Stablecoin Risks

Are stablecoins safe to use? Are they really as stable as claimed? What incidents have occurred involving stablecoins, and what were the consequences for stablecoin holders?

In this article, I’ll answer all these questions. While stablecoins are undoubtedly convenient assets, not fully understanding their associated risks can lead to significant losses.

How Stablecoins Are Used Today

Stablecoins have become essential tools for many crypto enthusiasts, serving as:

- a primary means of transferring funds,

- a preferred method of payment,

- a source of passive income through DeFi pools,

- and even a key instrument for storing savings.

If you need to transfer money from one country to another, you can simply buy stablecoins in one place and sell them in another, facilitating an international transfer. While you could do this with any cryptocurrency (BTC, XRP, or even DOGE), stablecoins maintain a fixed exchange rate, eliminating the risk of depreciation between buying and selling.

Consider two companies involved in cryptocurrency businesses — one using Ethereum and the other Solana. How should they transact with each other? Stablecoins that operate on both networks are ideal since their value doesn’t depend on the fluctuations or technical issues of Ethereum or Solana.

Lending and liquidity pools allow investors to earn interest in various cryptocurrencies. But earning a modest 5% yield in stablecoins often looks safer than a seemingly attractive 50% yield in a volatile cryptocurrency that might lose half its value within a year.

Keeping savings in volatile crypto assets can also be daunting. Take a look at the price dynamics of major cryptocurrencies over the past three months:

Observing this volatility, it becomes clear why many people prefer stablecoins for storing their savings.

Stablecoins appear to retain all the key advantages of cryptocurrencies:

- You can securely store them yourself without relying on banks or other institutions with questionable reputations.

- You can easily transfer them without needing approval or oversight from intermediaries.

- Transactions are transparent, allowing counterparties to independently verify payments.

And crucially, they don’t have the key disadvantage of unpredictable price fluctuations.

But let’s take a closer look at stablecoins.

Fiat-backed Stablecoins (USDT, USDC, and others)

Tether (USDT)

Tether, the oldest and largest stablecoin, has frequently lost its dollar peg during market turmoil. The most notable incident occurred on October 15, 2018, when amid rumors about reserve and banking issues, the price of USDT dropped sharply to $0.85.

USDT/USD chart from 2018. Source: Investing.com

During the height of panic, investors rushed out of Tether and into Bitcoin, temporarily driving Bitcoin’s price upward as it absorbed USDT’s loss of value.

