What Is Really Behind the DeFi TVL Drop?

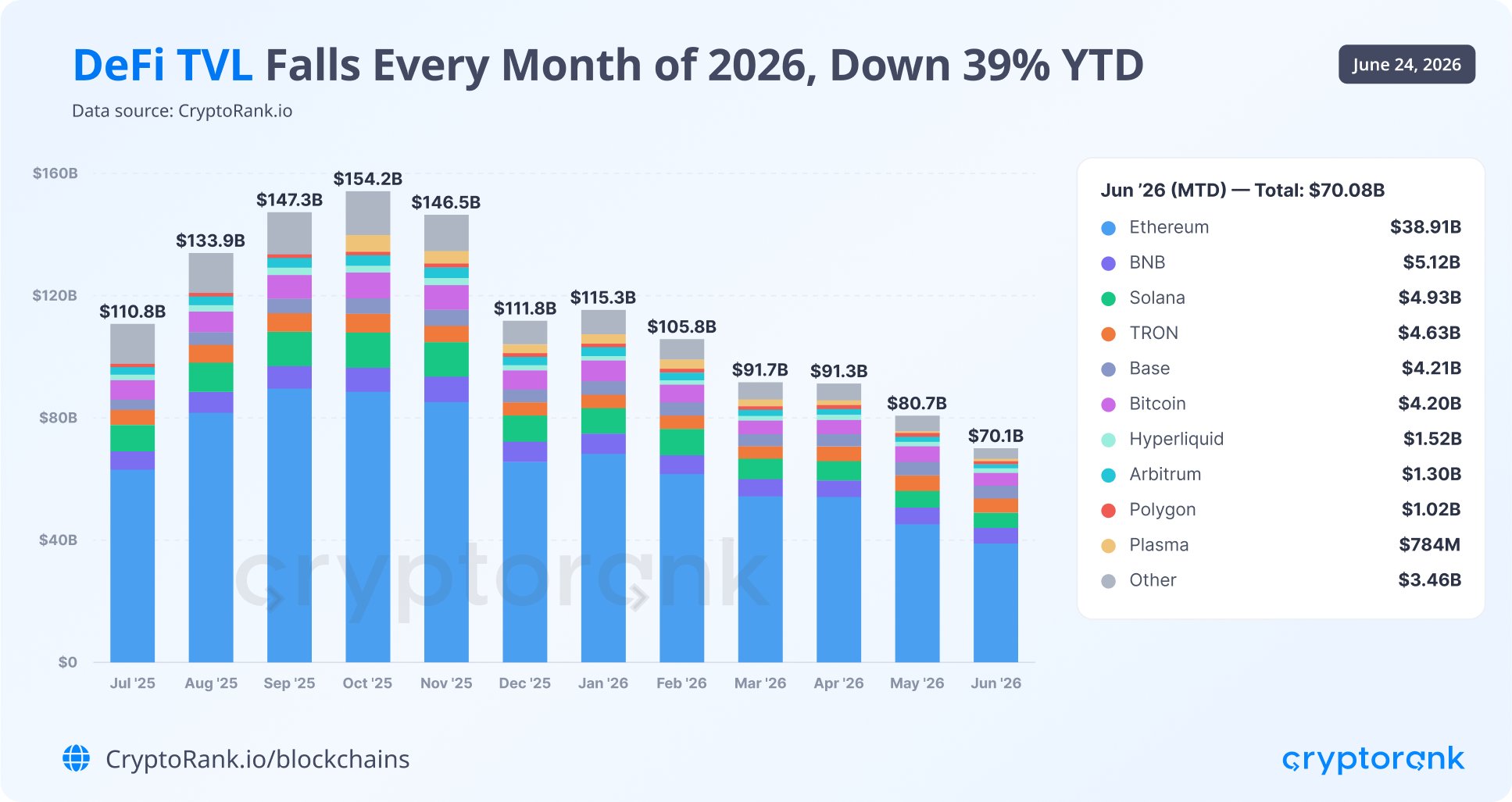

This week, CryptoRank reported that the total value locked in DeFi protocols has fallen by nearly 40% since the start of the year.

