Where’s the Bigger Risk: Banks or Crypto Exchanges?

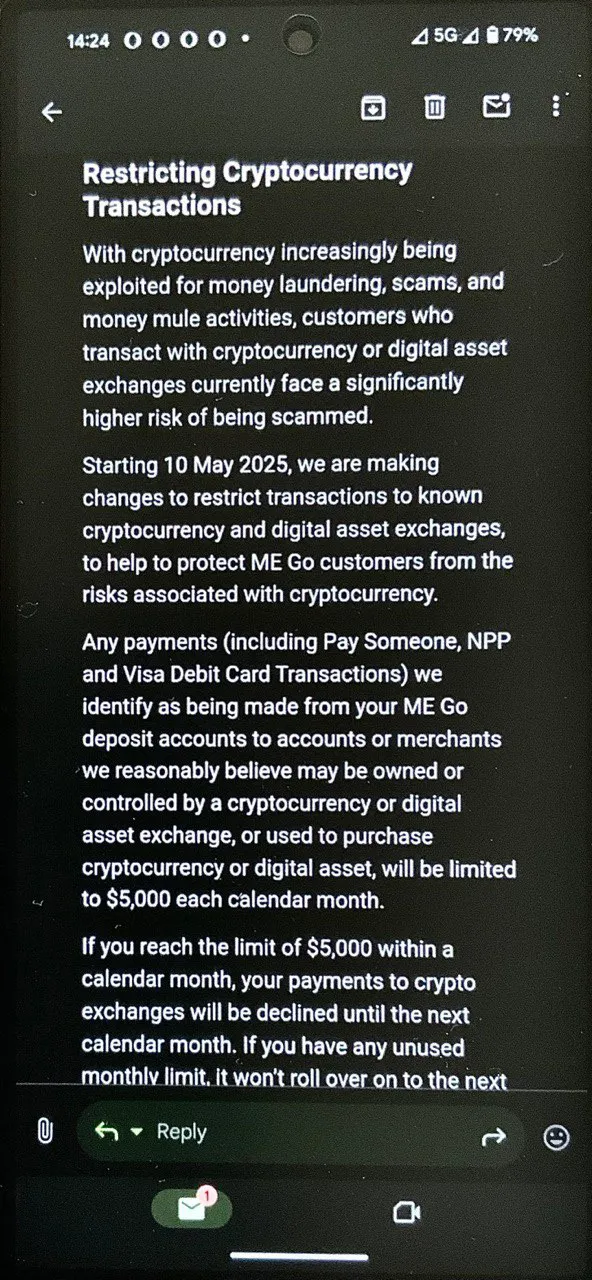

Last week, Australian ME Bank informed its customers that starting from May 10, 2025, it will introduce a cap on transfers to cryptocurrency and digital asset exchanges: no more than 5,000 AUD per calendar month. Clients reported receiving formal notices from the bank, sparking lively discussions in crypto-focused online communities.

One particular comment stood out to me. A user said that aside from daily essentials, the only thing he uses fiat money for is buying cryptocurrency. He receives his income in fiat, keeps just enough in his bank account to cover bills and basic needs, and converts the rest into crypto.

His approach seems quite rational to me. If I have money I don’t need right away, I don’t see the point in holding it in fiat currencies that are almost guaranteed to lose value. Some people try to protect their savings from inflation through business investments, others buy real estate or gold. My way is Bitcoin — and it seems this ME Bank customer does the same. Whether he chooses BTC, TRX, BNB, or any other crypto doesn’t really change the core idea.

He mentioned regularly transferring between 40,000 and 80,000 AUD from his bank to crypto exchanges each month (must be doing well!). But now, with the new restrictions, he’s left wondering: what should he do with that money if he can no longer send it to crypto exchanges?

Some suggested moving the funds to other banks and then transferring them to exchanges from there. But that turns out to be just as problematic. Australian HSBC division, for example, had already introduced a full ban on sending money to crypto exchanges back in July 2024.

Both ME Bank and HSBC — like many other banks around the world — frame such restrictions as a protective measure for their customers. According to them, sending money to a crypto exchange is inherently risky.

But that raises the big question: where is your money really more at risk — in a traditional bank or on a cryptocurrency exchange?

The Risks of Crypto Exchanges

At first glance, it might seem obvious that crypto exchanges are more dangerous than banks-and there are plenty of arguments to support that view. Here are some of the most common concerns raised by users:

Frequent hacks and large-scale thefts

Crypto exchanges have a long history of security breaches and massive fund losses. The most infamous example is Mt. Gox: back in 2014, it was the largest exchange in the world, but after discovering that hundreds of thousands of bitcoins had gone missing-worth hundreds of millions of dollars at the time-it filed for bankruptcy. Even a decade later, victims are still waiting for full compensation.