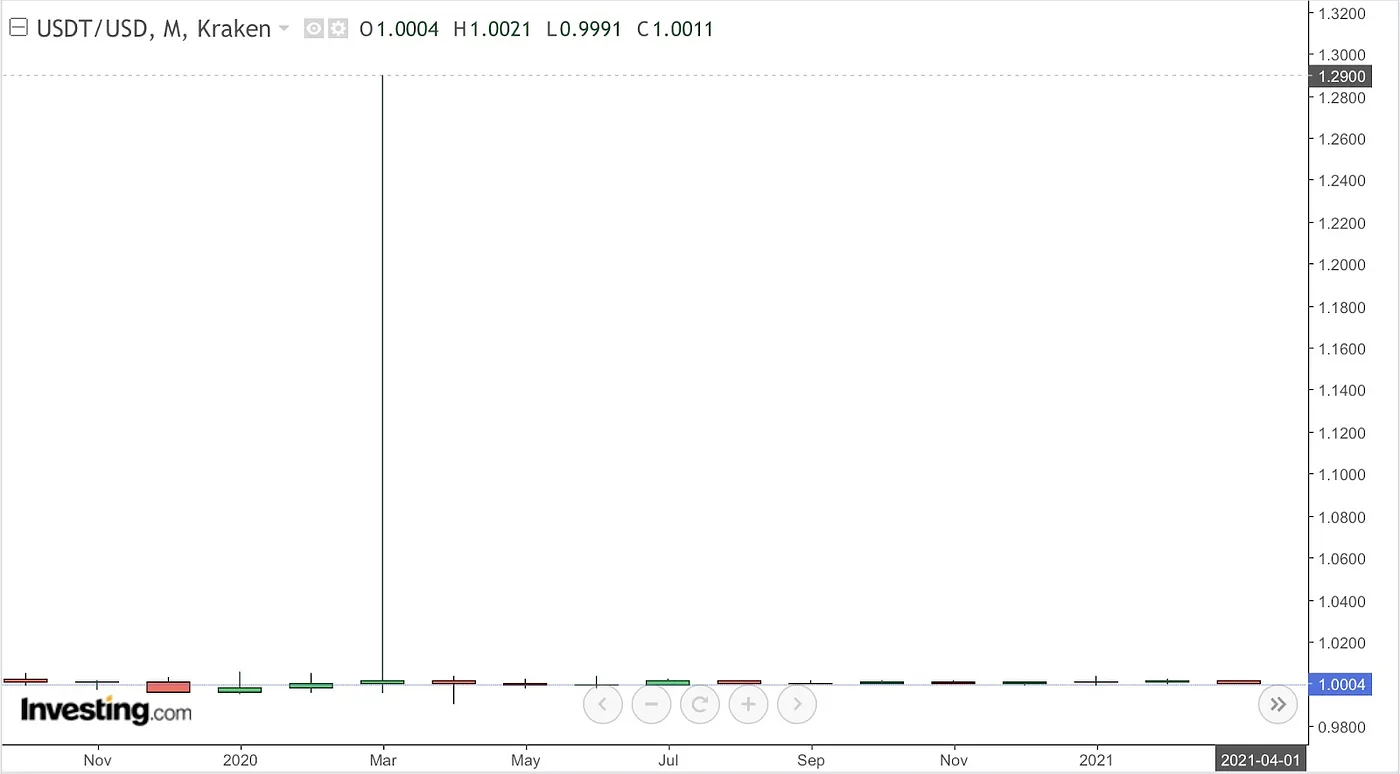

Interestingly, Tether’s peg can also break when issues arise in the broader crypto market. USDT is widely used as collateral in leveraged trading positions, which increases demand sharply during market downturns, occasionally pushing USDT’s price above one dollar. For example, in March 2020, amidst the COVID-19 financial panic and liquidity shortages, USDT traded as high as $1.29.

USDT/USD chart from 2020. Source: Investing.com

USD Coin (USDC)

USDC was long perceived as a reliable, regulated stablecoin, but it too experienced significant turbulence. On March 10–11, 2023, following news that $3.3 billion of Circle’s roughly $40 billion reserves were trapped in the troubled Silicon Valley Bank, USDC lost its peg and fell to an all-time low of approximately $0.88. Investors panicked and rushed to redeem USDC, withdrawing over $10 billion worth of tokens in a matter of days.

This temporary depegging occurred largely because the problems emerged on a Friday, after banks had already closed, and normal redemptions could only resume on the following Monday. As a result, many holders hurried to sell USDC at discounted prices. Circle publicly reassured investors that regular redemption operations would resume once banks reopened. Indeed, by March 13, after intervention from U.S. regulators, USDC restored its 1:1 parity. Nevertheless, this event highlighted that even fully backed stablecoins remain vulnerable if investors doubt the accessibility of reserves.

Paxos Stablecoins (HUSD and BUSD)

Paxos issued stablecoins for crypto exchanges such as Huobi and Binance. On its website, Paxos stated that every HUSD token, issued for Huobi, was backed by one dollar held in Paxos’s bank account. Despite this assurance, HUSD suffered several significant incidents in 2022. In August, the token briefly fell to around $0.82, and after being delisted from Huobi in October, it collapsed sharply to $0.28. Although it partially recovered afterward, investor confidence was severely undermined, and the project effectively ceased operations.

In 2023, the Binance-branded BUSD was banned by regulators. Currently, BUSD tokens can still be redeemed for dollars directly via Paxos’s platform. However, the fate of HUSD has raised doubts about whether such redemptions will always remain available.

What’s the Problem with Fiat-backed Stablecoins?

In theory, fiat-backed stablecoins should always be redeemable at face value, ensuring their price remains stable around $1. If the market price dips below the peg, arbitrageurs should quickly buy the discounted tokens and redeem them directly with the issuer at 1:1, restoring equilibrium.

But in reality, things aren’t so straightforward:

- Redeeming tokens directly requires a registered and verified account with the issuer, which isn’t accessible to everyone. Paxos, for example, doesn’t serve residents of certain countries. Tether explicitly states that its redemption obligations are “personal,” meaning if no USDT tokens were directly issued to your account, Tether has no obligation to redeem tokens for you personally.

