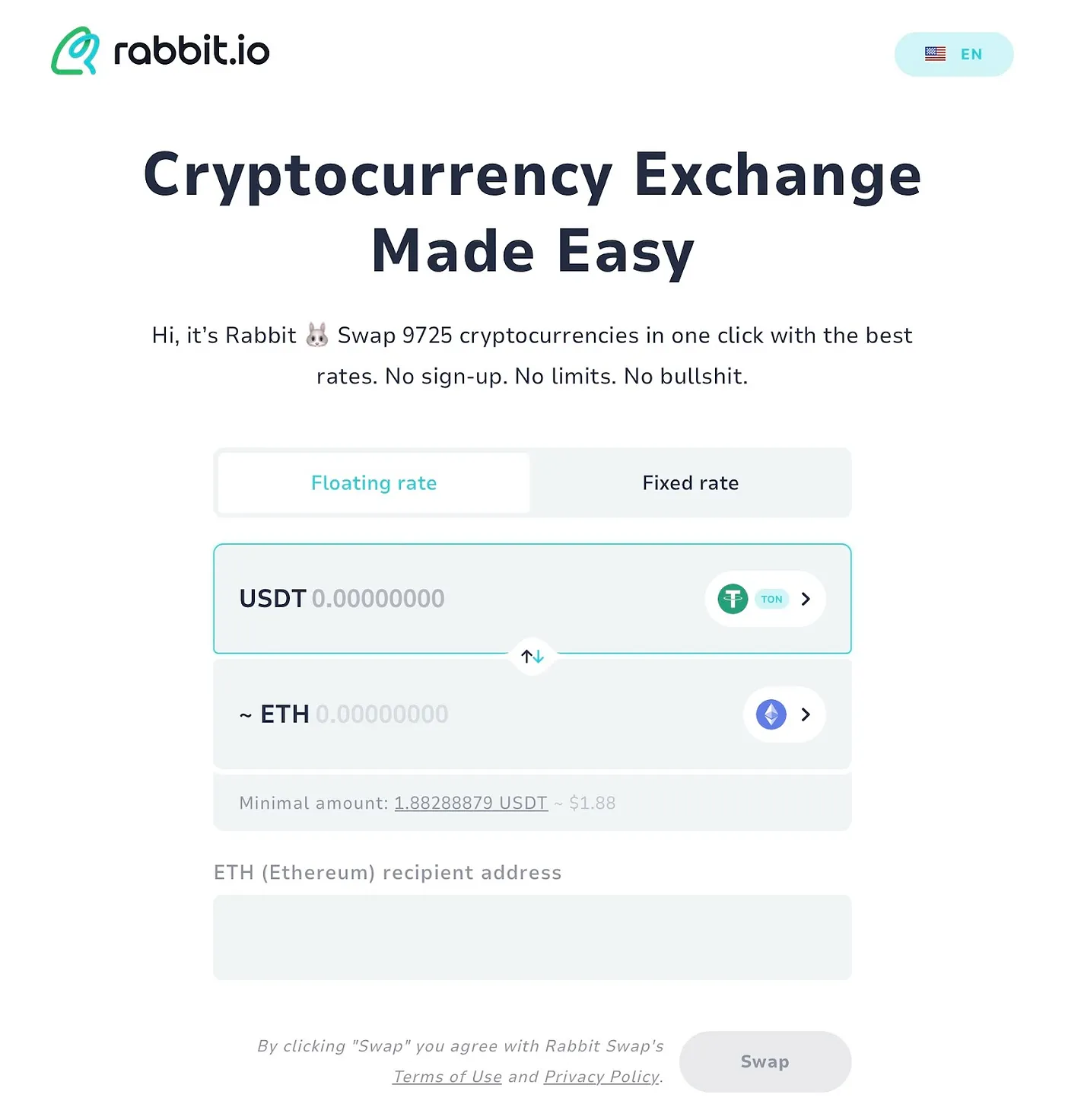

And people really are willing to pay. I see it firsthand in our crypto swapping service, rabbit.io, where users sometimes exchange very small amounts.

