Why Do Crypto Companies Buy Back Their Own Tokens?

This week, Hyperliquid announced that it will now direct 99% of its revenue toward buying HYPE tokens on the open market.

When I first heard this, one question immediately came to mind: why would they do that? I asked around in a few Hyperliquid community chats, and the answers I got were all over the place:

- to reward users,

- to buy user loyalty,

- to draw attention and build a brand,

- to turn their tokens into something resembling shares,

and even:

- You don’t get it! That’s just how Web3 works!

So which of these explanations actually makes sense? And is there a “true” one at all? Let’s dig into it.

Rewarding Users

Rewarding users with a project’s own tokens is a very common practice in crypto. Some people take the time to explore the product, their feedback helps improve it, and sometimes they spread the word to others — all of that is worth rewarding. And if the product comes from a startup that’s just entering the market, without the ability to pay in cash or in a solid cryptocurrency, then the reward will almost certainly be paid out in the startup’s own tokens. After all, minting those tokens costs the team practically nothing.

Yes, this is exactly what many teams do when they launch their product in the crypto market. But then a question comes up: why would they later start buying those tokens back from users? Doesn’t that undermine the whole point of the airdrop? Wouldn’t it make more sense to just pay users in dollars — or in another cryptocurrency that has intrinsic value?

Binance, for example, spends part of its profits on buying back and burning BNB. This drives the token’s price higher and, at the same time, increases the capital of users who rely on Binance products that actually require BNB. But that’s a completely different story. Binance never gave its tokens away for free!

So who did? Think of Aptos, Arbitrum, Hamster Kombat, and countless other startups. They all handed out tokens to users and then let those tokens float freely on the market. Users quickly swapped them for something else, and there was no need for the developers to create any artificial demand. Aptos and Arbitrum are still running today, and the drop in their token prices hasn’t stopped them from operating. Hamster Kombat, though, quickly lost its user base — and the falling token price played a big role in that.

Buying Loyalty

Buying user loyalty by creating artificial demand for a token is mostly relevant to crypto projects whose entire value proposition revolves around the token itself.

Take Hamster Kombat, for example — would anyone care about it if it weren’t for the token? The moment the token failed, interest in the project faded as well.

The same logic applies to tokens like MKR and SKY, issued by MakerDAO and its successor Sky Protocol. If no one holds these tokens, the protocols lose their purpose. After all, their role is to support the stablecoins DAI and USDS, and one of the key stability mechanisms involves pushing certain risks onto MKR and SKY holders. If a portion of the protocol’s revenue weren’t regularly spent on buying back and burning these tokens — effectively making them deflationary — no one would want to hold them.

But if a project’s token is not its core product, then price growth doesn’t necessarily impact whether people use the project or not. Hyperliquid is a good example of that. People use the on-chain derivatives exchange, the smart contracts on HyperEVM, and other services in the Hyperliquid ecosystem because they’re convenient and effective — not because there’s a token called HYPE and its price might go up.

There’s no guarantee that HYPE holders use Hyperliquid. And many Hyperliquid users don’t hold any HYPE at all.

So any effort aimed at winning over tokenholders might have no effect on the loyalty of actual users. But what Hyperliquid really needs — presumably — are users, not tokenholders. The team doesn’t sell HYPE tokens and earns nothing from them directly. What it does earn from is product usage. Yet it gives away 99% of its revenue to HYPE holders.

Drawing Attention and Building a Brand

Yes, bold moves like pledging 99% of all revenue to buy back tokens are guaranteed to turn heads. It’s a powerful marketing tool. But at what cost?!

Can you name a single business in any other industry that spends 99% of its revenue — not profits, revenue — on marketing? Maybe spending almost everything you earn on marketing works early on, when you’re just trying to break through the noise.

But Hyperliquid isn’t some unknown startup anymore. It’s already a major player in the world of derivatives, with trading volumes comparable to the biggest names in the business. By now, it should be in a position to spend far less than 99% of its revenue on marketing.

Some say crypto companies that use profits to buy back their own tokens gain something even more valuable in return: an army of true believers. Every tokenholder becomes personally invested in the company’s success. The more revenue the company earns, the more money gets spent supporting the token price — and that alignment of interests creates a loyal community that promotes the project and even helps with support.

