The Countdown to MiCA: Is the Crypto Industry Ready?

Opinions on MiCA vary widely in crypto circles. Some complain that it creates excessive bureaucratic hurdles that stifle business growth. Others welcome it as the world’s first comprehensive, clearly defined set of rules that allow businesses to operate in a structured, trouble-free environment.

Anyone intending to continue doing business in Europe, however they may feel about the European crypto-market regulation, must adapt their operations to these rules. After all, the final implementation date is just two weeks away — December 30, 2024.

Who Will Have to Adapt — and How?

The Markets in Crypto-Assets (MiCA) rules were approved by the European Parliament on April 20, 2023, and entered a transitional phase after their publication in the EU’s Official Journal on June 9, 2023. On June 30, 2024, the rules for stablecoin issuers and sellers began to apply. As of December 30, 2024, absolutely all providers of crypto-asset services will fall under MiCA’s scope.

Who are these service providers? Payment operators, remittance companies, and exchanges immediately come to mind. But MiCA’s definition of a “crypto-asset service provider” is so broad that virtually every professional participant in the crypto industry fits the description — even a crypto consultant.

This wide net means that if your professional activities involve cryptocurrencies and have any ties to the European Union, then as of December 30, you or your employer must meet MiCA’s requirements.

MiCA emphasizes that its rules are designed to protect investors, counter money laundering, and foster a transparent business environment. But many businesses in the crypto sector have already implemented investor protections, anti-money-laundering measures, and internal compliance departments well before these EU-specific regulations. The main problem, as MiCA takes full effect, isn’t that crypto companies must introduce transparency measures or strengthen investor protections. The primary challenge lies in the need for “authorization” under the newly introduced MiCA rules.

After December 30, 2024, anyone planning to offer crypto services in EU countries must be authorized in one of those states. Article 59 of MiCA states:

“A person shall not provide crypto-asset services, within the Union, unless that person is: (a) a legal person or other undertaking that has been authorised as crypto-asset service provider in accordance with Article 63…”

Furthermore, it explains that national competent authorities issue, refuse, or revoke such authorization. So even though the word “license” doesn’t appear in MiCA, the concept of “authorization” effectively functions as a licensing process required for providing crypto-related services in the EU.

Up until now, not all EU countries have established procedures for this type of licensing. Spain has officially postponed it until December 2025, and about a quarter of EU member states simply haven’t managed to roll out the process in time. Because of this, crypto companies asked the European Securities and Markets Authority (ESMA) to delay the remaining MiCA provisions by six months. Their request was denied. As a result, a complicated situation has emerged where many crypto companies might have to halt their European operations on December 30. This predicament was discussed at an ESMA meeting on December 11, but no press release followed. Most likely, that silence suggests no changes to the effective date of MiCA.

What Happens if You Ignore MiCA? The Stablecoin Example

Can you keep doing business while ignoring the EU’s requirements? Strangely enough, there are examples suggesting that you can — at least for a while. These cases involve offering stablecoins in the EU.

Strict stablecoin regulation, affecting both the structure of reserves and the geographic location of assets, became one of MiCA’s most contentious issues. Since June 30, 2024, issuers are required to hold at least 30–60% of their reserves in European banks. Tether’s CEO, Paolo Ardoino, initially criticized these measures, arguing that they introduce “a large systemic risk.”

MiCA requires stablecoin issuers to ensure that users can redeem their tokens at any time for the underlying assets backing them — be that dollars, euros, or another fiat currency. But if the money is held in a European bank, that bank might refuse to release it, citing anti-money-laundering efforts or liquidity issues. European banks have faced liquidity challenges for many years, and increasing their role in stablecoin operations could be dangerous. In the event of a bank’s bankruptcy, only €100,000 is guaranteed to depositors, while the largest stablecoins’ capitalizations run into tens of billions.

Major players like Tether initially presented their flagship stablecoins as products not aligned with MiCA. USDT’s reserves have not been transferred to European banks, yet European users can still trade USDT on exchanges (the largest being Bybit) and through payment services (like BitPay). In the five and a half months since unregulated stablecoins could no longer be legally offered, none of the providers have faced sanctions.

