What’s Behind the Hype Around Hyperliquid?

This week — on Bitcoin Pizza Day — the prices of three cryptocurrencies hit their all-time highs in dollar terms. One of them was Bitcoin, and the other two were HYPE and WBT.

- Everyone knows what Bitcoin is: the most reliable store of value that has changed how millions view the financial system.

- WBT is straightforward too — it’s the native token of one of the crypto exchanges.

- But what is HYPE? Is it yet another exchange token? Or something more?

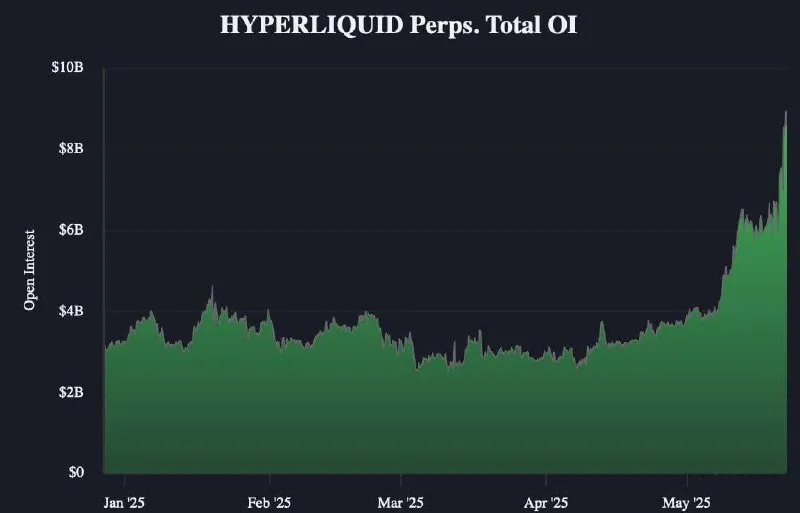

The buzz around this boldly named token and the platform behind it, Hyperliquid, has reached a point where it feels like a whole new chapter in the history of crypto — a shift on par with Satoshi Nakamoto’s invention. Maybe it’s no coincidence that Hyperliquid, without advertising or venture funding, has quickly climbed into the top five derivatives platforms by open interest.

Source — https://x.com/Neda4_

Let’s dig in.

Hyperliquid — The Return of CeDeFi

Years ago, Changpeng Zhao promised to build CeDeFi — a decentralized finance system running on a centralized platform. At that time, Binance Smart Chain seemed poised to make it real: every validator on the blockchain was directly linked to Binance, and the decentralization of dApps running on it was always limited by this central control. Later on, BNB Smart Chain evolved into a more decentralized model, and the idea of CeDeFi seemed to fade away.

But at the end of 2024, those same principles found new life in Hyperliquid. And so far, the execution has been impressive.

How Hyperliquid Works

Hyperliquid is often compared to DEXs built on specialized high-speed trading blockchains: dYdX v4, Injective, Sei. But to me, that’s not quite accurate. All of these platforms focus on decentralized governance, while Hyperliquid doesn’t offer anything of the sort.

A more accurate comparison might look like this:

- Imagine you deposit funds on a derivatives exchange you’re used to, like Binance.

- The exchange doesn’t just record your deposit as a number in your account — it issues you tokens in its own blockchain.

- In that same blockchain, the exchange records all the orders you place and all the trades you execute.

- When you withdraw funds from the exchange, you give back its internal tokens (also done as a transaction in its internal blockchain), and it sends you tokens on an external network.

That’s exactly how Hyperliquid works. It’s a fully centralized, custodial trading platform whose main difference from competitors like Binance, Bybit, or OKX is full transparency: every action on it — deposits, withdrawals, orders, trades, liquidations, and more — is recorded in an open blockchain.

But there’s one caveat: while bigger competitors accept deposits in various cryptocurrencies across different networks, Hyperliquid only accepts deposits in a single token and on a single network.

Who Holds Your Assets

The first step for any new Hyperliquid user is depositing USDC from the Arbitrum network. These funds are sent into a bridge, where they’re locked up by a multisig controlled by the Hyperliquid blockchain validators. In return, you receive a balance within Hyperliquid’s own network. But this balance isn’t the actual USDC you deposited — it’s a promise that the exchange will pay it back to you. If you want to get back your original funds, you have to wait until two-thirds of the validators sign off on the withdrawal. If they don’t sign, you get nothing. You hold the private key to your wallet, but the door itself is controlled by a team of sixteen validators.

