NFTs: Much More Than Just Collectibles

Recently, a user reached out to Rabbit Swap, our crypto exchange service, with a question: can we swap a non-fungible token (NFT)? At Rabbit Swap, we handle all sorts of crypto assets — from classics like BTC and XMR to stablecoins and more obscure tokens. But NFTs? No, we don’t support them.

But why not? After all, NFTs are also crypto assets! Strictly speaking, the only real difference between an NFT and, say, BTC is that there’s only one of each NFT, while there are 21 million bitcoins. We’ll happily exchange almost any obscure altcoin — so what makes NFTs so different?

That’s exactly what our client asked us. And honestly, these questions deserve a proper answer. Let’s dig in.

A Brief History of NFTs

Namecoin: Blockchain Names as the First NFTs

Many people call “Quantum,” a piece by artist Kevin McCoy, the very first NFT. It was registered on the Namecoin blockchain on May 2, 2014, with a transaction that included a hash of McCoy’s digital image.

I agree that Quantum deserves to be called the first NFT artwork. But I wouldn’t go so far as to call it the first NFT token — and here’s why.

Since 2011, the primary use case for Namecoin — the first widely recognized Bitcoin fork — has been registering unique names on the blockchain. Each name is a digital object with a clearly defined owner, who can transfer it to anyone else. In other words, all names registered in the Namecoin blockchain since 2011 are, in a very real sense, non-fungible tokens. The Namecoin community never used the term “NFT,” but from a technical standpoint, every name in the system is exactly that.

Before Quantum, most registered Namecoin names were .bit domains — a decentralized alternative to traditional domain names, designed so that no one could seize ownership from you. Unlike conventional domains, .bit addresses can’t be taken away by government order; whoever controls the private key for the blockchain address, controls the domain. To make your browser open these sites, you just need a special extension, like PeerName. Registering a .bit domain is as simple as sending a blockchain transaction. It’s basically the same minting process used by modern NFTs.

From the very start, Namecoin allowed you to register any string as a name — not just domain names. That could be a short poem, a personal pledge, or even a hash of a work of art — forever recorded on the blockchain. In theory, registering a hash as a blockchain name could have served as proof of authorship (or at least proof that you had the work before anyone else). But no one really used this feature until Kevin McCoy did it in 2014.

Colored Coins

Starting in 2012, Bitcoin developers began experimenting with “colored coins” — protocols that let you attach unique tags to individual bitcoins and transfer those tags from one address to another. This opened the door to creating digital objects on the blockchain that existed in a single, unique copy and whose ownership could be easily verified.

However, I couldn’t find any well-known examples of colored coin protocols being used to issue one-of-a-kind tokens. Enthusiasts mostly used colored coins to tokenize financial assets like fiat currencies, rather than to create something truly unique. At the time, nobody saw much practical value in tokenizing a one-of-one asset. The idea of unique colored coins came up in the protocol’s original whitepaper, in the context of “smart property” and collectibles, but as far as I can tell, it never moved beyond theory.

Given that unique colored coins were mentioned in the whitepaper introducing the technology, I suspect that someone (at the very least, the developers themselves) probably ran experiments of this kind — and somewhere in the Bitcoin blockchain, there may be an example of a unique colored coin issued before Quantum. But if there is, it never became widely known.

Standardized NFTs on Ethereum

One of the colored coin developers, Vitalik Buterin, took some of the ideas behind colored coins and built them into his new project: Ethereum. On Ethereum, non-fungible tokens quickly became a standardized part of the ecosystem. The platform made it easier than ever to create tokens, introduced universal standards for them, and allowed people to manage tokens through smart contracts. All of this helped popularize NFTs and inspired the public to find new ways to use the technology.

That’s when NFTs started to take on features that made them resemble cryptocurrencies. Most importantly, people began using them mainly for speculation. People bought NFTs on marketplaces, hoping to resell them later at a higher price. For those who discovered the technology during this period, NFTs became just another speculative asset class. That probably includes our client, who assumed you could exchange NFTs for crypto on rabbit.io.

