Airdrop Hunters and the Ponzi-Style Tokenomics

In the final days of 2025, right after Lighter's LIT airdrop, crypto communities were buzzing with comparisons between Lighter and its biggest rival, Hyperliquid.

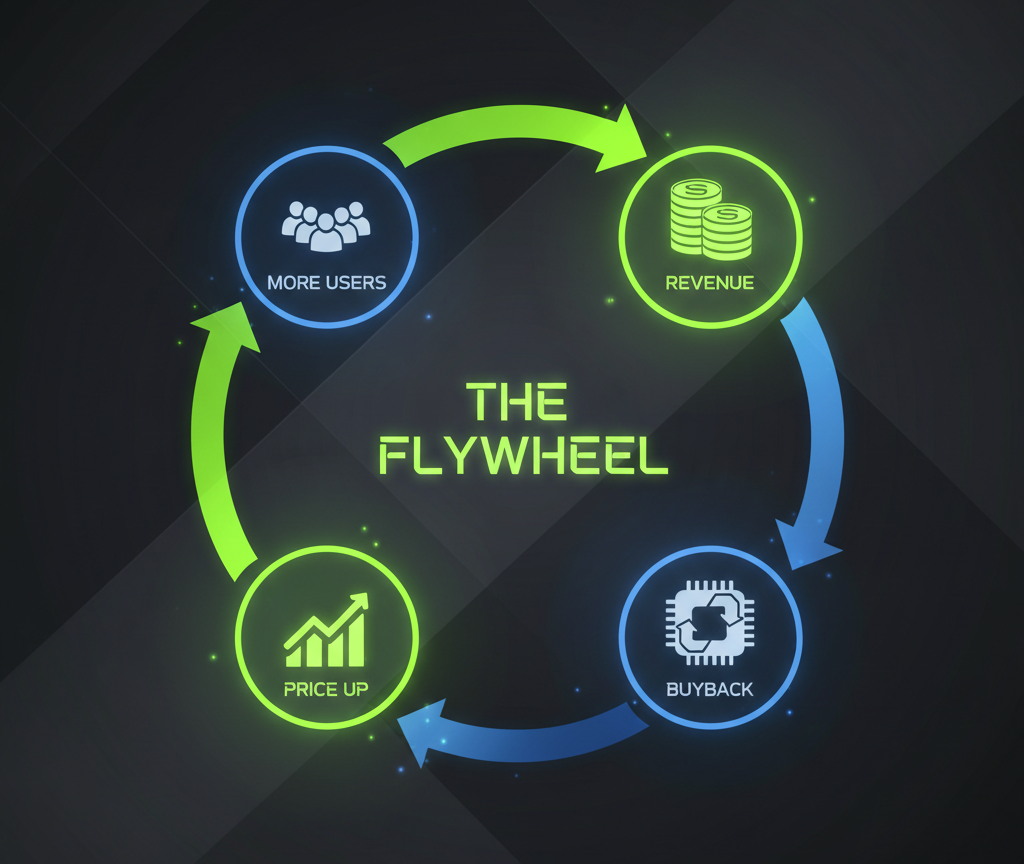

In one of those debates, a supporter of Hyperliquid summarized the advantage of his favorite platform like this: "revenue → buybacks → token price goes up → more users → more revenue - a closed growth loop."

It sounds smooth, almost like a self-running engine. But one piece of that logic caught my attention: "token price goes up → more users." That connection isn't obvious to me. When traders choose an exchange, they usually care about execution, liquidity, fees, uptime - not the market price of the exchange token.

As I started digging into the mechanics, I noticed a structure that strongly resembles a Ponzi-style model.

Quick reminder for context: a Ponzi scheme is a financial scam where returns to earlier participants are paid using the money of newcomers, without any actual underlying economic activity. These structures tend to collapse once the inflow of new funds slows down or stops.

The Motivation Puzzle: Why Pay More?

Imagine you’re at a market shopping for apples. The stand on the left sells them for $2, while the one on the right offers the exact same apples for $1. Where would you buy? The answer is obvious to anyone with common sense.