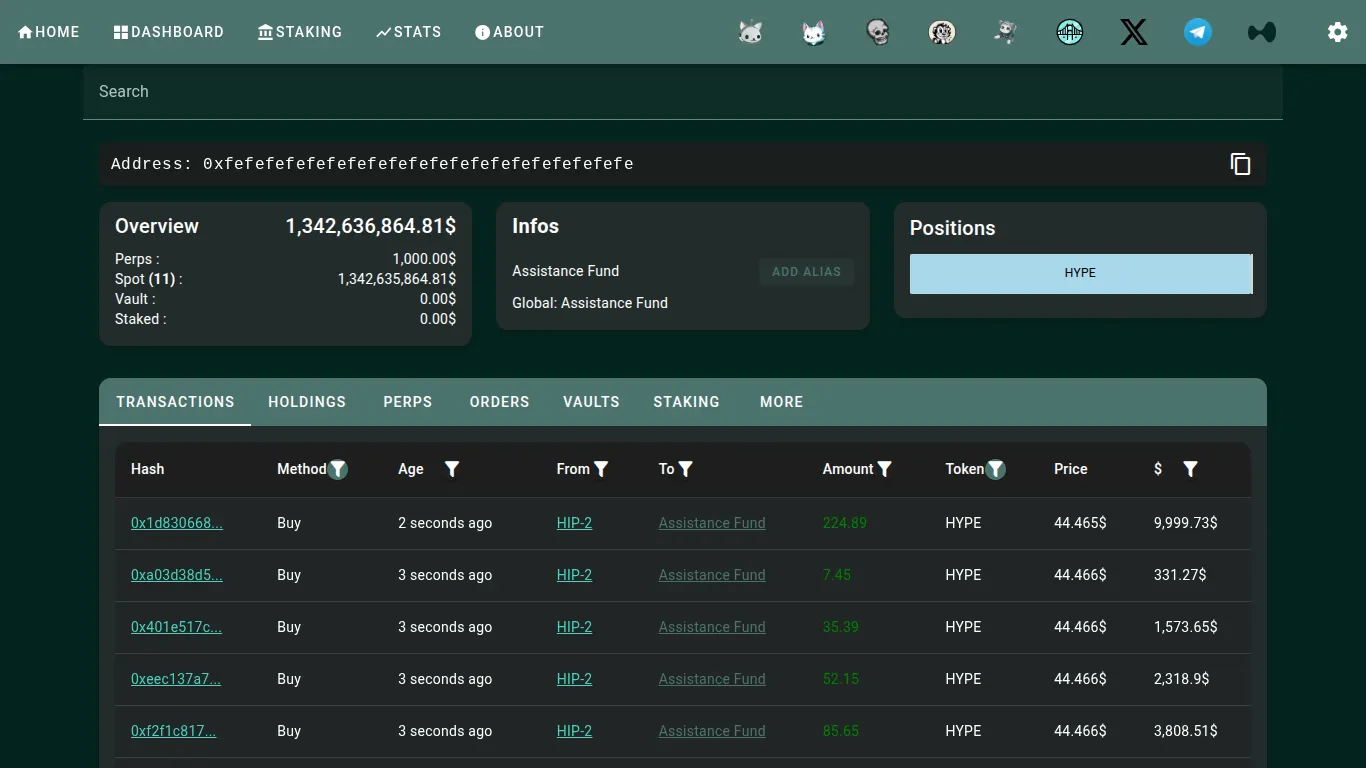

But look at how massive the buybacks have already become. The Hyperliquid smart contract that handles token purchases has accumulated over a billion dollars’ worth of HYPE tokens — and new purchases are being made almost every second.

Now ask yourself: how much would it cost to hire the best growth marketers in the world? I’m pretty sure it would be way less than that. And the results might not be worse either.

When Tokens Start to Look Like Shares

What do tokens and shares have in common? In cases where a company uses its revenue to buy back tokens, holders are essentially receiving a share of those profits — much like shareholders do in traditional finance.

Sounds reasonable at first. But in traditional business, a company issues shares when it needs capital to grow. It sells ownership in exchange for funding. Shareholders — especially if they band together — may eventually gain some level of control over the company. Understandably, founders aren’t usually thrilled about handing over too much power. That’s why some companies use profits to buy back shares: yes, they’re paying more than they originally raised, but they’re also slowly regaining ownership and minimizing investor influence. That kind of buyback makes perfect sense. Everyone wins — investors walk away with profits, and founders regain control.

But when a project buys back tokens, what’s the point? Tokenholders have no real control over the company — not even theoretical control.