- Some issuers (e.g., Tether) only allow redemptions for large clients, typically requiring minimum amounts (such as $100,000 worth of USDT).

- Even when issuers claim full backing, if transparent and independently verified audits aren’t provided (as often criticized with Tether), arbitrageurs may distrust the reserves and refrain from intervening, fearing delays or partial redemptions.

- Fiat-backed stablecoins also face risks from banking and custodial issues. Issuers store billions of dollars in bank accounts and treasury securities; bank failures or frozen accounts pose a direct threat to stablecoin holders.

- Regulators can mandate blocking specific addresses. After the U.S. imposed sanctions against Tornado Cash, Circle froze around $75,000 of USDC on sanctioned addresses, setting a precedent for direct regulatory interference in stablecoin transactions. Such freezes have become common; in March 2025, Tether even froze wallets of a cryptocurrency exchange holding customer funds.

All these factors complicate arbitrage opportunities, making fiat-backed stablecoins far less stable than their theoretical design suggests.

Crypto-Backed Stablecoins (DAI and Others)

DAI

“Black Thursday” (March 12, 2020) is a textbook example of the vulnerabilities inherent in crypto-backed stablecoins during extreme market shocks. On that day, the price of Ethereum (the primary collateral asset behind DAI) plunged by about 47%, following the global financial panic caused by COVID-19.

ETH/USD chart from 2020. Source: Investing.com

The Ethereum network became heavily congested, causing gas fees to skyrocket and resulting in the malfunctioning of MakerDAO’s price oracles. When the protocol started mass liquidation of devalued collateral, network congestion caused many auctions to fail. Some liquidators won collateral lots paying 0 DAI, effectively acquiring ETH for free. This glitch created a deficit in MakerDAO, leaving around 4.5 million DAI undercollateralized. Simultaneously, demand for DAI surged on secondary markets (since DAI was required to participate in lucrative liquidation auctions), causing its price to spike well above $1.

The protocol survived the crisis by quickly issuing and selling new MKR governance tokens, raising approximately $5.3 million to cover the deficit. The borrowing fee (stability fee) was temporarily reduced to zero to encourage more DAI minting and bring the price back toward $1. Although the system stabilized, the reputational damage was severe. A group of affected users filed a lawsuit against MakerDAO, seeking compensation for $8.3 million in losses. Following this event, MakerDAO diversified its collateral assets, notably adding USDC for increased stability. The incident also prompted MakerDAO to enhance its protective mechanisms, such as reserve funds and the Peg Stability Module, designed to facilitate automatic 1:1 exchanges between DAI and other stablecoins.

However, incorporating USDC led to a different type of crisis in 2023. On March 11–12, when USDC faced its own banking-related troubles, DAI’s value dropped significantly due to USDC making up approximately half of its collateral reserves. When USDC’s price fell to about $0.90, DAI also lost its peg, dropping even lower to around $0.86.

DAI/USD chart from 2023. Source: Investing.com

This reliance on a centralized asset (USDC) exposed the supposedly decentralized DAI to risks from traditional banking systems. Although DAI quickly returned to parity after USDC recovered, users experienced a brief period of uncertainty, raising concerns about the stablecoin’s future reliability.

Additionally, after OFAC sanctioned Tornado Cash, Circle immediately froze USDC assets on affected addresses, complying with regulatory demands. Addresses holding DAI linked to Tornado Cash were also blocked by certain crypto platform interfaces. Though the problem was limited to individual platform interfaces, it made the MakerDAO community aware of a serious potential threat. If Circle could freeze USDC collateral at regulators’ request, significant portions of DAI’s collateral could become inaccessible instantly. Such an event could severely damage trust in DAI and lead to a sustained loss of the dollar peg.

In response, MakerDAO reduced its reliance on centralized and regulator-vulnerable assets by increasing the share of decentralized collateral and limiting USDC’s role. MakerDAO also implemented internal mechanisms to quickly adjust collateral allocation if necessary, mitigating the impact of future regulatory sanctions on DAI’s stability.