When I saw those numbers, my first thought was that the outflow made sense. Given the wave of hacks and asset thefts we have seen in DeFi projects over the past few months, it is hardly surprising that users would start pulling their capital out.

But CryptoRank itself sees the decline differently. It attributes the drop to a broad crypto market correction, implying that assets are not actually being withdrawn from DeFi protocols - they are simply losing value.

I have believed since 2020-2021 - the first time DeFi broke into the mainstream - that DeFi works best with stablecoins. Putting volatile assets into DeFi just does not make sense: they can drop so sharply in price that the losses eat up any expected yield, and then some.

So CryptoRank's take struck me as questionable, and I decided to dig into what is actually going on: what is behind the TVL decline, and where did that 40% of capital go?

What DeFi Protocols Actually Hold

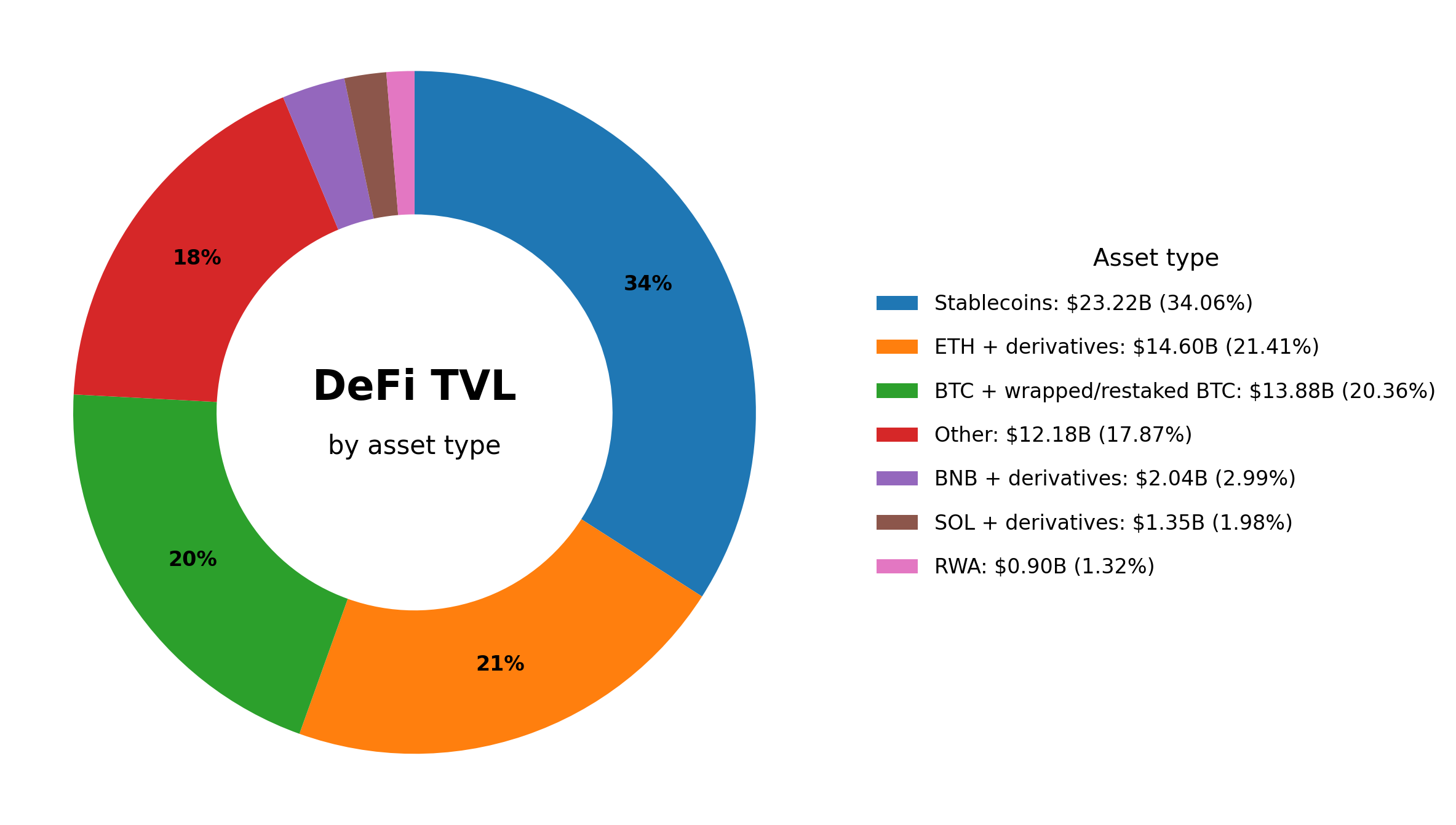

Most DeFi analysts rely on DeFiLlama for their data, so I went there too. The site itself does not display a breakdown of TVL by token, but the public API gives enough data to reconstruct a close approximation.

I queried how many of each token are locked across DeFiLlama-tracked protocols, summed the amounts across protocols for each token, multiplied them by current prices, and grouped everything into categories. Here is what I got:

- Stablecoins: $23.22B (34.06%)