Why would someone need just $1.88 worth of ETH? But those kinds of transactions happen. It usually means our client simply needed a bit of ETH to cover gas fees on the Ethereum network — and they’re willing to buy that ETH just to pay the stakers who keep the network running.

In short, blockchains like Ethereum show that staking has real value. There are users who genuinely benefit from paying those fees because staking keeps the entire system up.

Coin Issuance

But there’s another important factor to consider. In many PoS networks, staking rewards come not just from transaction fees, but also from inflation — that is, the protocol itself mints new coins and distributes them to stakers based on how much they’ve committed.

Of course, these new coins don’t come out of thin air without consequences. When the protocol mints new coins, it effectively dilutes the holdings of everyone else. So, if you’re staking, you’re getting your share of this new issuance and either preserving or even growing your slice of the total supply. But if you’re not staking, you’re slowly losing ground as your share of the overall supply shrinks due to inflation.

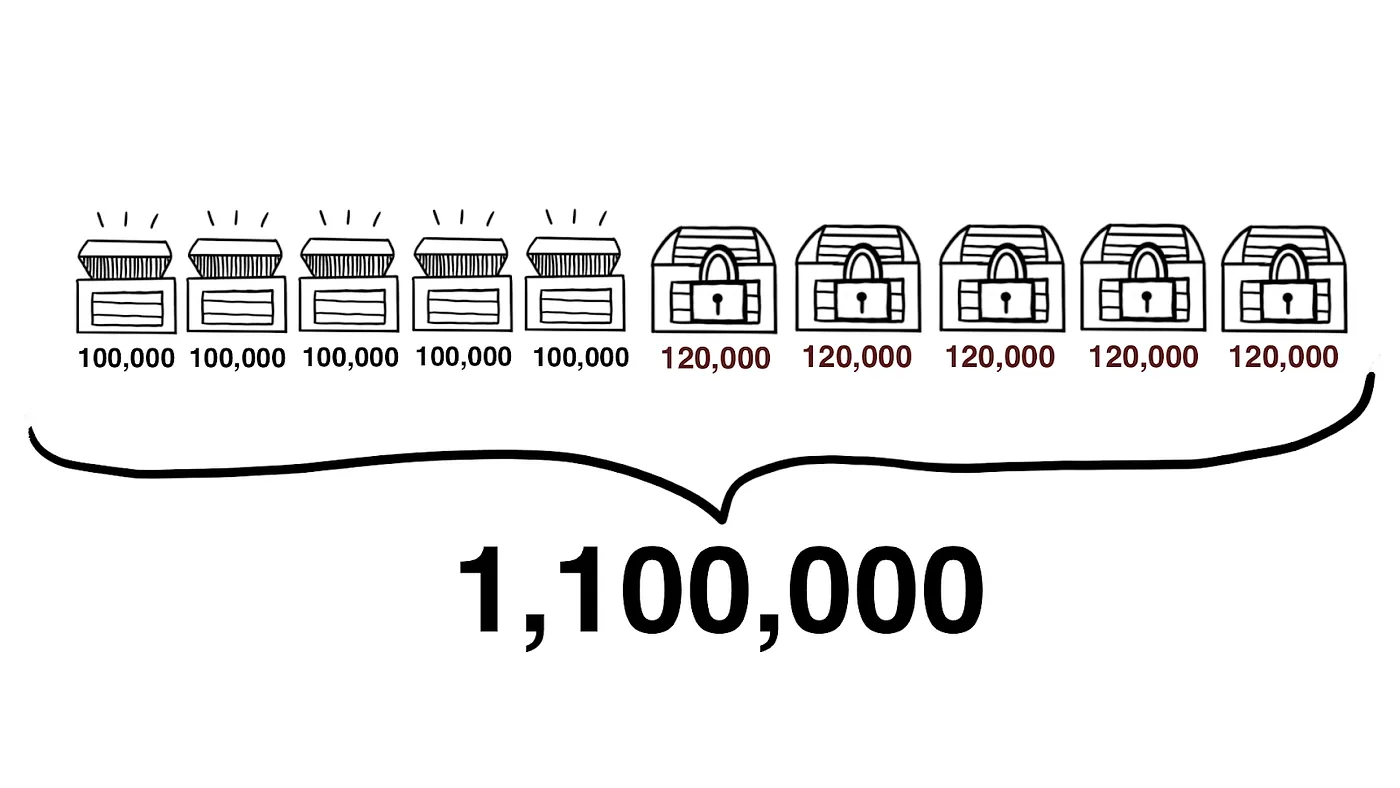

Imagine a network with a total supply of one million coins, evenly split among ten holders. Each of them controls exactly one-tenth of the total. But five of these holders stake their coins, while the other five don’t.

A year later, the network has minted an additional 100,000 coins, and these new coins go exclusively to the stakers. Now:

- The total supply is 1,100,000 coins.

- Each staker holds 120,000 coins (about 11% of the total).

- Each non-staker still has 100,000 coins (but now it’s about 9% of the total).

In networks like this, not participating in staking isn’t just about missing out on rewards — it’s also about losing influence. Over time, a non-staker’s share of the total supply keeps shrinking, reducing not only their economic standing but also their power within the blockchain. Since validator privileges are usually proportional to the size of the stake, even if a non-staker eventually wants to become a validator, they’ll have less say in the network compared to those who staked early on.

So, when staking rewards come “out of thin air” through new token issuance, they also bring hidden costs. They’re paid by diluting everyone else’s holdings — and the choice of whether to stake or not can have long-term consequences for your standing in the ecosystem.

Platform-Based “Staking”: Yields from Other Sources