The Hyperliquid blockchain is really fast: blocks are finalized in fractions of a second, and the order book updates faster than a WebSocket can blink. The price of that speed is an exclusive club of validators. Until March 2025, there were just four of them, and now there are sixteen. Most are nodes operated by the Hyperliquid Foundation. They’re the ones who decide which transactions go into a block, how they’re ordered, and, if needed, when to end the market drama manually.

The Limits of Validator Power

A perfect example of how validators can manually end the “drama” came in March 2025, with the memecoin JELLY. A speculator had driven the price so far that the platform’s insurance pool was about to be drained by massive liquidations. Validators intervened immediately: they unanimously voted to delist the JELLY futures market on Hyperliquid, halted all trading, and forcibly closed all positions at a pre-set price. In practice, this wiped out the market’s profits and losses entirely. All open positions were forcibly closed at $0.0095 — exactly the entry price of the short position that had triggered the price spike.

This was the essence of the CeDeFi return I mentioned earlier in this section: Hyperliquid applies some principles of decentralized finance — primarily transparency — on a fully centralized platform. The whole community watched the JELLY drama unfold in real-time. Many were outraged that a team proclaiming “decentralized on-chain strategy” and DeFi principles would just take millions in USDC away from a short-selling trader.

But notice: the platform’s team never once claimed Hyperliquid was a “decentralized exchange.” They said it incorporated some decentralized principles, yes. “Code is law” — no. Final authority always rests with the validators. This, incidentally, is exactly what Changpeng Zhao once called CeDeFi.

Reasons for Hyperliquid’s Success

Proponents of Hyperliquid say it’s the first real merging of a high-volume, retail-focused on-chain trading platform and a general-purpose smart contract platform (EVM). But I think EVM has little to do with Hyperliquid’s success. The real driver is the network effect:

- The more active users there are, the higher the liquidity and the larger the trading volumes become.

- High liquidity and large volumes attract new users in turn.

On top of that, Hyperliquid has some serious advantages over both decentralized and centralized exchanges. Compared to DeFi DEXs, it offers much faster order processing. Compared to CEXs, it doesn’t collect users’ personal data.

Hyperliquid also cleverly carried out its HYPE token airdrop for early users. With no early investors, the platform was able to allocate 70% of its tokens for community rewards. Of this, 31% (or 310 million HYPE) was given out in the first airdrop to more than 90,000 addresses. At launch, this was valued at $1.2 billion — today, it’s nearly $12 billion. This massive airdrop immediately created a large, engaged user base that keeps actively trading on the platform, seeing the rewards firsthand. And new users keep joining in, hoping for future rewards — for which another 389 million HYPE has been reserved. From there, the aforementioned network effect and the platform’s unique advantages kick in.

Why the HYPE Token Keeps Rising

Usually, cryptocurrencies distributed for free in airdrops quickly get dumped, and their price plummets to the floor. But HYPE has defied that trend. Since the airdrop, its price has grown nearly tenfold. So what’s going on?

The price of any asset depends on the balance of supply and demand. Let’s look at where each side comes from in the case of HYPE.

Supply side

- At first, only users who received the tokens from the airdrop could sell them.

- There were no early investors holding a huge chunk of tokens.

- Tokens allocated to the team can’t be sold yet — they’ll be unlocked only in 2027–2028.

- Later on, validators who earn HYPE for confirming blocks also began to sell.

Demand side

Here’s where things get more interesting. HYPE doesn’t need organic demand from users — purchases of HYPE are automatically triggered whenever someone pays trading fees to the platform.

Let’s take a closer look at how that works:

- Users pay trading fees in USDC.

- 54% of these USDC fees go to rewarding validators.

- Since validators are paid in HYPE, 54% of the USDC fees are used to buy HYPE from the market.

In other words, there’s a hidden gas fee baked into the trading fee. Users don’t have to buy HYPE directly to trade — but as trading volumes grow, so does the indirect demand for HYPE.

So long as trading volumes keep growing, demand for HYPE will rise too. And with that, the price can keep going up. But if trading volume growth slows — or worse, starts to decline — the exchange team will have to find other ways to create demand to support the price.

At present, the rising price itself attracts speculators who join in the buying, helping push the price even higher. But when growth eventually stops, these same speculators will likely start dumping tokens, adding more downward pressure.

So, it’ll be interesting to watch what happens to HYPE next. As of now, it hasn’t just hit a new all-time high on Bitcoin Pizza Day alongside Bitcoin — it has kept setting new highs every day since. Hyperliquid seems to be very good at drawing attention to its token. And if HYPE has caught your interest, you can find it on rabbit.io, where you can swap any of the thousands of supported cryptocurrencies for this token.