Other Problematic Cases

Other crypto-backed stablecoins have faced similar issues. For instance, the VAI stablecoin on Binance Smart Chain (from the Venus platform) consistently traded below $1 (~$0.80–$0.95) after its launch in 2021. It was easy to mint new VAI tokens but less profitable to redeem them, causing market oversupply. Eventually, Venus had to introduce fees and redemption restrictions to restore the peg.

Early experimental stablecoins also offer cautionary examples. BitUSD (from BitShares) and NuBits (NBT), both launched around 2014, were early crypto-collateralized stablecoins. BitUSD was backed by BTS tokens, and faced similar issues to MakerDAO when the collateral token (BTS) suffered price declines and liquidity shortages. By 2018, BitUSD permanently lost its dollar peg. NuBits attempted to maintain stability using Bitcoin reserves and additional tokens (NuShares). After initial success, it collapsed in 2016 when BTC reserves depreciated sharply, leaving NBT severely undercollateralized and trading well below one cent.

What’s the Problem with Crypto-Backed Stablecoins?

Crypto-backed stablecoins’ behavior under extreme market conditions remains unpredictable.

Their main vulnerability is the volatility and risk of collateral depreciation. To maintain a $1 peg, the value of the crypto collateral must consistently exceed the issued stablecoins by a significant margin. Sudden collapses in collateral value can quickly lead to insufficient coverage, destabilizing the token. Protocols typically prevent this through automatic liquidations — selling collateral when it falls below certain thresholds — but extreme conditions can overwhelm these mechanisms. During major market crashes, liquidity can evaporate, making it impossible to sell collateral quickly enough or at fair value, especially if blockchain networks become congested and liquidations are delayed.

Although crypto-backed stablecoins aim to offer a decentralized alternative, they carry economic risks distinct from fiat-backed tokens. The need for overcollateralization (often 150% or more) makes minting these coins capital-intensive. During high demand periods, supply shortages can drive stablecoin prices above $1. Conversely, if trust deteriorates, stablecoins can trade at discounts despite seemingly adequate collateral. Regulatory risks are lower compared to centralized issuers since smart contracts issue these tokens, yet still exist — especially when protocols use collateral that depends on traditional finance (as DAI does with USDC).

These examples demonstrate the structural complexity of maintaining stability. Decentralized stablecoin protocols often require careful calibration of fees, collateralization levels, and reserve rebalancing to keep token prices close to $1.

Algorithmic Stablecoins (UST, IRON, and others)

BAC and UST

Basis Cash (BAC) was an uncollateralized algorithmic stablecoin launched at the end of 2020. It tried to maintain its dollar peg by issuing additional tokens (“bonds”) that transferred volatility risk to bondholders. When the stablecoin’s price fell, the system issued additional tokens, using proceeds from their sale to buy back stablecoins, theoretically stabilizing the price. However, this model failed quickly — in early 2021, BAC permanently lost its peg and never recovered. Within a year, it traded at less than 1 cent.

Surprisingly, the creators of BAC went on to launch another similar project, TerraLabs’ UST stablecoin, a few months later. UST employed a similar algorithmic model but resulted in much greater damage. UST holders lost over $15 billion, shocking both regulators and the broader crypto market. The collapse of UST became a harsh lesson about how quickly an uncollateralized stablecoin can fail catastrophically.

Iron Finance

Iron Finance on Polygon issued the IRON stablecoin, backed 75% by USDC and 25% by its own volatile token, TITAN. By June 2021, IRON reached a circulation of around $2 billion, attracting significant attention due to its high-yield farming opportunities. However, when TITAN’s price began to decline, investors panicked and rapidly exited the protocol, selling both TITAN and IRON tokens en masse, which pressured both assets’ prices downward. The algorithm attempted to defend IRON’s peg by minting more TITAN tokens, but this only further exacerbated TITAN’s price collapse. A vicious cycle ensued: within hours, TITAN’s value plummeted almost to zero (rendering its share of the collateral worthless), and IRON lost its peg, trading as low as approximately $0.69. This incident famously impacted billionaire investor Mark Cuban, who publicly admitted losing money on TITAN, describing it as “the worst possible outcome embedded in their tokenomics.” The case underscored the danger of partial collateralization: even having 75% reserves in a reliable asset was insufficient when the remaining 25% rapidly collapsed.