On onchain derivatives exchanges, the “apples” are trading services - opening and closing positions, recording them on-chain, and managing balances. And the “price” of those apples is the trading fee. Hyperliquid has consistently charged higher fees than Lighter and some of its other competitors. So the question is: are all these “apples” really the same?

Objectively, no. Hyperliquid is the largest onchain derivatives platform with the deepest liquidity. Perhaps only Aster comes close. But Aster isn’t exactly an onchain platform - or maybe not onchain at all, since I’ve never seen its trades show up in any blockchain explorer. So yes, Hyperliquid probably offers the “shiniest apples.”

But let’s be honest: only whales actually need a $100 million order book. For the average trader with a $10k or even $100k portfolio, it doesn’t really matter if the liquidity pool is $10 million or $50 million. Their orders will execute just fine either way. So for most users, the "apples" are functionally identical - and what really matters is how much they’re paying for them.

So why are crowds of traders still choosing Hyperliquid and willingly paying higher fees? And how exactly does a rising HYPE token price attract new users?

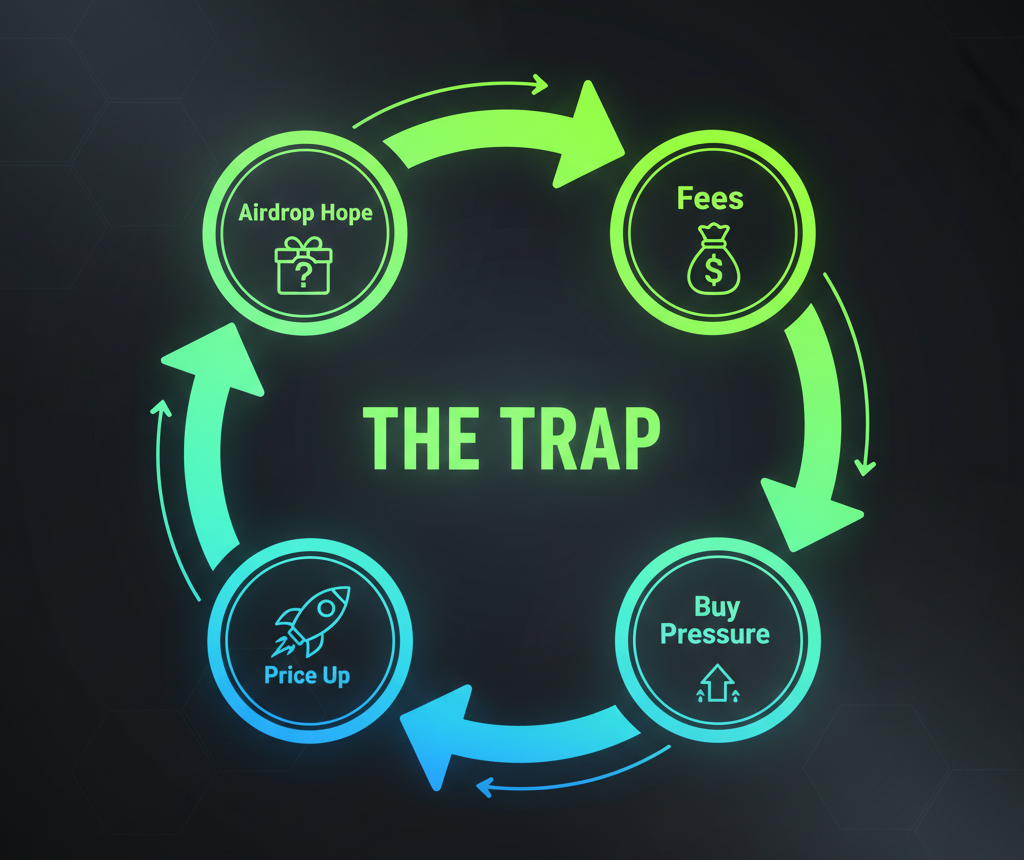

I asked the person who originally described Hyperliquid’s so-called “flywheel” to me. His reply was disarmingly honest: “New users come for the future airdrops. The higher the HYPE price is now, the juicier those future drops look. People are trading not for trading - but for points.”