But here’s the thing: in that context, NFTs are really just an illiquid form of cryptocurrency — a bit like the millions of meme tokens recently launched on Solana. Have you ever seen a “wanted” ad for an NFT on a marketplace? I never have — all I see are “for sale” listings.

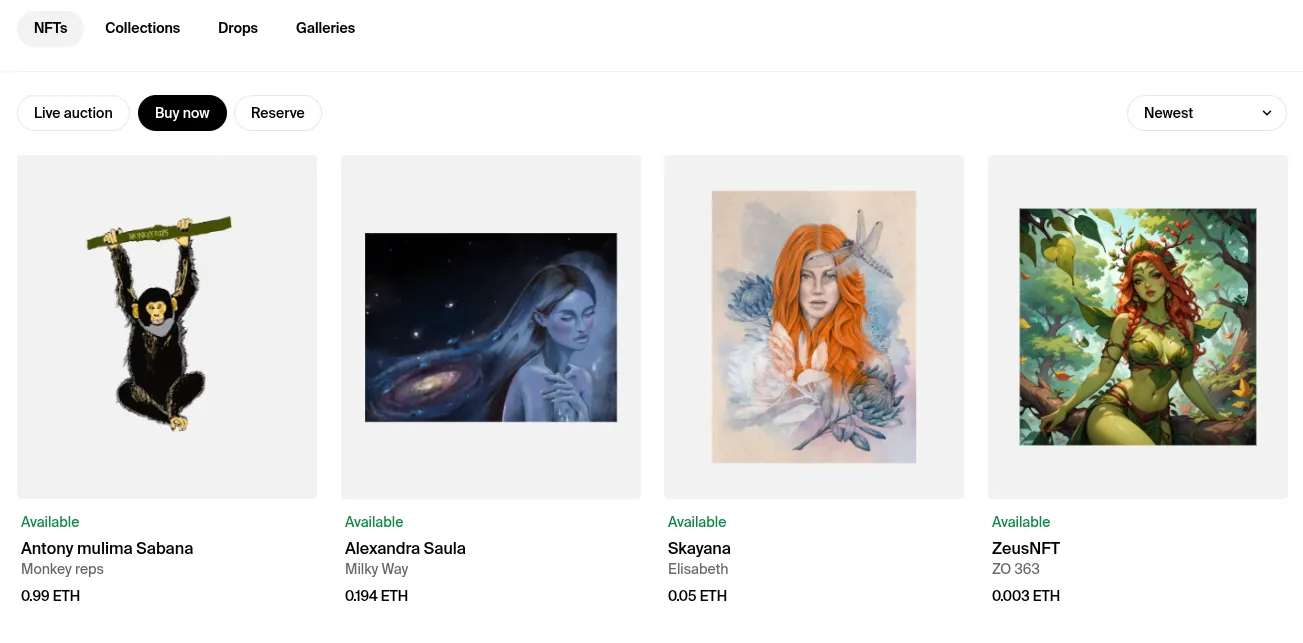

Screenshot: NFT marketplace Foundation.app

The price you see in those listings isn’t what you’d actually get for selling the token — it’s just what the seller wants someone to pay. Whether you can actually sell it, and at what price, is a completely different question.

NFTs, then, aren’t exactly a speculator’s dream. But NFTs have a much broader purpose — one that people rarely talk about.

What Are NFTs Actually Good For?

The fundamental property of an NFT is its authenticity — it can’t be faked. Any digital file can be copied, but an NFT’s originality is always verifiable: no matter how many times you copy the image or file, only one version will ever be recognized as legitimate by the blockchain.

That opens up all kinds of possibilities.

Take property rentals, for example. Suppose Alice rents out her place — first to Bob, then to Carol, and now to Dave. When Alice hands over the key to Dave, a problem could arise: what if someone else, using a copy of the key, gets inside and takes something? Who’s responsible — Bob, Carol, maybe even Alice herself? Anyone could have made a copy of the key, and Dave might suspect all of them.