The European bureaucratic machine may be slow, but it’s not completely ineffective. Sooner or later, businesses that don’t comply with MiCA will have to shut down their non-compliant operations. That’s why all those offering stablecoins to a broad audience are, in one way or another, searching for solutions.

Instead of overhauling their entire business for a relatively small European market, companies are considering launching separate, small-cap stablecoins that formally meet regional regulatory requirements without changing their global operational model.

For example, Binance introduced a new asset called Binance Credit (BNFCR). In Binance’s USDⓈ-M futures trading mode, PnL, margin, and fees are displayed as BNFCR credits. This was done so that European users can continue accessing futures trading, even if they’re prohibited from using standard stablecoins. Any stablecoin balance (USDT, USDC, FDUSD) in the futures wallet can be converted to BNFCR at a 1:1 ratio at any time. When transferring between the futures wallet and other wallets in this mode, only BTC, ETH, and BNB can be used. BNFCR cannot be withdrawn directly, but it can be converted into BTC, ETH, or BNB prior to withdrawal.

Coinbase, for its part, restricted access to many stablecoins for European clients — but only starting December 13, 2024. The exchange encourages users to convert non-licensed stablecoins into USDC or EURC, which have the necessary approvals. (Circle, USDC’s issuer, has already taken steps to legalize its activities in the EU by obtaining an Electronic Money Institution (EMI) license. This status lets them continue operating within Europe’s legal framework.)

Other platforms, such as OKX, are planning to expand the number of euro trading pairs to give clients alternatives to stablecoins as the regulatory landscape shifts.

All these changes are happening right now, while stablecoin offering rules are already effective. The experience with stablecoin regulation under MiCA shows that, during the first few months, businesses can continue operating much as they always have, ignoring the new rules. But over time, the business model will have to adapt to MiCA’s requirements or leave the European market.

What Should Customers Expect After December 30, 2024?

If the stablecoin example is any indication, not much may change at first. Crypto companies that offered their services to the European market will likely continue to do so. Smaller companies focused on the European market, or even more local ones, often already have offices in European countries and have gone through something similar to what MiCA now calls “authorization.” And global players (like Bybit and Tether) might keep running their operations as usual.

Tether has announced plans to discontinue EURT, but it cited low user interest in the token as the reason. Blockchain metrics confirm the tepid interest: while USDT’s market cap exceeds $140 billion, there’s only about €25 million worth of EURT in circulation.

Just in case, Tether has also invested in Quantoz, a company that issues stablecoins according to MiCA’s rules. If needed, Tether can maintain access to the European market through them. Other global businesses might take similar steps.

Ultimately, we might see Europe develop its own localized crypto industry — a kind of lagoon, separated by proxy solutions from the mainstream global crypto economy.