And that’s where the Ponzi-style trap begins.

The Economics of Hope

Let’s trace the money behind HYPE tokenomics. It’s often framed as a business model, but in reality, it functions more like a value redistribution loop powered by expectations.

1. The Donor

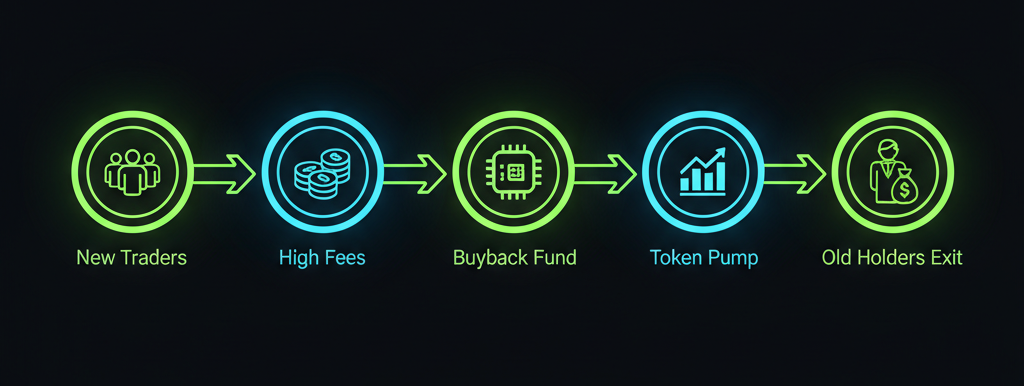

A trader joins Hyperliquid and starts racking up trades - sometimes way more often or larger than they normally would - just to boost their activity stats. Every trade costs them a fee. Yes, the fee is higher than on competing platforms, but many treat it like paying for a future reward - earning points today to get more HYPE in a potential upcoming airdrop.

2. The Assistance Fund

So where does that fee money go? In a normal company, revenue gets split between improving the product, paying the team, and rewarding investors. But here, almost everything flows into one place - a buyback fund. It's called Assistance Fund, and its only job is to purchase HYPE tokens from the open market using the fees paid by traders.

3. The Beneficiary

Who sells those tokens to the fund? Mostly the people who got HYPE earlier - either from the original genesis airdrop or from buying after. So the cash that early holders receive today comes directly from the fees paid by new traders. That fee money doesn’t fuel development or trading perks for newcomers - it becomes exit liquidity for those who were already holding the token.

The Result:

Early participants turn their tokens into cash using funds supplied by new participants. Meanwhile, new participants pay premium fees hoping that even more traders will join after them - bringing fresh fee money that might later become their own chance to exit into cash.

The Ghost of Charles Ponzi

Let’s revisit the classic Ponzi scheme model. In its core version, early “investors” get paid with the funds contributed by new ones - not with profits from any real business. At first glance, this may not seem relevant to Hyperliquid. After all, it’s a functioning exchange. It has a product, a slick interface, fast execution, and real trading activity.

That’s all true. The product exists. But the sale of the product doesn’t. The people who build and maintain the exchange don’t benefit from user fees. Instead, those fees end up enriching people who have nothing to do with the development or operation of the platform.

Here’s a thought experiment. What if Hyperliquid announced tomorrow that there would be no more airdrops? Or what if they said: “That was the final buyback, the HYPE token is only for governance from now on”? What would happen?

It becomes clearer when you recall how HYPE governance has worked so far:

- Voting on who gets to assign the ticker USDH to their token.

- Voting on whether to officially “burn” tokens that were already essentially unrecoverable.

Let’s be honest - these votes aren’t particularly impactful. What really matters is the one thing users are chasing when they overpay fees on Hyperliquid: hope. If that hope disappears, so will the traders. They’ll move to platforms where fees are lower but the “apples” - the trading experience - are basically the same.

In the end, a huge part of Hyperliquid’s traction doesn’t stem from the value of the product itself, but from a clever mechanism that channels funds from the bottom to the top. Traders aren’t paying for a service. They’re paying an entrance fee into an exclusive club - hoping the club keeps growing so they’ll one day benefit like those who got in earlier.

