Why ADL Isn’t the Villain Everyone Thinks It Is

Right before the crypto market crashed on October 10, one savvy trader hedged his $5 million long position in BTC by opening a $500 thousand short on Dogecoin with 15x leverage. A smart move! When Bitcoin drops, DOGE usually falls even harder. The setup looked perfectly balanced: the hedge was supposed to protect him and even leave him in profit if the market turned red.

When the crash came, his DOGE short did exactly what it was supposed to — it printed a big profit. But because of the high leverage, the exchange automatically closed that short through Auto-Deleveraging (ADL). The hedge was gone. The trader’s unprotected BTC long kept bleeding as the market continued to fall, and soon the entire position was liquidated.

The result: his portfolio was wiped out, even though he guessed the direction right and managed his risk responsibly.

Discussions across trading communities this week show that there were thousands of similar cases. ADL forcibly cut off profitable hedges, turning balanced strategies into one-sided disasters and wiping out accounts.

The crypto crowd has reached a rare consensus: “ADL is evil.” But I’d argue the opposite: ADL is one of the most misunderstood yet essential safety mechanisms in crypto markets.

Where and How ADL Is Used

ADL exists to keep derivatives exchanges functioning — especially those that trade perpetual futures.

Imagine you’ve just launched such an exchange. To start small, you introduce only one product: perpetual futures on BTC/USD.