- ETH + derivatives (LST/LRT): $14.60B (21.41%)

- BTC + wrapped/restaked BTC: $13.88B (20.36%)

- BNB + derivatives: $2.04B (2.99%)

- SOL + derivatives: $1.35B (1.98%)

- RWA: $0.90B (1.32%)

- Other (tokens individually too small to track separately): $12.18B (17.87%)

Stablecoins lead with 34%, while purely speculative coins rarely even reach 1% on their own, so I swept them all into the "Other" bucket. This partly confirms my longstanding intuition: DeFi is primarily infrastructure for dollar-denominated capital, not an altcoin multiplier.

Another surprise: Bitcoin has nearly caught up with ETH in DeFi by volume - 20.36% versus 21.41%. Long-time readers know I have always assumed bitcoiners do not lock their savings in DeFi protocols. They self-custody. Yet it turns out that one in every five dollars locked in DeFi is sitting there as wrapped or restaked Bitcoin. And relative to Bitcoin's total market cap, the figure is not trivial either: more than 1% of all Bitcoin has made its way into DeFi.

The RWA category accounts for just 1.32% ($0.90B). But it is important to understand that this only covers what is directly locked inside traditional DeFi protocols as collateral or liquidity. The total tokenized real-world asset market on-chain is much larger. It just lives outside the DeFi perimeter.

This already gives us a way to estimate where the 39% TVL drop - from $115B in January to $70B in June - is coming from.