Beanstalk (BEAN)

Beanstalk was a credit-based algorithmic stablecoin on Ethereum that aimed to maintain its peg through dynamically adjusting supply. It failed catastrophically due to a governance attack. In April 2022, attackers gained control over governance mechanisms and drained around $182 million worth of assets from the protocol. As a result, BEAN instantly lost about 86% of its value, effectively destroying the project within minutes.

What’s the Problem with Algorithmic Stablecoins?

Algorithmic stablecoins attempt to maintain a stable price without direct full backing by fiat or valuable assets. Instead, they rely on token minting/burning mechanisms, arbitrage opportunities, and economic incentives. The main risk they carry is the lack of intrinsic backing; if confidence is lost, the entire system can rapidly enter a “death spiral” of devaluation.

Typically, algorithmic stablecoin models rely on pairs of tokens: the stablecoin itself and a volatile reserve token (e.g., LUNA for UST or TITAN for IRON). If the stablecoin deviates from its peg, the algorithm mints or redeems reserve tokens to restore equilibrium. But if investors collectively lose confidence, simultaneous selling of both tokens accelerates price declines. This scenario, known as a “death spiral,” unfolds like this:

Stablecoin price falls → more reserve tokens minted to support it → reserve tokens lose value → further stablecoin collapse.

The absence of external reserve funds or sufficient collateral makes algorithmic models highly vulnerable to panic. While stable during normal conditions, in extreme situations these models have no way to balance supply-demand imbalances other than minting additional tokens (akin to “printing money”). Moreover, valuation errors or manipulation can occur easily. The peg relies on arbitrage, which might fail due to liquidity shortages or delays. Attackers can deliberately target these stablecoins by selling large quantities to trigger chain reactions. Technical exploits or bugs can also prove devastating: if attackers discover vulnerabilities enabling them to issue unlimited tokens, they can instantly flood the market with unbacked stablecoins, crashing their value completely.

Conclusions

All the cases discussed above share a common symptom: the stablecoin losing its peg to the dollar. However, beneath this common issue lie fundamentally different problems.

- Fiat-backed stablecoins face risks stemming from regulation and centralized custody. Holders’ assets can be directly affected by the actions or failures of the stablecoin issuer, the banks holding the reserves, or regulatory authorities. During crises, only the most daring arbitrageurs dare to buy these stablecoins, limiting their ability to quickly restore the peg.

- Crypto-backed stablecoins encounter similar issues but also face additional risks related to the volatility of their underlying crypto collateral and inadequately tested peg-maintenance mechanisms, which often fail unpredictably under extreme market conditions.

- Algorithmic stablecoins exhibit even greater vulnerabilities due to their purely automated peg-maintenance mechanisms.

Taken together, these examples suggest that stablecoins shouldn’t automatically be considered safer or more reliable than regular cryptocurrencies. Even their fundamental characteristic — price stability — is questionable.

However, there are examples of stablecoins that have thus far avoided incidents similar to those described above:

- USDe, developed by Ethena Labs, maintains a 1:1 peg to the dollar through collateralizing with ETH and simultaneously shorting ETH in futures markets.

- RAI is a stablecoin whose price isn’t pegged to exactly $1 but rather floats around $3 (typically between $2.9 and $3.1). RAI is solely backed by ETH and adjusts its interest rate dynamically to maintain price stability. This project demonstrated relative resilience, even during market stress like the March 2020 crash, when it adjusted without fully collapsing.

- Liquity USD (LUSD) is an Ethereum-based stablecoin that does not rely on DAOs or governance votes. Its parameters are entirely immutable, defined within the smart contract code. This eliminates risks related to governance attacks and significantly reduces regulatory risks. Stability is ensured through automatic arbitrage: if the LUSD price dips below $1, collateral holders (ETH) can redeem LUSD at face value ($1), quickly restoring its peg. This makes LUSD ideal for those concerned about censorship or regulatory freezing of assets.

However, the absence of incidents involving these stablecoins doesn’t guarantee they are immune to future risks. None of these coins have reached widespread adoption levels sufficient to confidently assert their reliability under extreme market stress or significant uncertainty.

Nevertheless, these stablecoins are available for exchange on rabbit.io, and you can test them yourself as alternatives to those tokens that have already demonstrated vulnerabilities and repeatedly experienced issues. This approach allows you to diversify your risks rather than relying on tokens that have proven problematic in the past.