Hyperliquid: Has the Exchange Truly Become Decentralized?

Back in May, I wrote that Hyperliquid was a striking example of CeDeFi — a system that uses decentralized finance technologies to build a centralized product.

By “product,” I meant its on-chain perpetuals exchange. To me, it looked as if Binance decided to store all your deposit and trading data not in a private database visible only to you and the exchange, but in a public ledger — one that anyone could inspect. At the same time, the exchange still had the technical ability to alter or delete any record, or simply refuse to process your transaction.

And that’s exactly how Hyperliquid worked a few months ago:

- All deposits and trades were recorded on-chain;

- The blockchain had only four validators — all connected to the project’s developers;

- A quorum of validators could rewrite any block or contract;

- And if validators refused to include your transaction (for example, a withdrawal), you had no way to enforce it.

To make matters worse, trading was only possible through the official interface at api.hyperliquid.xyz or via the mobile app. If either went down, you couldn’t trade at all — not even cancel your orders to free up collateral for withdrawal.

But things have changed since then:

- Anyone can now become a validator on the Hyperliquid blockchain — no developer approval required;

- The exchange has gained alternative access points through wallets like Phantom, MetaMask, and others.

Which brings up an important question: Has Hyperliquid finally become a truly decentralized exchange?

What Do We Expect From a Decentralized Exchange?

No single point of failure. A truly decentralized exchange can’t be switched off. Even if one node or frontend goes down, trading continues through the rest of the network.

Open access and freedom to build new interfaces. When there’s no central authority that can forbid or restrict anything, users aren’t tied to a single website or app. A DEX protocol running on a public network can be accessed in many ways — through alternative web clients, wallet integrations, or third-party apps. This removes dependence both on a specific domain (which could be blocked) and on the developers of the official frontend.

Open-source code for smart contracts and infrastructure. If the code is closed, nobody can be sure that the developers don’t have hidden levers allowing them to manipulate trading or other core processes. Transparency of code is what turns trust into verifiable security.

Personal control over trading funds. In a decentralized exchange, users themselves manage the assets they use for trading. There’s no central authority that can stop you from placing, modifying, or canceling an order — and, most importantly, no one can block or delay your withdrawal of the funds you’ve deposited as margin.

When I mention “margin,” I primarily mean DEXs designed for futures and perpetual swaps. That’s the segment Hyperliquid originally entered — and it remains the one most in demand among active traders.

Hyperliquid’s Steps Toward Decentralization

Since the publication of my previous article, Hyperliquid has made significant progress toward decentralization.

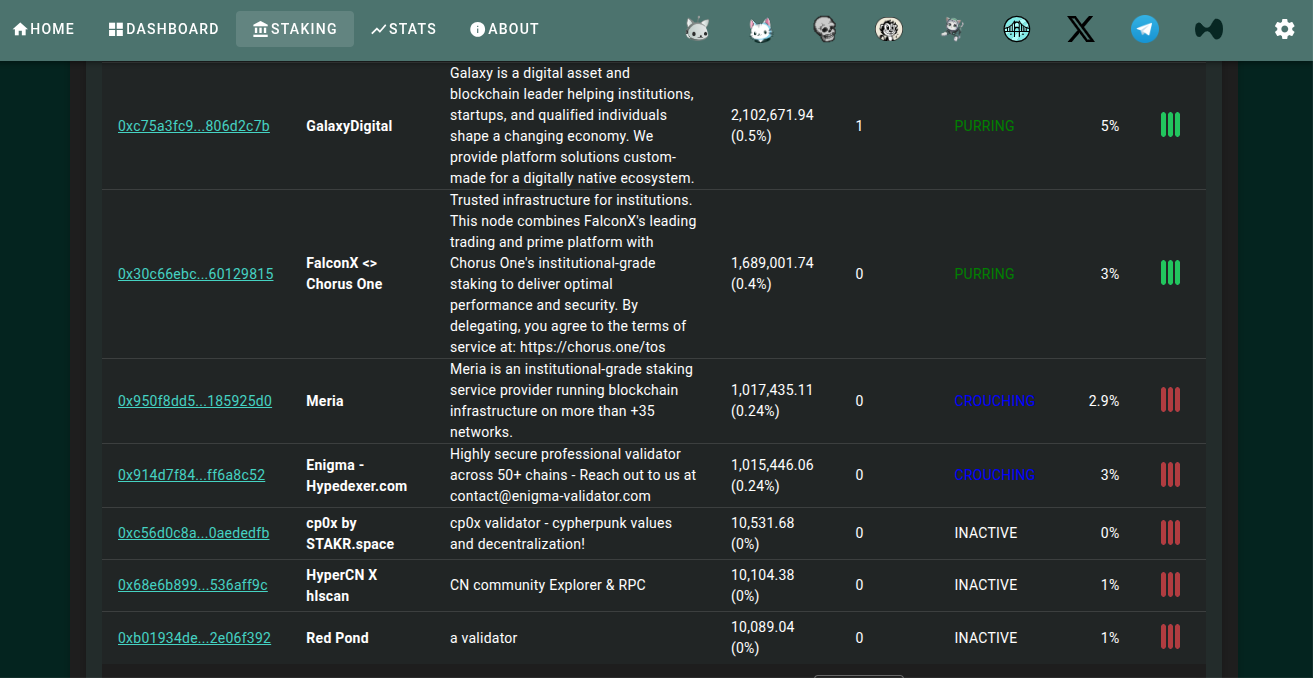

Open validator access. Previously, new validators could only join with the team’s approval. Now, anyone can become one. The instructions are publicly available, and the process requires no special permission — just technical setup and a large enough stake. The requirements, however, are steep: there are only 24 validator slots in total, and to earn one, a candidate must lock enough HYPE tokens to reach the top 24 by stake.

