bullHYPE: The Return of Leveraged Tokens. Part II

In Part I, I traced the history of leveraged tokens: how they emerged, why they died, and why even the survivors, ETH2x-FLI and XSOL, still lost 97-99% of their value. And now the Hyperliquid ecosystem has produced a reincarnation of this idea: bullHYPE from Hypezion Finance, which people are praising as a good way to long HYPE at the bottom with leverage and no liquidation risk - exactly the way people once talked about BULL, BEAR, UP, DOWN, and other tokens of that kind.

I already mentioned in Part I that Hypezion has implemented things differently. So let’s take a closer look at how this is structured.

How it works

To understand what fundamentally sets bullHYPE apart from everything that came before it, let's use an analogy.

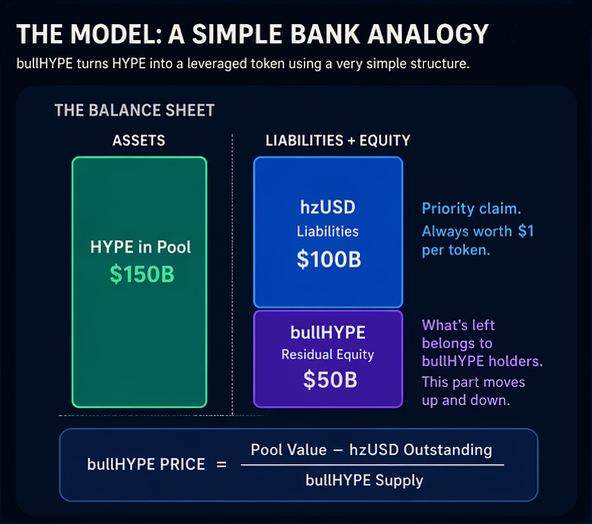

Imagine a bank. It has $150 billion in assets and $100 billion in liabilities to depositors. The shareholders own the remainder: $50 billion.

Now imagine the value of the bank's assets rises to $170 billion. An interesting picture emerges: the bank's assets are up 13%, but the amount belonging to the shareholders is up 40%, from $50 billion to $70 billion. The depositors, meanwhile, still have the same $100 billion they had before.

But if the assets fall to $130 billion, again by 13%, then the shareholders take a 40% loss, while the depositors take no loss at all: their $100 billion remains intact.

That is exactly the structure Hypezion Finance implements. The roles are distributed as follows:

- The assets. Some users deposit HYPE tokens into the protocol treasury in exchange for hzUSD, while others do so in exchange for bullHYPE. All the HYPE deposited remains in the collateral pool, and that is all the "bank" ever has at any given moment.

- The liabilities. These are the hzUSD stablecoins that have been issued. Each hzUSD token is an IOU backed by exactly $1 worth of assets from the pool. hzUSD holders are the "depositors": they have a senior claim on the collateral and get paid first.

- The amount belonging to the "shareholders." This is bullHYPE. Its price is whatever remains of the assets after all liabilities have been covered. The pricing formula for bullHYPE is transparent and fixed in the smart contract:

bullHYPE price = (Pool value - hzUSD outstanding) / bullHYPE supply

This core feature - the existence of an officially declared price, rather than only a market price - makes bullHYPE resemble the leveraged tokens I discussed in Part I. But unlike many of the tokens mentioned there, exchanging bullHYPE at the official rate does not depend on the goodwill of an exchange market maker. It can be done at any time through the smart contract itself. True, the redemption is not into dollars or even stablecoins, but only into the HYPE tokens stored in the collateral pool. But that should not be a problem, because HYPE can always be swapped into any stablecoin at the best rate on rabbit.io.

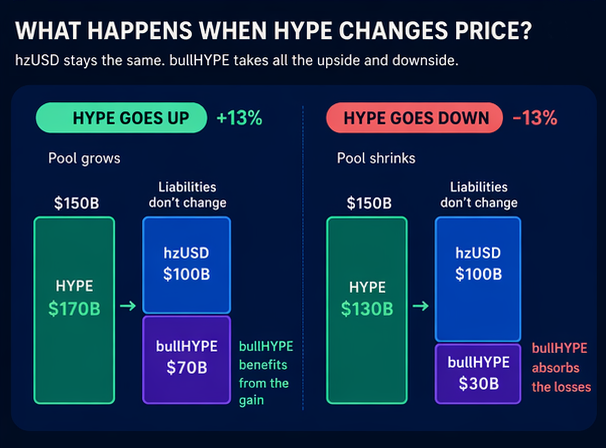

To make the bank analogy clearer, here is what happens when the price of HYPE changes:

- HYPE goes up. The value of the collateral pool rises with it. The liabilities to hzUSD holders do not change, so the entire gain goes to the "shareholders" - the bullHYPE holders.

- HYPE goes down. The hzUSD debt does not go anywhere, so the entire hit is absorbed by bullHYPE.

Depositors are protected, shareholders bear the risk, and in return for taking that risk they get the upside when prices rise.