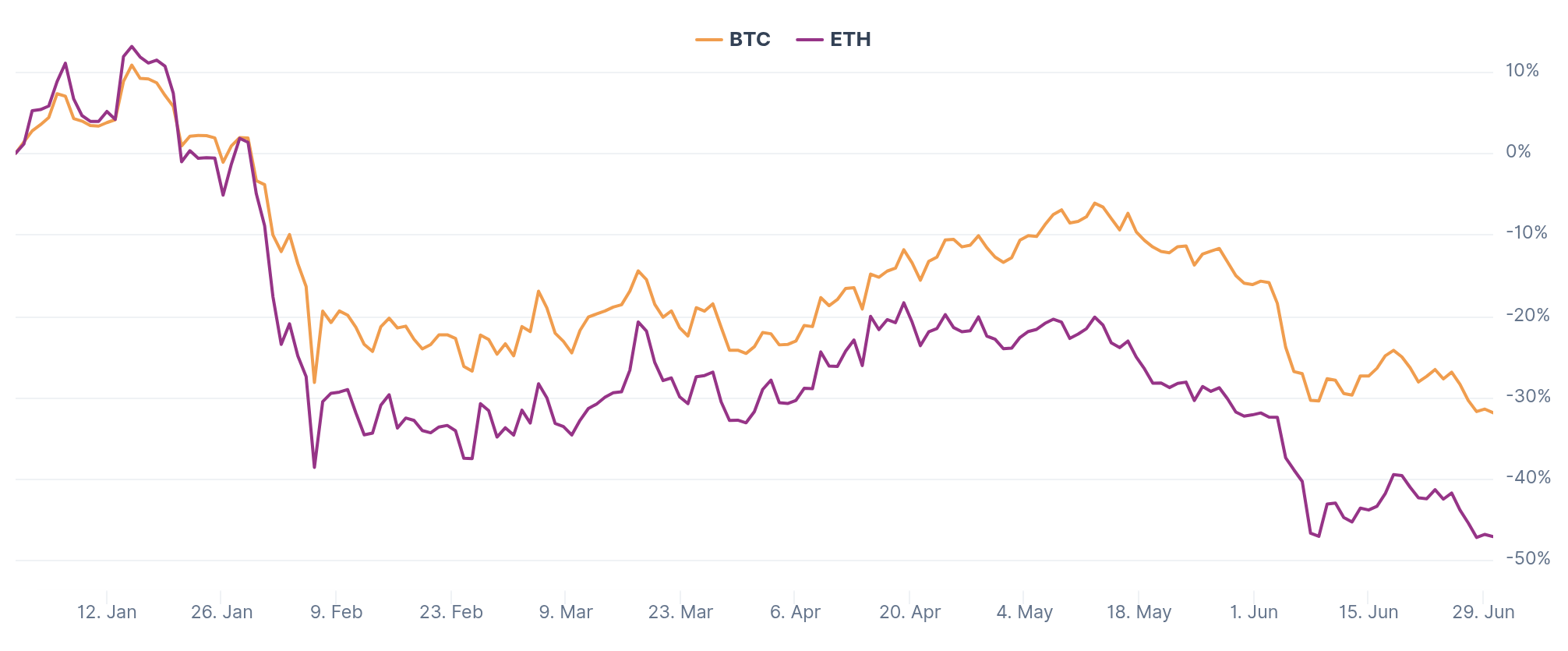

ETH and BTC together make up 41% of TVL, and both have dropped substantially in price. Since January 1, 2026, ETH has fallen roughly 47% and Bitcoin roughly 32%.

A rough calculation: if ETH and its derivatives accounted for around $24B of the starting $115B TVL, and BTC and its derivatives for $23B, then price declines alone would have cut the dollar value of those two categories by roughly $18B. That is about 16% of the starting TVL.

So price effects alone explain more than a third of the total decline. CryptoRank's emphasis on market correction as the primary driver is partially correct: plenty of people really do lock volatile crypto assets into DeFi protocols.

Who Keeps Crypto in DeFi, and Why

I used to assume DeFi attracted mostly yield hunters. But look closely at what DeFi users actually say about their strategies, and you find several distinct groups with very different motivations.

Stablecoin "parkers" are by far the largest group. For them, DeFi is a substitute for a bank deposit: no red tape, no demeaning compliance procedures, and no political risk attached to the banking system.

A significant share of stablecoin capital in DeFi is currently earning less than the yield on US Treasuries. In 2025-2026, T-bills have been paying 4.5-5.5% annually with no smart contract risk, while a typical stablecoin pool in Aave returns around 2-4%. So this group of DeFi "depositors" is now largely made up of people who do not have access to mainstream investment instruments.

Earning 3-5% annually in USDC/USDT through Aave, Morpho, or Sky is genuinely attractive for people in countries like Nigeria, Turkey, Russia, and much of Latin America and Asia. According to Standard Chartered, residents and businesses in emerging markets already hold around $173 billion in dollar stablecoins, using them as a substitute for a USD account outside the local banking system.

Traders - particularly in derivatives markets - are the second most significant category. The thing is, DeFiLlama classifies as DeFi many platforms that are actually run centrally and keep full control - either directly or through custodians - over user-deposited assets, issuing wrapped tokens on their own chains in return. Hyperliquid is one example: it grew its TVL by around 7% in 2026, bucking the broader trend. If platforms like this were excluded, the DeFi TVL decline would look considerably steeper.