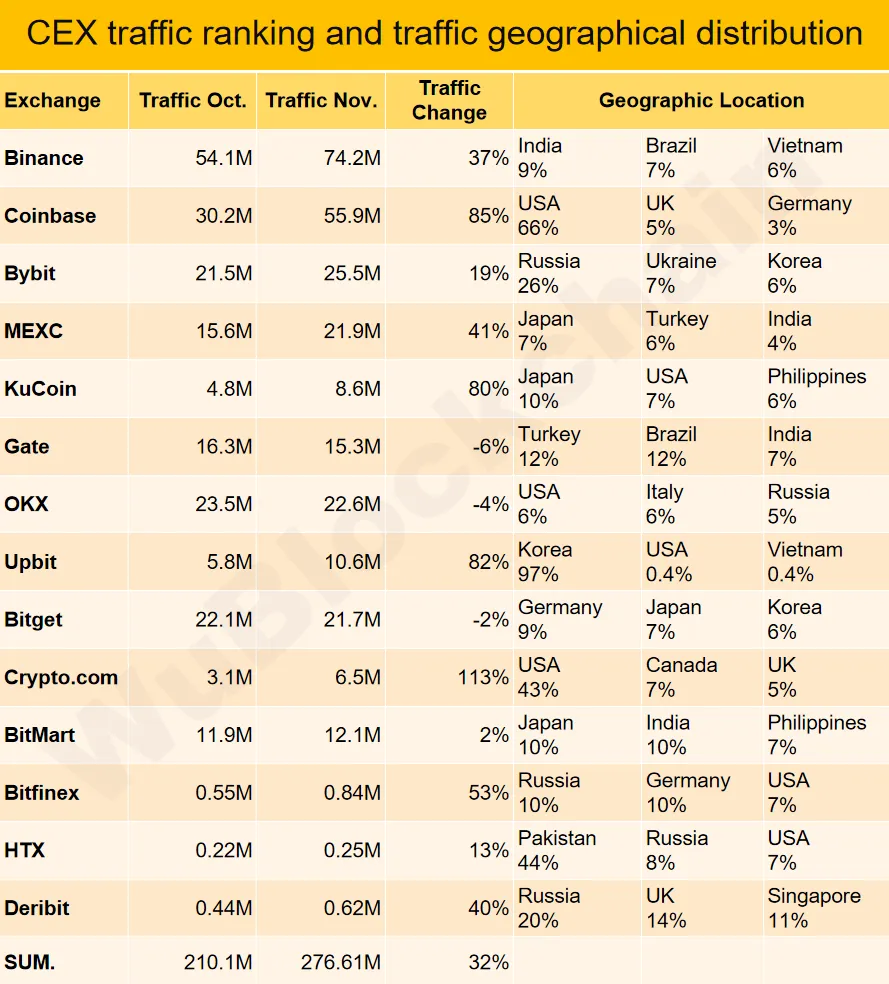

The biggest threat for customers is that banks may refuse to credit funds coming from “unauthorized” exchanges or other crypto services. On one hand, exchanges have an incentive to solve this problem for their European clients. On the other hand, if we look at the share of European countries in the traffic of the largest exchanges, Europe rarely appears in their top three sources of volume, according to Wu Blockchain.

Source — Wu Blockchain

It’s unlikely that solving European clients’ banking problems will become a top priority for exchanges. If push comes to shove, exchanges can simply offer their own payment solutions, such as debit cards (like the Bybit Card), which would further separate crypto flows from fiat money. But this separation isn’t necessarily a disaster. At Rabbit Swap, we’ve long operated within a paradigm that keeps crypto and fiat transactions distinct. Our clients swap one cryptocurrency for another freely, without ever needing to step into the traditional banking system.

Is This Permanent?

Many crypto businesses show strategic flexibility, moving across jurisdictions in search of the friendliest regulatory climate. When the U.S. regulatory environment was uncertain — where the SEC’s arbitrary interpretations effectively strangled many crypto businesses — some American companies began looking to the EU, hoping MiCA would provide clear, stable rules.

But MiCA is a highly restrictive set of rules — prohibitive in some aspects. If the U.S. introduces more permissive laws (which is entirely possible), the EU may have to rethink MiCA. Otherwise, as regulation tightens and requirements for reserves and licensing become more onerous, the crypto industry might shift back to the U.S. Right now, thanks to MiCA, Europe leads the world in setting up a legal framework for the crypto business. But that could change quickly, leaving the region behind in global competition.

The EU has another piece of legislation where it’s ahead of the curve: the Payment Services Directive 3 (PSD3). It will allow licensed non-bank financial companies to open correspondent accounts at European central banks. This could create crypto-friendly accounts backed by central bank risk — not just a regular bank’s limited guarantee of €100,000. Such opportunities might attract even the most conservative segments of the financial markets to crypto.

But PSD3 may only come into force in 2027. To implement PSD3, the MiCA framework is needed first, as it establishes the foundation for licensing crypto companies that could eventually open central bank accounts. By the time PSD3’s real-world benefits become available, however, MiCA might have already driven away major crypto businesses from Europe. Those businesses have more interest in serving clients from regions where crypto solves pressing financial problems rather than creating new ones.

Conclusions

How has the crypto industry prepared for MiCA’s final implementation? In truth, it hasn’t, not really.

- When it comes to the core issues MiCA was designed to address — AML, transparency, transaction security — European companies have long been up to standard without any new rules.

- The main adjustment now is to the bureaucratic procedures, and many countries aren’t ready for that yet.

- The stablecoin experience demonstrates that under MiCA, it’s still possible to continue operating as before, ignoring the new rules for a while.

- Time isn’t on MiCA’s side. In the foreseeable future, we might see a more liberalized U.S. crypto law. The question remains: what will ultimately adapt to what — the crypto industry to MiCA’s requirements, or MiCA’s framework to the global realities of crypto?