But with a digital lock and an NFT as the “key,” this isn’t possible. When Alice rented to Bob, she transferred the NFT to him, and he gave it back at the end of the lease. The same happened with Carol. Technically, anyone can copy the digital file, but only the original NFT will open the door. The smart contract for the lock checks the blockchain to confirm the key’s authenticity. During Dave’s rental period, only his wallet can open the door — any duplicate, no matter how perfect, will be rejected. Moreover, when the lease is over, the smart contract may simply stop accepting that NFT as a key.

The same logic applies to any kind of digital key or credential — even, in theory, something as critical as the launch codes for a nuclear arsenal. In countries where leadership changes from time to time, imagine if an outgoing president hands over the nuclear “key” but secretly keeps a copy. With a traditional system, this would be a security nightmare. But if the key is an NFT, making a duplicate is pointless: only the legitimate, one-of-a-kind NFT grants access.

It’s a dramatic example, but it shows just how powerful this technology could be for humanity. And there are plenty of less dramatic, everyday situations where NFTs could solve old problems.

Ever bought a digital ticket? You show up to the event, flash your QR code, and — oops — someone else has already used it. What can you do? This can happen even without scalpers, just because of technical glitches. But if event entry required you to send an NFT to a smart contract (say, to open a turnstile), no one else could use your ticket, and all transactions would be recorded on a public blockchain. Any technical mishap would be easy to spot and prove.

Authenticating a token can be useful for all sorts of digital documents: from IDs to promissory notes. Think about crypto exchange verification — you upload scans of your ID and proof of address. But how does the exchange know you’re not sending them well-made forgeries? In the current system, they can’t be sure. If your document were a digital NFT, though, verification would be simple. Even better, exchange employees wouldn’t be able to steal your documents for fraud — copies wouldn’t work, and the original NFT (along with the signature from your wallet) would remain yours.

Sure, most Rabbit Swap users probably don’t use exchanges that require such verification, but for everyone else, these problems are all too real.

So, NFTs are a powerful technology that can solve real-world problems. Right now, their reputation has taken a hit because people are using them for all the wrong reasons. But an NFT renaissance is inevitable. The technology is simply too good — and too useful — to stay forgotten.

Why Doesn’t Rabbit Swap Exchange NFTs?

We don’t support NFT swaps — and it’s not just because nearly 100% of all NFTs are illiquid, although that’s certainly the main reason.

There’s also another reason, and I hope this article has made it clear. The fact is, we don’t consider NFTs to be true cryptocurrency assets. Yes, they were born in the same ecosystem as cryptocurrencies, but they aren’t really suited for transferring value. It’s simply impossible to objectively determine how much any unique token is worth.

Since the NFT boom in 2021, plenty of experts have criticized the NFT industry for losing sight of its genuinely useful applications. Moxie Marlinspike, founder of Signal; Dan Olson, creator of the documentary “Line Goes Up — The Problem With NFTs”; and UC Berkeley professor Nicholas Weaver have all pointed out that “collecting pictures” without transferring any real rights or ownership cheapens the technology. Yet, that’s exactly how most NFTs are being used today.

Strictly speaking, this isn’t even a new problem. Even Kevin McCoy — the artist behind the first NFT artwork, Quantum — eventually minted and sold a version of it on Ethereum for $1.4 million, even though the original hash still exists on the Namecoin blockchain. So who actually owns the rights to the work: the Namecoin name holder or the Ethereum token owner? In reality, neither does. The rights remain with the creator. So what do the token holders actually have?

As things stand, the NFT industry often feels like one big illusion. That said, if you buy NFTs on platforms like exchange.art, objkt.com, or foundation.app to directly support digital artists, there’s nothing dishonest about that. NFTs, in their current form, help encourage patronage and support for the arts.

But beyond the world of digital art, the potential of NFTs is so much greater!