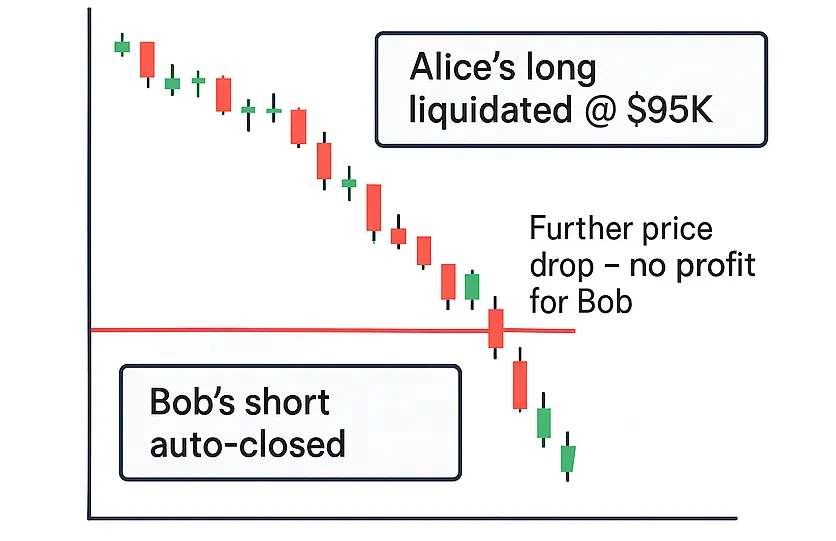

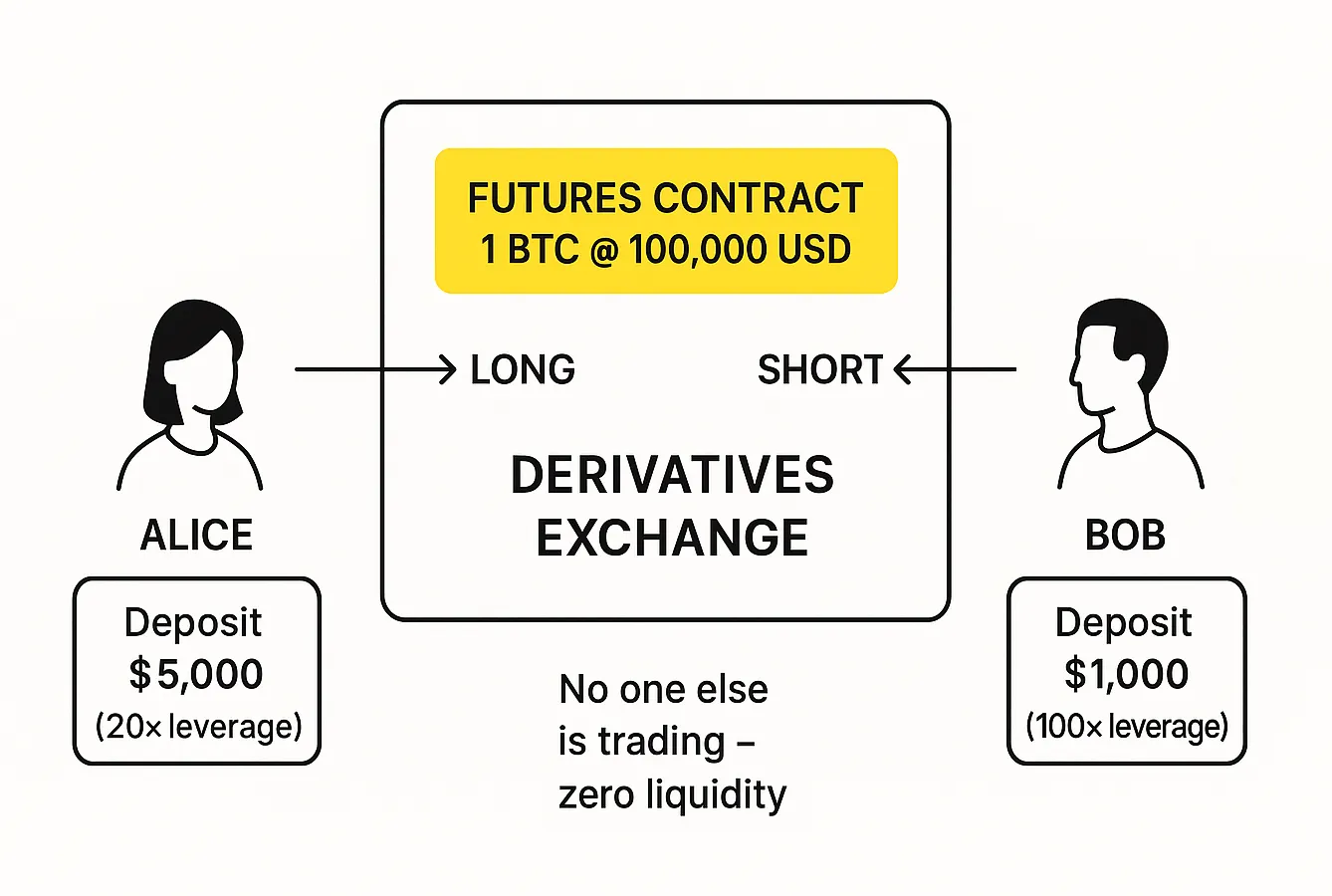

Two traders arrive: Alice and Bob. Alice deposits $5,000, Bob deposits $1,000. At a Bitcoin price of $100,000, Alice buys one BTC perpetual contract from Bob.

- For Alice, the leverage is 20x, because she controls a $100,000 position with only $5,000 of her own funds.

- For Bob, the leverage is 100x. His margin is a hundred times smaller than the contract size.