Recursive borrowers make up another important segment. These users treat DeFi as a loop: deposit ETH, borrow stablecoins against it, buy more ETH, deposit that too, and repeat. One important slice of Aave's lending activity follows this pattern: users post stETH/wstETH as collateral, borrow ETH or stablecoins, and run the loop again, boosting yields while stacking liquidation risk. Similar dynamics play out around Ethena/sUSDe, where yield is tied to ETH staking and funding rates in derivatives markets. The result is that lending protocols can end up counting the same asset multiple times. When ETH drops in price, these loops unwind in a cascade.

Tax optimizers are a notable group, mostly wealthy crypto holders from developed countries. They have brought the "Buy, Borrow, Die" strategy into DeFi: deposit BTC into a protocol and borrow stablecoins against it for living expenses. No capital gains tax is triggered because a loan is not income. It is a perfectly legal strategy, and it keeps large amounts of capital in DeFi more reliably than any APY could. I suspect this accounts for a meaningful chunk of the BTC sitting in DeFi protocols.

Institutions deserve a mention too - not because they are a significant presence, but precisely because they are absent, and that absence shapes the DeFi landscape in its own way. The infrastructure for institutional players is already built, but nobody is using it. Aave Arc, Aave's flagship institutional product, has accumulated a TVL of $50,000. Fifty thousand dollars.

All of these groups - institutions aside - genuinely seem to need DeFi, and their capital is unlikely to leave the decentralized finance space anytime soon.

Who Is Actually Pulling Money Out of DeFi

The obvious reasons for withdrawing assets have already been mentioned at the top: market decline and hacks. But there are three more groups with their own specific reasons for pulling out.

The first is the farming-fatigued. Many users have spent years locking capital in DeFi protocols chasing airdrops. Many received their tokens and found them worthless, while their capital had been sitting at risk the whole time, generating no meaningful yield. Katana's team captured this mood well when they wrote that users are not farming points - DeFi projects are farming users.

The second is those withdrawing from some protocols only to move into safer ones. This has been especially visible after the hacks of recent months.

The third is EU residents. I have not come across hard data showing DeFi protocols actively restricting access for European users. But recently, I wrote about how EU regulators have started scrutinizing services that present themselves as decentralized in their marketing while actually holding admin keys to all their smart contracts and bridges. Even if this has not hit European capital in those services yet, I am confident it will start flowing out soon due to regulatory uncertainty.

So Where Is the Money Going?

The 39% TVL decline appears to be the result of three distinct processes.

The first is the optical effect. ETH, BTC, and other assets have fallen in price, and their dollar value inside protocols has dropped with them. The capital has not gone anywhere. It is just worth less.

The second is the deflation of bubbles. Recursive debt, point farming, and restaking chains that artificially inflated TVL during the bull run have either become unprofitable or wiped out the users running those strategies. But this was never all real, unique capital in the first place. It was often the same asset counted multiple times in the metrics.

The third is genuine net outflow. And I think it is split across three destinations that everyone has been talking about lately:

- Tokenized real-world assets, many of which do not show up in DeFiLlama's TVL metric.

- AI stocks - a competitor for risk capital that did not exist at this scale in previous crypto cycles.

- Stablecoins outside of DeFi.

That last one deserves special attention. The total stablecoin supply today exceeds $314 billion, 50% more than a year ago. And yet the total value locked in DeFi has fallen. The reason is that stablecoins no longer need to be "parked." They can be used. More and more, they are being used in payment systems and cross-border transfers as real money.

At rabbit.io, we see the same trend in exchange flows: user interest in stablecoins keeps growing. People clearly know what to do with them. Otherwise, they would not be swapping other crypto assets into stablecoins at such a pace. And if people know where to use stablecoins, there is no longer much reason to "park" them.

So my initial instinct about hacks driving the outflow was only partially right: hacks may have accelerated something that would have happened anyway. But CryptoRank is only partly right as well: Bitcoin and ETH have dropped in price, but that does not explain the shrinkage of DeFi's stablecoin segment.