When the Music Stops

Any system that relies on a continuous inflow of new money to pay off earlier participants shares a common weakness: the audience isn’t infinite.

In the so-called “flywheel” model, the step “more users” only works under two conditions:

a) users believe that the next airdrop will more than cover the fees they’re paying today;

b) the inflow of new donors exceeds the pace at which early beneficiaries cash out.

If Hyperliquid's user base starts to shrink - or if the flood of newcomers makes the next airdrop look too diluted - the math turns negative for new traders. Buying a “lottery ticket” that costs thousands of dollars in fees stops making sense. That’s when the flywheel stops spinning and turns into a meat grinder. The last ones in are the ones paying for the feast enjoyed by those who got out in time.

Hyperliquid has built a brilliant piece of technology - but it attached a financial pump that runs on greed. Traders need to realize that every time they pay above-market fees hoping for a drop, they’re not investing in the exchange. They’re simply passing money along to those who got in earlier. And there’s no guarantee someone else will show up after them to do the same.

Are Only HYPE Holders at Risk?

HYPE is far from the only example of a Ponzi-style mechanism hidden within token farming. In fact, crypto history is full of projects built on the same principle. There’s even a name for it: Trading-as-Mining or Trade-to-Earn.

One of the most dramatic examples of this model was FCoin, a crypto exchange that launched in 2018. FCoin was the first to introduce the “Trading-as-Mining” concept, promising to refund users 100% of their trading fees (and sometimes even more) in the form of native FT tokens. Even more aggressively, it pledged to redistribute 80% of the exchange’s revenue to FT holders. While the structure differed slightly, the core logic was the same: “Pay fees → receive tokens → token value rises because of those same fees.”

So what did users do? They launched trading bots that endlessly traded with themselves, racking up billions in volume. They paid real fees (in BTC and other cryptos) just to farm FT tokens.

FCoin’s volume quickly overtook every competitor on the market. But once the flow of new users slowed - and with it, the flow of new buyers drawn in by the promise of dividends - the token's price collapsed. Early holders cashed out at the expense of newcomers, and the exchange shut down amid scandal.

In reality, almost any platform that hands out tokens in exchange for fee-based user activity contains some element of a concealed Ponzi dynamic. If you're earning income based on the commissions of those who come after you, there's a far more transparent and sustainable way to do that: affiliate programs.

Affiliate programs don’t require you to “pay first” to participate. You don’t have to fund the profits of those who joined before you. Entry is typically free, and your rewards are tied to how well you help grow the project.

The swapping service Rabbit.io offers an affiliate program, too. You can create an affiliate account and earn a share of the profit generated from users who visit the site via your link and complete a swap.

Disclaimer

In many jurisdictions, schemes that generate returns solely from the inflow of new “contributors” are considered illegal and even criminally punishable. But I am by no means accusing the teams distributing their tokens through the model described in this article of committing a crime. Rather, I aim to highlight the risks such a model carries.

The key element that transforms this kind of setup into a crime is the guarantee of returns. Hyperliquid, in particular, demonstrates how a project can carefully avoid crossing that line.

- The tokenomics are public and transparent. The community knows exactly how many tokens are set aside for future airdrops, can track how many have already been distributed, and can roughly forecast what’s still left - to the point where future distributions feel almost pre‑announced. But crucially, the team has never guaranteed that future distributions will reward trading activity specifically. Traders are simply extrapolating from the logic of the first airdrop. That logic may or may not apply going forward.

- Even if they’re right - and future airdrops are tied to trading - that still doesn’t constitute a promise of profit. The project’s Assistance Fund is designed to buy back tokens using trading fees. But a guaranteed buyback is not the same as a guaranteed price. There’s no certainty that the selling price of distributed tokens will exceed the trading costs incurred to earn them.

What this article describes are signs of a hidden Ponzi-like structure embedded in a mechanism for redistributing funds. But unless such economic models are combined with marketing efforts that explicitly promise returns to attract new users, they do not qualify as Ponzi schemes in a legal sense.