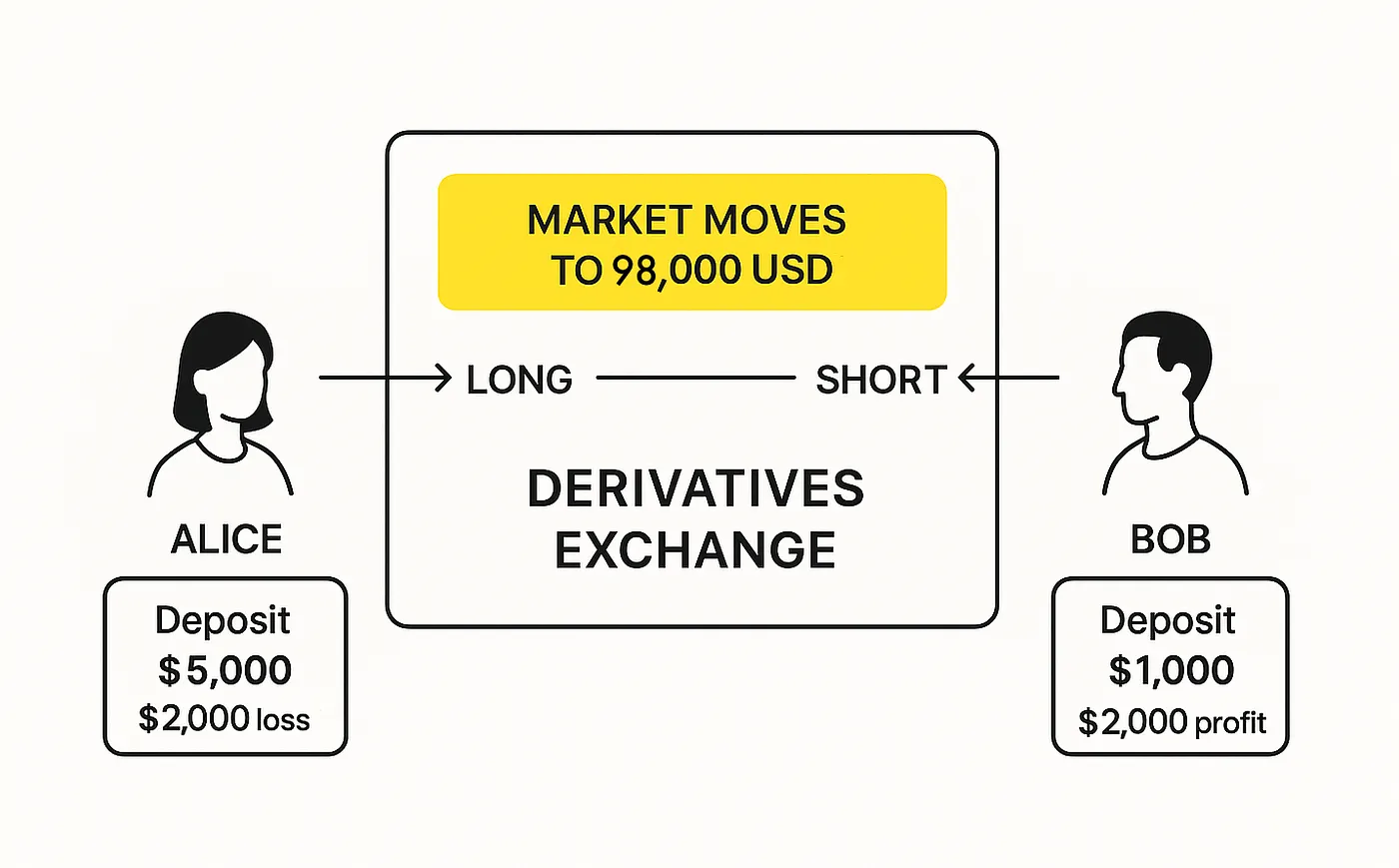

Then the BTC price starts to fall — down to $98,000. Bob now has a floating profit of $2,000, while Alice shows a floating loss of $2,000.

Alice doesn’t want to lose more, so she tries to close her position and places a sell order. But there’s no one else on the market — just her and Bob. Bob refuses to buy — he’s waiting for the price to drop even lower.

When the price hits $95,000, things get dangerous: Alice’s loss is now so big that one more dip would exceed her margin. She wouldn’t be able to pay Bob what she owes.

Neither Bob nor the exchange can force Alice to pay more than she originally deposited. So exchanges found another way. When Alice’s loss gets close to her margin, her position is forcibly liquidated.

To close Alice’s long 1 BTC, the exchange needs to sell 1 BTC contract. If there are other traders willing to buy, the trade happens. They take on the risk and the position continues under a new owner. But what if there are no buyers at all?

Then the exchange closes both sides of the trade — Alice’s and Bob’s. The contract that Alice originally bought from Bob at $100,000 is now automatically sold back to him at $95,000. No matter how far the price drops afterward, Bob won’t profit anymore — his short has been closed.

This forced closing of profitable positions is called Auto-Deleveraging (ADL). ADL happens when there simply aren’t enough limit orders in the order book to absorb the liquidations of losing positions.

The rule most exchanges follow is straightforward: If forced liquidations need to happen and there are no buyers, the buyers of last resort become traders whose profitable short positions have the highest leverage.

In other words, if there were several traders, Alice’s long wouldn’t necessarily be closed by Bob — it would be closed by the profitable short with the highest leverage.

What Are the Alternatives?

Crypto derivatives exchanges first faced the problem of traders defaulting on their obligations about a decade ago — in the early days of crypto futures.

On traditional futures markets, the broker takes on that counterparty risk. If a trader’s losses exceed their collateral, the broker still honors the trader’s obligations to the other side of the deal — and then goes after the client to collect the debt. Since a proper legal contract exists between the trader and the broker, the broker can take the case to court and enforce repayment.

Crypto exchanges never had that luxury. Traders might register on them anonymously, without revealing their personal data, and there were no professional intermediaries willing to guarantee traders’ losses.

Traditional exchanges also have “safety brakes”: daily price limits and circuit breakers that halt trading when the market collapses too fast. For instance, in U.S. equities, a drop of more than 7% automatically triggers a 15-minute pause — giving the market time to cool off and preventing a chain reaction of liquidations. If several halts fail to stabilize prices, a lower trading limit is imposed, freezing trades below a certain level until the next session.