Since then, other major incidents have followed:

- Bitfinex (2016): ~120,000 BTC stolen

- Coincheck (2018): ~$530 million in NEM tokens

- Binance (2019): ~$40 million hacked

- KuCoin (2020): ~$280 million lost

- Bybit (2025): ~$1.4 billion in ETH and other crypto assets drained from the platform by hackers

In most of these cases, it wasn’t the exchange’s own money that was stolen — it was user funds.

Sudden account freezes without explanation

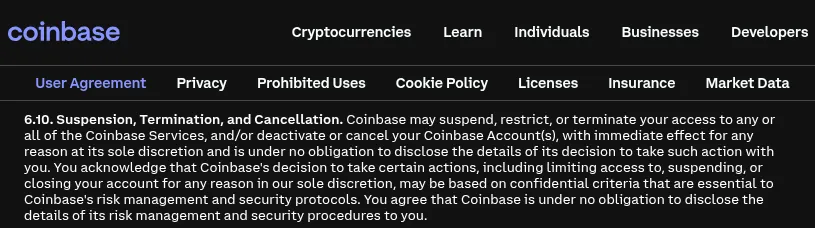

Many exchanges reserve the right to lock user accounts without prior notice or explanation. For example, Section 6.10 of Coinbase’s terms of service explicitly allows them to freeze funds at their own discretion.

In late 2024, several Coinbase users went public, saying their accounts had been frozen for months — or even years — without clear reasons. Coinbase responded by citing anti-fraud protocols and claimed that such freezes are rare, only triggered by legal requirements or policy violations. However, the real issue lies in how those violations are determined: many platforms reserve the right to make that call unilaterally, and they’re under no obligation to provide proof.

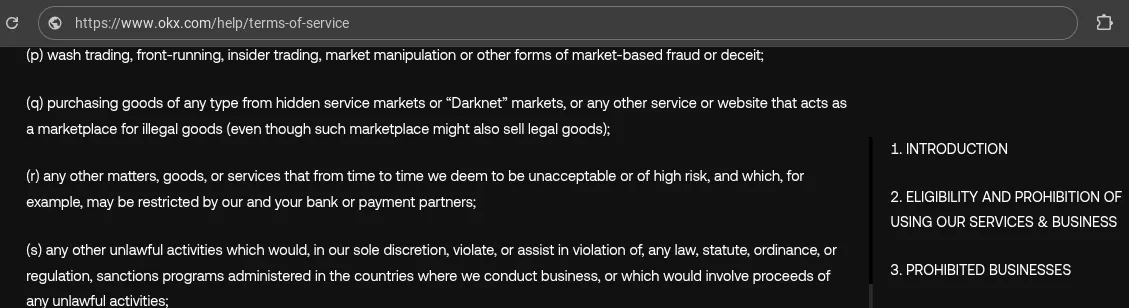

Other platforms, like OKX, list broad categories of “prohibited businesses.” One such category (point ‘s’) is so vague that it could apply to a wide range of users, making it easier for exchanges to justify freezing funds.

Another common issue: users being asked to provide documents that are either unreasonable or impossible to obtain. One Binance customer shared how his account was frozen until he could verify the source of all deposits ever made — including from old crypto wallets he no longer had access to. Unable to meet those demands, his account remained locked.

No insurance on user funds

What happens if an exchange disappears along with its customers’ money? Cases like Livecoin, Bitforex, and the earlier WEX incident show that in many instances, this means a total loss. A notable example is QuadrigaCX: when its founder suddenly died in 2019, he took the passwords to the cold wallets with him — leaving users without access to about $190 million in funds.

Some exchanges offer limited safeguards. Coinbase, for example, holds customer USD balances in custodial bank accounts with FDIC insurance up to $250,000. But that insurance only applies to USD balances — and only if the partner bank fails, not if Coinbase itself goes under. So, if Coinbase were to declare bankruptcy tomorrow, customers would have to rely on liquidation proceedings in court. And even then, having enough assets to cover all liabilities doesn’t guarantee full repayment — just ask the users still waiting on FTX.

In short, when you hold funds on a crypto exchange, you’re taking on full credit risk of that company. You’re placing your trust in the integrity and competence of the people who run it. High returns offered by exchanges — through staking programs or “earn” products — are essentially a premium for taking on that risk.

The Risks of Banks

Let’s take a look at the same risk factors — but this time, through the lens of traditional banking. Do banks actually offer better protection from the issues that plague crypto exchanges?

Protection from hacks and theft

Crypto exchanges offer a range of security features to protect user accounts: two-factor and even three-factor authentication, IP whitelisting, withdrawal address whitelisting, time-locks after password changes — you name it. Each platform has its own security toolkit.