There are no futures. There is no daily rebalancing either. The leverage is not set in advance: it emerges from the ratio between debt and residual equity.

At any moment, the effective leverage can be calculated using this formula: Leverage = Pool value / bullHYPE market capitalization

If many people mint hzUSD, the "shareholders'" share in the "bank's" assets shrinks, and leverage rises. If hzUSD is redeemed, leverage falls.

Hypezion Finance's three main promises

1. No liquidations

That is true, but there is a catch: bullHYPE holders are the first to absorb losses in the system. If HYPE falls by 20%, hzUSD stays at $1, while bullHYPE loses far more than 20%. You do not get a margin call, but you may still lose 40-60% of your asset value.

No liquidation does not mean no losses. It only means no forced exit from the market. Even if you lose 99.9% of the value of your investment, you still keep the tokens, and they will continue to rise and fall in sync with HYPE.

2. No funding rate

That is also true, and it is a real advantage. In traditional models, leveraged-token holders indirectly paid the funding costs on the futures used to create the upside and downside exposure. Remember, on FTX that came to 0.03% per day, or about 11% per year. bullHYPE does not open futures positions, so there is no carrying cost for simply holding it.

But no funding rate does not mean no costs at all. There are minting and redemption fees, and they can range from 1% to 8% depending on the state of the pool. When the "shareholders'" share in the "bank's" total assets becomes too small, minting is cheap and redemption is expensive. And vice versa: if there is a lot of bullHYPE outstanding and relatively little hzUSD, the fee for minting new bullHYPE rises while the redemption fee falls.

3. No volatility decay

This is the most interesting promise. And for the most part, it is actually true.

In Part I, I explained the mechanism by which classic leveraged tokens decay: with every up-and-down cycle, rebalancing eats away part of their value. ETH2x-FLI did not lose 99.6% because ETH crashed. It lost it because the math of compounding worked against holders every single day.

Under normal conditions, bullHYPE does not rebalance. If HYPE falls 20% and then returns a month later, bullHYPE should return as well. So this particular mathematical flaw has, to a significant extent, been removed.

But removing the biggest risk does not mean removing all risks. New ones have appeared.

The four risks of bullHYPE

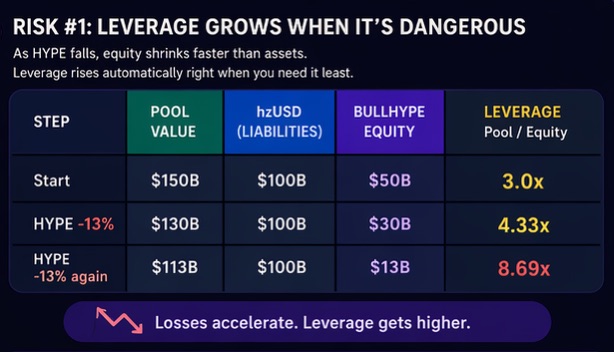

1. Leverage rises precisely when that becomes dangerous

Let's go back to the bank example.

We start with:

- total assets of $150 billion,

- liabilities of $100 billion,

- shareholder equity of $50 billion.

If assets fall by 13% from $150 billion, that is a loss of $20 billion:

- total assets become $130 billion,

- liabilities remain $100 billion,

- shareholders are left with $30 billion, meaning they have lost 40% of their original $50 billion.

If assets then fall by another 13% from $130 billion, that is another $17 billion:

- total assets become $113 billion,

- liabilities remain $100 billion,

- shareholders are left with $13 billion, meaning they have lost 57% of their remaining $30 billion.

The same thing happens in Hypezion Finance. When HYPE falls, the collateral value shrinks, but the hzUSD liabilities remain unchanged. That means the price of bullHYPE melts faster and faster. Leverage rises automatically at exactly the moment the market is moving against you.

That immediately raises a question: what happens if assets fall by another 13%? Total assets would drop below total liabilities. Does that mean bullHYPE would have a negative price?

Judging by the formula stated in the protocol rules, yes. But the smart contract contains protection against that scenario, and it introduces another set of unpleasant facts for holders of the leveraged token. This is where socialization of losses comes in, diluting the value of bullHYPE.

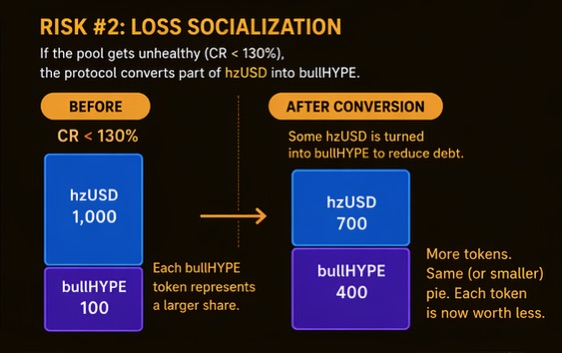

2. Loss socialization

The health of the collateral pool is measured by the Collateralization Ratio, or CR. This is the ratio of pool assets to liabilities. When CR falls below 130%, the system enters a critical mode. In this mode, the protocol automatically converts part of the hzUSD supply into bullHYPE in order to reduce the pool's debt burden and save the system from collapse.