For stakers in PoS blockchains, the source of rewards is usually pretty clear: the protocol defines how much gets paid out, and anyone can see how many new coins are being issued or how much is collected in transaction fees. But in the world of centralized platforms that call their products “staking,” the mechanics can be completely different. Big exchanges like Binance and Coinbase do offer real PoS staking on behalf of their clients — they run validator nodes, collect the network rewards, and then share them with their users (after taking a cut, of course).

However, some platforms let users “stake” assets that don’t actually have any native staking in their underlying blockchain — like Bitcoin or stablecoins. In these cases, the platform isn’t really doing any staking at all. Instead, it’s running entirely different schemes behind the scenes, even if it’s easier to call them all “staking” in marketing materials.

Remember how things worked in the heyday of crypto lenders like Celsius, BlockFi, and Anchor Protocol before the 2022 meltdown? They took in user crypto deposits and promised returns. Celsius, for example, was making money from many sources: selling its own token, lending out crypto to borrowers, mining Bitcoin, and even speculative trading. Up to 80% of what it earned from all these activities, it promised to pay back to depositors as “interest.”

When there was real demand for their tokens (like CEL), plenty of borrowers willing to pay fees, healthy mining profits, and successful trades, the platforms could share these earnings with their users. But when any of those income streams dried up, the well ran dry — and users suddenly wanted to withdraw their crypto. To keep the illusion of high interest going, some platforms even dipped into their own reserves, paying users out of the company’s own pocket.

The problem got even worse because many platforms promised fixed interest rates no matter what was happening in the market. They had to keep those promises — until the model broke and the collapses began. Many people who had “staked” their crypto on these platforms in 2022 ended up losing it altogether.

Of course, not every centralized “staking” offer has turned out to be a scam. Many exchanges today still offer “staking” and reliably pay users. But in most cases, those payments come directly from the exchange’s own revenue. And that brings up the real question: why would an exchange even want to pay people for locking up their assets, when those locked assets aren’t adding to trading volume or liquidity?

To make this work, platforms have come up with all sorts of tricks.

- Some let you use staked tokens as collateral for borrowing — so you can earn staking rewards and still unlock some liquidity and trading activity.

- More recently, liquid staking has become popular: instead of holding locked tokens, you get a “liquid” token that can still be traded freely, while the original assets remain staked. These “liquid” tokens represent a claim on your locked assets.