Banks? Not even close. Their technical defenses often lag behind.

So why don’t we hear about hackers stealing from banks as often as from exchanges? The reason isn’t better protection — it’s the structure of the banking system itself. Bank balances are just digits in a centralized database, not real money. If a criminal somehow gains access to your account, what can they do with it? Sure, they might be able to transfer funds to another account, but that’s easily traceable. Converting stolen funds into something spendable, like cash, is much harder — sometimes even legitimate customers struggle to withdraw large amounts of cash. Remember that recent case in the UK where a bank refused to let a man withdraw money for a motorcycle purchase until he could provide proof?

Now, a bank might argue: “A hacker could send the stolen money to a crypto exchange — this is why we block those transfers.” But let’s not forget that crypto exchanges, like banks, also enforce strict KYC procedures. If you send illicit funds to a KYC-compliant exchange, you’re just as likely to get caught as if you sent them to another bank.

Some might argue that criminals can buy verified exchange accounts using stolen identities. But the same applies to banks — black markets for KYC’d bank accounts exist too. Yet for some reason, no one’s proposing a monthly cap on transfers to banks, like they do for crypto. Why? Probably because such restrictions would be illegal in many countries.

Account freezes and blocked funds

Worried about crypto exchanges freezing your assets? Banks do it too - and arguably more often. The difference is, banks usually do it in coordination with government agencies, making them harder to challenge.

Here are a few examples:

- Cyprus (2013): During a financial crisis, banks were shut down for nearly two weeks. Cash withdrawals were strictly limited, and large deposits were forcibly converted into bank shares.

- Canada (2022): During the “Freedom Convoy” protests, the government froze bank accounts used to collect donations for participants.

- Ukraine (2022): Following the Russian invasion, the Ukrainian government froze all bank accounts held by Russian and Belarusian citizens. The only permitted use of those funds was donations to Ukraine’s defense effort.

And even in ordinary circumstances, banks are legally obligated to freeze any transaction they deem “suspicious” under anti-money laundering laws. Enforcement levels vary by country, but such freezes are common globally. Personally, I’ve had funds frozen in banks across three different countries on that basis alone.

Then there’s the whole issue of transferring crypto profits into your bank account. In the UK, for example, some banks — including Lloyds and NatWest — have reportedly frozen accounts simply because clients moved money from crypto exchanges. You don’t even need to be doing anything shady — just cashing out your coins can be enough to trigger suspicion.

Deposit insurance

Many countries offer government-backed deposit insurance for bank accounts, which provides a layer of safety. But this protection has limits — and often doesn’t cover high-net-worth individuals.

Remember the man who transfers AUD 40,000–80,000 per month from their bank to crypto exchanges? If he kept that money in a bank account instead, would it be fully insured? Unlikely. In Australia, the deposit insurance cap is AUD 250,000.

This isn’t just a theoretical concern. When the European MiCA regulations were being finalized, Paolo Ardoino, CEO of Tether, explained why his company couldn’t comply with the requirement to store 60% of reserves in EU banks: if one of those banks collapsed, Tether would only be guaranteed €100,000 in insurance — yet their reserves total tens of billions. That level of risk is unacceptable when you’re managing funds meant to be redeemed on demand.

So What’s the Smart Move?

When I first heard that banks were restricting or outright blocking transfers to crypto exchanges, my gut reaction was: \n“If you can move money from an exchange to a bank, but not the other way around — maybe it’s actually safer to keep funds on the exchange.”

But then I remembered that many exchanges no longer support fiat withdrawals to banks. So if you can’t get your money out either way, what difference does it make?

Here’s the reality I’ve come to accept:

- Keep only what you need for near-term daily expenses in the bank. If paying with a debit card is more convenient than using cash, great — that’s a practical use case.

- Hold funds on an exchange only if you’re actively trading — for example, if you’re using leverage and need collateral on the platform. In that case, just keep the minimum required to cover short-term price swings.

In both cases, the key question is: “Can I afford to lose this amount?”

If the answer is yes — go ahead and send it to the bank or the exchange. If not — don’t risk it.

I’ve noticed that even many clients of Rabbit Swap who make large-volume exchanges tend to split their funds into smaller portions — clearly to avoid sending more than they’re comfortable risking in one go. And honestly, I respect that approach.

Rabbit Swap has never scammed anyone — not once. But the beauty of crypto is that it lets you stay in control of your money. So why not take advantage of that and keep personal custody over any amount you consider truly important?

The most rational strategy? Self-custody for critical funds. Yes, at rabbit.io we’re ready to process any amount without limits — but we fully support clients who set their own risk caps and choose to keep their money under their own control, rather than trusting someone with more than they’re willing to lose.