For hzUSD holders, this means their stablecoin is not quite as stable as it seems. At some point it may suddenly turn into a rapidly falling leveraged token. So it is better to redeem the stablecoin before CR drops below 130%. If it is redeemed, the pool's liabilities shrink, CR rises, and the risk of entering critical mode declines.

But if the system does enter critical mode, the newly issued bullHYPE dilutes the share of the old "shareholders." Yes, some of the losses of existing bullHYPE holders are shifted onto the new involuntary holders, the former "depositors." But once HYPE starts rising again, bullHYPE will behave the same way BULL tokens behaved under rebalancing. The total value of all bullHYPE will grow as fast as it previously fell, but each individual token will represent a smaller share of that total than it did before the downturn. Which means that even if HYPE returns to the level it was at before the decline started, bullHYPE will not return to its original price.

There is another point worth noticing. The collateralization ratio can fall below 130% not only because HYPE crashes. Another reason the pool can become less healthy is that bullUSD holders may redeem a large amount of tokens, exchanging them for HYPE, for example to lock in profits after a rally. That too would trigger the same kind of rebalancing-like effect described above.

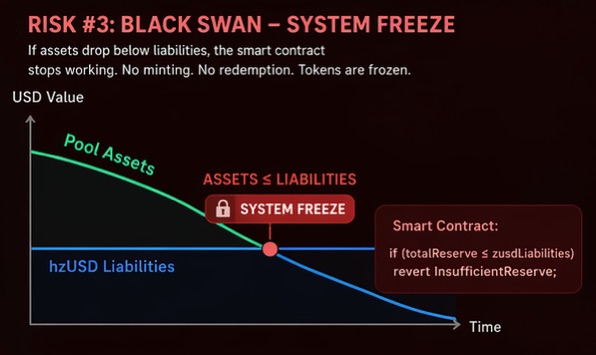

3. The "black swan" scenario

If loss socialization fails for some reason - for example, if HYPE drops by tens of percent in a matter of seconds and the protocol simply does not have time to convert hzUSD into bullHYPE - the tokens become frozen, and no operations with them are possible. The smart contract states that if totalReserve ≤ zusdLiabilities, then any token operation reverts with the error InsufficientReserve.

And even adding more HYPE to the pool would not help. Depositing HYPE in order to mint more stablecoins would only increase the pool's liabilities and make the problem worse. Depositing HYPE in order to mint or redeem bullHYPE is impossible as well, because according to the bullHYPE pricing formula, the token price would be negative. That would mean the address depositing HYPE would also need to surrender additional bullHYPE on top of it - which is obviously nonsense.

In a black swan scenario, your tokens remain in your wallet, but the system itself is frozen until the price of HYPE rises enough for the value of assets to exceed liabilities again. And once that happens, a large share of hzUSD will be abruptly converted into bullHYPE, causing heavy dilution in bullHYPE.

4. No real-world track record

All comparable protocols - Liquity, MakerDAO, Ethena, Money-on-Chain - have been through real stress tests. Some of them suffered real failures along the way. Some did not survive at all, like the LUNA/UST structure. Hypezion Finance has not been through anything like that yet.

And one more thing should be kept in mind: all the protocol's eggs are in one basket. The entire collateral pool consists only of HYPE. If Hyperliquid runs into systemic trouble, the pool will have no outside source of value to restore solvency.

So are HYPE supporters right?

Is bullHYPE a "good way to long HYPE at the bottom with leverage and no liquidation risk"?

bullHYPE really does eliminate funding costs and dependence on an exchange market maker, and in most cases it eliminates volatility decay as well. Those are real and meaningful improvements over BULL, BTCUP, and the rest of the dead products that came before it.

But the risk has not disappeared. It has been transformed - from slow decay toward zero in a sideways market into:

- the danger of losing a large share of your position very quickly in a sharp downside move,

- the threat of new token issuance and value dilution when holders rush for the exit,

- the risk of a full token freeze in the worst-case scenario,

- and the simple fact that this is a very young protocol with no battle-tested track record.

In short, bullHYPE is not a risk-free long. It is a long with a different risk profile. If you are convinced that HYPE will appreciate over the long term, the safer option is to come to rabbit.io, buy HYPE for any stablecoin or any other cryptocurrency at the best available rate, and hold HYPE itself rather than a derivative built on top of it.

But before you do that, read one of my older articles about a rarely discussed flaw of HYPE's own tokenomics: Airdrop Hunters and the Ponzi-style Tokenomics

Everything above is based on the protocol documentation, the public Hypezion Finance smart contract, and the BEOSIN audit report from November 2025. The system's real behavior under bear-market conditions and extreme volatility still has to be tested in practice.