The full list of validators is available on Hypurrscan, where anyone can view the stake amounts of active validators and candidates — and get an idea of how much HYPE is needed to qualify for block validation.

At the time of writing, the entry threshold — defined by the stake of the 24th validator — stands at 1,689,001.74 HYPE, which equals over $66 million at current prices.

That’s far beyond the reach of most users, but for large players it offers a safety valve: if their funds ever get stuck on the exchange and the active validators refuse to include their withdrawal transaction, they could, at least in theory, stake enough tokens to enter the validator set and validate the withdrawal themselves.

Geographical distribution of validators. Once the protocol opened validator registration, the network quickly expanded. New participants include experienced staking pools and professional validators such as Imperator, B-Harvest, Alphaticks, ValiDAO, and others. They operate in different jurisdictions, which lowers the risk of simultaneous outages or coordinated disruptions.

The official staking guide emphasizes that token holders can delegate their stake to any validator — and move it freely from one validator to another. This gives the community the ability to redistribute voting power and react to potential downtime among key nodes. No single validator is indispensable.

Open-source progress. The project has gradually been publishing components of its source code on GitHub. It’s not full transparency yet, but it allows the community to review how consensus is implemented and contribute to its improvement. This openness also enables ecosystem growth: in September 2025, Hyperliquid held its first in-person hackathon — a sign that the team is actively engaging with developers and encouraging participation.

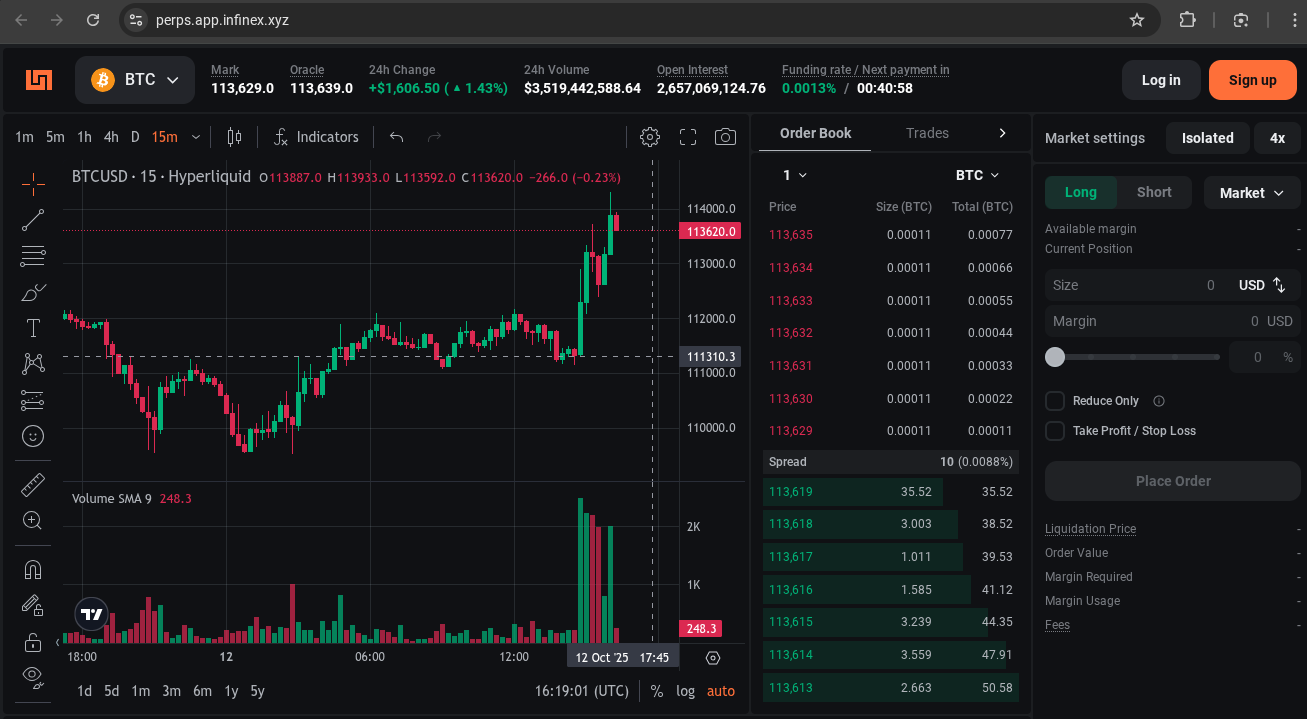

Multiple access points. Hyperliquid is no longer tied to its official frontend. The exchange can now be accessed directly through several popular wallets. Most notably, MetaMask has integrated perpetual trading on Hyperliquid directly into its interface. In addition, Infinex — a decentralized frontend launched by the 1inch team — now uses Hyperliquid as its backend for derivatives trading.