Why all this complexity? Does it really make sense for an exchange to pay out staking yields? Maybe it’s just a trap.

- First, by promising passive income, the exchange gets access to the funds of crypto holders who might not be interested in trading at all. But once it’s gotten the client in the door, the exchange uses every opportunity to push them toward other products: first, seemingly passive options like copy-trading and trading bots, and then, step by step, into more and more active and risky trading. In the end, someone who only wanted to park their crypto for staking ends up as an active trader — and loses everything.

- Second, for active traders, staking can become a lure to use margin trading. If part of your funds are locked up, you may end up borrowing more to keep trading — and that adds a lot of risk. What was supposed to be “safe” passive income can turn into serious losses.

- And finally, why is an exchange so eager to have you keep your crypto locked up on their platform? Maybe it’s because your crypto isn’t really there anymore.

Ultimately, when you see “staking” on a trading platform, remember that the yield is really coming from the platform itself — and they’re paying it to get you hooked on their other products. If you just deposit your crypto, lock it up, and withdraw it later without ever using their other services, the exchange doesn’t really profit. So be careful with these kinds of “staking” offers!

DeFi Staking

In decentralized finance (DeFi), the term “staking” often refers to depositing your crypto assets into liquidity pools or lending pools. But keep in mind: your crypto in these scenarios isn’t just locked away — it’s actively used to provide financial services. If something goes wrong (like a smart contract bug or an economic flaw in the model), you risk losing part or even all of the assets you’ve staked. Interestingly, if a mistake happens, no one’s directly responsible for your crypto: after all, you haven’t entrusted it to a specific party, but neither have you kept full control over it.

Take Flare Networks, the platform Uphold intends to use for XRP staking. Flare is positioned as an “interoperable” blockchain, enabling smart contracts and DeFi operations for tokens like XRP, LTC, DOGE, and others that originally didn’t support such features. Staking on Flare typically involves depositing your crypto, often in the form of wrapped tokens (like FXRP), which are then used in DeFi protocols.

The source of yield in these setups is usually clear: it generally comes from fees paid by users of DeFi services. While not as stable or secure as traditional PoS staking, it’s still reasonably transparent and usually marketed without excessive hype. If you understand the risks and can handle potential losses, it might be worth participating.

However, remember the DeFi boom of 2020–2021, when countless new projects promised astronomical staking returns — hundreds or even thousands of percent annually. In most cases, those incredible APYs weren’t sustainable or backed by real economic value. Instead, the projects simply minted endless amounts of their own tokens, effectively paying users to hold and not sell. This worked fine as long as excitement kept bringing in new money, but eventually, the bubble burst. Those who didn’t exit early enough ended up holding worthless tokens. PancakeSwap, OlympusDAO, Wonderland, Iron Finance, SafeMoon, and many others became textbook examples: APYs as high as 80,000% evaporated as token values plummeted by 90–99% or more.

These stories clearly demonstrate that yields not backed by real economics (such as fees, demand for services, or genuine utility) inevitably turn into dust once the inflow of new funds dries up.

Transparency Above All

The main takeaway is this: staking yields never just magically appear out of nowhere — there’s always an economic source behind them, and it’s crucial to understand exactly what it is.

- In Proof-of-Stake networks, staking rewards come from one of two “wallets”: either directly from the network itself, through inflationary issuance that effectively dilutes all token holders, or from user wallets in the form of transaction fees that validators collect.

- With centralized platforms that advertise “staking,” the yield often involves shifting funds around among different user groups: essentially, interest paid to some users is financed by others — borrowers, margin traders — or directly by the platform out of its own earnings.

- In DeFi staking scenarios, risks can be high: today, you’re enjoying high returns, but tomorrow you might discover the smart contract has been broken or that the underlying economic model was fundamentally unsound.

This is why it’s essential to ask yourself the question, “Who’s really paying for this?” before committing your crypto to any staking scheme. Asking this helps you separate sustainable models — where someone genuinely benefits from paying you, and you’re comfortable with why they’re doing so — from schemes propped up only by hype, untested ideas, and other people’s money.