Those measures stop panic, but they don’t solve the core issue. When trading resumes, if prices still don’t cover the losing traders’ obligations — or if the losses have grown even larger — there’s simply no money to pay the winners.

The first major crypto futures exchange, BitMEX, launched in 2014, experimented with several approaches:

- “Guaranteed settlement,” where the exchange promised to cover any losses itself.

- “Dynamic profit equalization,” where part of profitable traders’ gains was temporarily held and could later be reduced to offset others’ losses.

Guaranteed settlement risked bankrupting the exchange, while profit equalization angered users who hated seeing their profits clawed back. So, in October 2016, BitMEX adopted the Auto-Deleveraging model, which it still uses today.

ADL removed uncertainty: profits were now immediately available — and if your position wasn’t touched by ADL, nothing else could reduce your balance later. There was also a sense of fairness: before, one reckless trader with 100x leverage could cause losses for everyone else. Now, that same high-risk player might lose part of their own profit, while everyone else stayed unaffected.

The trading community largely welcomed the change. BitMEX grew rapidly, and within a few years ADL became the industry standard. New derivatives platforms — OKEx, Binance Futures, Bybit, Deribit, and others — all adopted auto-deleverage systems as part of their risk management.

“Socialized losses” became taboo. When OKEx in July 2018 distributed $9 million in losses among all profitable traders because one large whale went bankrupt, it caused a scandal. The exchange promised to revise its system and soon introduced an ADL-like mechanism to prevent that from ever happening again.

In other words, ADL was born as a response to collective punishment — better for a few over-leveraged winners to lose a bit of their profit than for everyone to share the losses.

One of the most recent adopters was Hyperliquid. Back in March 2025, it used a special reserve called HLP, funded by users who deposited capital in exchange for yield, taking on liquidation risk. But a massive position in the token JELLY — apparently opened just to drain that fund — exposed a fatal weakness. The exchange had no clean way to stop the exploit and was forced to close JELLY positions at off-market prices, which drew heavy criticism from competitors. In my view, Hyperliquid survived that crisis only because traders hoped for another HYPE token airdrop — the first one was generous enough to keep them loyal.

It’s worth noting that even in October 2025, many traders didn’t realize that Hyperliquid used ADL. Online debates blamed the exchange for unexpected position closures more than any other platform. Jeff Yan, the project’s founder, had to publicly clarify that their ADL mechanism was designed for users’ benefit, allowing them to lock in profit that would otherwise be absorbed by the system itself.

And he wasn’t wrong. In fact, ADL can sometimes increase traders’ total profit across all platforms — not just on Hyperliquid.

Imagine shorting ATOM at $3. Suddenly the price flash-crashes to $0.001. All longs get liquidated, your short gets closed by ADL — and then the price quickly rebounds to $2–$3. Result: you sold at $3, bought back at $0.001, and shorted again at $2. Without ADL, you might have missed that perfect spike entirely.

Why Traders Hate ADL

In the early days, traders used to complain about derivatives exchanges for a different reason: “Why should I pay for someone else’s mistakes?” Now, the complaint sounds more like: “Why did the exchange close my perfect trade?!”

The problem, as I see it, lies in the airdrop frenzy surrounding on-chain derivatives platforms. After last year’s massive Hyperliquid airdrop — over $1.2 billion worth of tokens distributed to traders — everyone rushed to trade on similar platforms, hoping to qualify for the next big giveaway.

To maximize their future airdrop rewards, traders began inflating their trading volume by any means possible. It might seem smart to run hedged strategies — one position offsetting another — to generate volume without taking much risk.

But that assumption is wrong. Many of the people who got caught by ADL last week were using such “safe” strategies without really understanding how perpetuals and leverage systems work.

ADL isn’t the villain in these stories. It doesn’t increase risk — it limits it. It ensures traders can’t lose more than the margin they’ve deposited. Remember, on traditional exchanges, during a violent price move, a trader can actually owe their broker more than they had in their account. ADL, by contrast, prevents that. It’s a built-in circuit breaker — protecting the system, and ultimately, protecting traders from themselves.

But it only works if you know how it works. Until you understand what ADL does and why it exists, you shouldn’t treat derivatives trading as an easy way to “farm” rewards.

If you’re still learning, you’re better off simply holding assets you believe in, and swapping them when needed.

When you do need to swap — the best rates are always available on rabbit.io.