The appearance of these alternative entry points means that even if the Hyperliquid website goes offline, traders can still interact with the protocol through other applications. In effect, the frontend monopoly is gone: the network is accessible from multiple clients, making it far more resilient to censorship and technical failures.

All these developments show a clear and deliberate move by Hyperliquid to eliminate central points of control. The project has been actively responding to community criticism — expanding the validator set, reducing its own influence, opening its technology, and promoting integrations.

The Hyperliquid technical roadmap for 2025 explicitly states the goal of “Full Decentralization” — a multi-stage process expected to take 6–12 months. While this transformation is not yet complete, Hyperliquid today looks very different from the version I wrote about in my first article.

Evaluating Hyperliquid by Decentralization Criteria

So, has Hyperliquid’s nature changed enough for it to be called a decentralized exchange? Let’s go through the criteria one by one.

Control over the network. At the moment, Hyperliquid is governed by 24 validators, and they are not directly controlled by the developers. However, the nodes belonging to Hyper Foundation hold 60.5% of the total validator stake. In theory, that’s not enough to alter any block or smart contract — such interventions require 66.67%. But in practice, about 20% of the total stake doesn’t belong to independent validators; it consists of tokens delegated to them through the delegation program launched by Hyper Foundation. This means that the amount of tokens needed for single-party control over the network can be withdrawn from independent validators and redirected to the team’s own nodes at any time.

The single point of failure — a kind of “supernode” controlled by the developers — has not been eliminated. If the team decided to stop the network while other validators continued producing blocks, it would still have the tools to replace each of those blocks with an empty one.

Accessibility and censorship resistance. Hyperliquid has made major progress toward letting users operate without relying on a single website. The integrations with MetaMask and Infinex are clear proof of that. Now, all you need to trade is a wallet and access to the blockchain through RPC. If tomorrow the Hyperliquid domain were blocked or the team shut down its interface, trading would continue — anyone could simply switch to another interface. That fully matches the DeFi ethos: permissionless access to financial activity.

Open code. Here, Hyperliquid is still in progress. The code of its core smart contracts has not yet been fully opened, so we can’t be certain that there are no hidden mechanisms of centralized control. However, the direction is clear: the more confident the developers become in the reliability of their code and the safety of open-sourcing it, the more components will become available for public review.

Custody and withdrawals. In this area, nothing has changed. Hyperliquid remains a custodial platform, just as it was initially. To start trading perpetuals, users must deposit USDC on the Arbitrum network. These tokens go into a smart contract entirely controlled by Hyperliquid validators. Withdrawals can only be processed with their approval. Support for deposits in other cryptocurrencies has been added, but that situation is even more complicated: when depositing such assets, users send them to intermediaries, so withdrawals depend not only on Hyperliquid’s validators but also on those intermediaries fulfilling their obligations.

However, there is a partial solution. When you deposit USDC on Arbitrum into the Hyperliquid bridge contract, you receive wrapped USDC tokens on the Hyperliquid blockchain in return. These tokens represent a kind of promise from the bridge administrators to redeem them for the corresponding amount of USDC later.

Occasionally, Hyperliquid has failed to fulfill these obligations. Several users have reported losing access to the exchange interface at different times. Without that access, they couldn’t cancel limit orders, close positions, or release collateral for withdrawal back to Arbitrum. Now that there are several interfaces, if access is blocked, users can simply open Phantom or MetaMask, import their seed phrase, and cancel orders or close trades manually to free their funds.

USDC on the Hyperliquid network cannot be redeemed directly by Circle for real dollars — after all, these are wrapped tokens, and Circle does not recognize them. However, since Hyperliquid USDC is the main trading asset on one of the largest on-chain exchanges, the token has gained traction in the crypto community.

That means you can go to rabbit.io and exchange wrapped Hyperliquid USDC for any of over 10,000 available cryptocurrencies — including official USDC on any network supported by Circle.

Conclusion

At the moment, Hyperliquid has come significantly closer to the status of a decentralized exchange. It has eliminated the main flaw of the past — the network’s dependence on a narrow circle of trusted developer nodes. Thanks to 21 independent validators and open access to the network, Hyperliquid no longer has a visible point of failure that could simply be “switched off” with a button press. But there is still an “invisible” one — through tokens delegated by the developers to independent validators, which can be withdrawn at any moment.

Of course, Hyperliquid still has room for improvement. For example, some service components (such as API servers) remain centralized. But what matters most is the trend: the project consistently declares a path toward a fully open and resilient protocol, and its recent steps confirm the seriousness of that goal.

Thus, Hyperliquid today is no longer an example of CeDeFi — it is an example of a platform moving toward real decentralization. If the Hyperliquid team continues on its path toward giving up control, we can expect that soon the exchange will meet decentralization criteria 100%, becoming a fully on-chain protocol beyond the control of any single entity.