There are exceptions, like the governance token for the dYdX protocol. Holding and staking DYDX tokens allows users to become validators in the dYdX Chain. If one group manages to control more than two-thirds of the stake, they could manipulate MEV opportunities, censor transactions, or even reverse blocks. So when the dYdX DAO uses a portion of protocol revenue to buy and stake these tokens, it’s actually a smart move — they’re defending the network by becoming a “megavalidator” and blocking anyone else from doing it.

But HYPE tokens don’t give that kind of power. They don’t carry any real rights or governance functions. In the Hyperliquid blockchain, no one can become a validator without approval from the core team. And the smart contract that buys HYPE isn’t staking them or using them in any meaningful way. It just keeps collecting them — with no clear endgame.

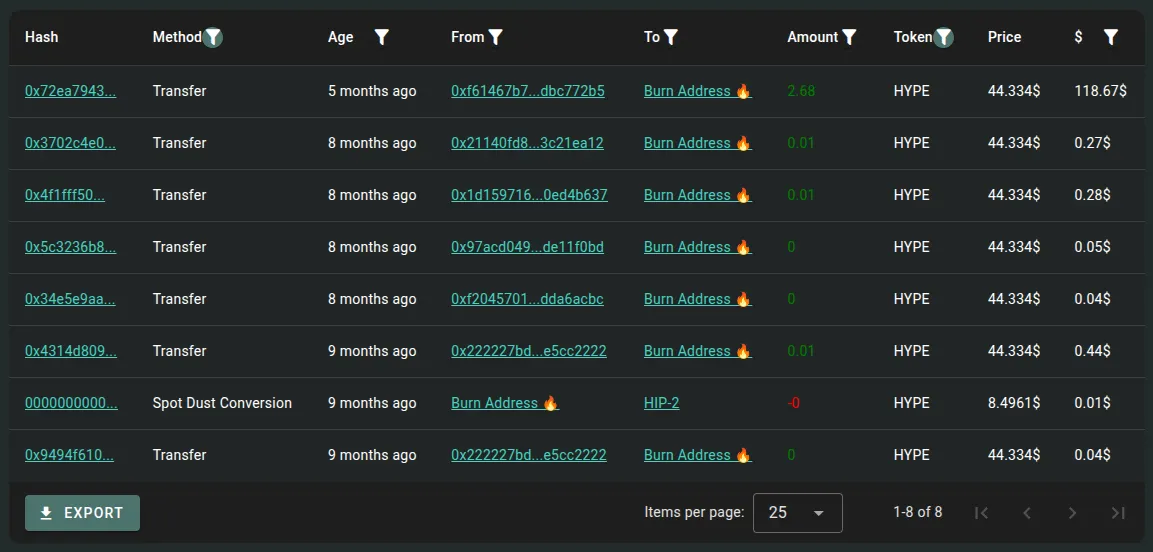

Some people assume these tokens are being burned. For instance, an article on OKX Learn makes this claim. But Hyperliquid is a blockchain — and blockchains don’t lie. Try finding a single transaction from the buyback contract 0xfe…fefe to the standard burn address 0x00…dead. I couldn’t.

Here are the latest incoming HYPE transactions to the burn address:

In short, the entire buyback program looks… pointless.

You Don’t Get It! That’s Just How Web3 Works!

Web3 runs on the principle of “code is law.” So when the Hyperliquid team promised to allocate the majority of the platform’s revenue to buying back HYPE tokens — and locked that promise into a smart contract — the whole point was that they couldn’t walk it back. Even if it became economically irrational, the code wouldn’t let them stop.

At least, that’s how it was supposed to work.

But events this past week showed that the smart contract’s rules can be changed. All it takes is consensus among the validators of the Hyperliquid blockchain. And since you can’t become a validator without the team’s approval, forming that consensus — when the team wants it — may not be hard at all.

So if it was possible to increase the buyback rate from 97% to 99%, it’s technically just as easy to reduce it to 50% or even 0%. Which means: this isn’t really about immutable smart contracts. There must be some deeper reason why these buybacks are still happening.

The most obvious explanation is that the Hyperliquid team holds a significant chunk of tokens under a vesting schedule. Sooner or later, those tokens will unlock — and the team has every incentive to keep the price high until then. That would explain why the buybacks continue: not to reward users, but to support the future valuation of the team’s own allocation.

Of course, there’s no guarantee this strategy will work. If competitors attract away the user base, or if regulators shut down uncontrolled trading on Hyperliquid, the token price could crash anyway — buybacks or not.

But in any case, if you ever need to swap HYPE — or any other token — you can always get the best exchange rates on rabbit.io.