bullHYPE: The Return of Leveraged Tokens. Part I

This week, the Hyperliquid ecosystem saw a fairly high-profile launch. Hypezion Finance went live with a pair of new toys: the hzUSD stablecoin and the bullHYPE token.

bullHYPE is a leveraged token. HYPE enthusiasts are thrilled about it. And no wonder: free leverage and no margin calls sound like a dream - buy it and get rich. In Hyperliquid community chats, the dominant reaction sounds something like this: "A good way to long HYPE with leverage at the bottom without liquidation risk."

I have been in crypto for a long time, and the word "BULL" in a token's name makes me smirk almost automatically. Six years ago, the market went crazy for assets like this. For many people, it ended in tears. So what is this - are these tokens really making a comeback?

Not quite. Once I dug into how bullHYPE actually works, I realized this is not just a rebranding of an old idea. The structure here is fundamentally different. It has real advantages of its own, but it also has traps of its own - traps that hardly anyone talks about.

In the first part of this article, I want to revisit what was wrong with the old leveraged tokens and explain why the concept was unfair to holders from the very beginning. Then, in the second part, I will explain what bullHYPE really is.

A graveyard of old hopes

DX Exchange's turbo tokens

The idea of "buy a token and get leverage without the hassle of margin" is not new. Its first serious attempt already went badly back in 2019. In July of that year, the Estonian exchange DX Exchange launched "turbo tokens" with leverage ranging from 5x to 15x. The idea was simple: if the price of a chosen cryptocurrency moved by 1%, the token with leverage would move by 5%, 10%, or 15%. Long tokens rose when the cryptocurrency went up, and Short tokens rose when it went down. On July 17, 2019, when the crypto market dropped sharply, the exchange showed on its Facebook page how much profit an investment in Short tokens could have made in 24 hours.

It looked tempting, but on September 26, 2019, disaster struck. The exchange's internal currency, DXCASH, collapsed by a factor of 25.5. Under the rules, holders of the 15x leveraged tokens should have earned spectacular profits: the price of those tokens should have risen 382-fold. But the market maker, whose job was to support the price, simply refused to honor its obligations and did not place buy orders at those extreme prices. And if nobody is willing to buy at the "official" price, then that price is a fiction.

DX Exchange never recovered from the reputational damage and shut down on November 3, 2019. The first buyers of leveraged tokens learned two important lessons:

- Nobody can guarantee a token's price. It is determined only by supply and demand, not by the price movement of some other cryptocurrency.

- When you buy leveraged tokens, you are playing against the casino - the authorized dealer of those tokens - and if you win too much, the casino simply breaks the roulette wheel.

FTX's BULL and BEAR tokens

The real revolution came from FTX, which in August 2019 launched its own tokens: BULL (3x long Bitcoin), BEAR (3x short Bitcoin), ETHBULL and ETHBEAR (the same for Ether), and dozens of others. The mechanism was more transparent: the exchange set aside dedicated accounts with positions in perpetual futures. Each token was backed by a position in the corresponding account. When you bought $1 worth of tokens, the exchange used that dollar to open a $3 futures position with 3x leverage.

If the price of the underlying cryptocurrency moved by 11.15%, the exchange rebalanced: it closed the old futures position and opened a new one sized to keep the token tracking correctly. Once the old position was closed, the balance of the backing account changed by 33.45% (11.15% * 3). Because of that, the size of the new position also changed, while the leverage remained the same: 3x.

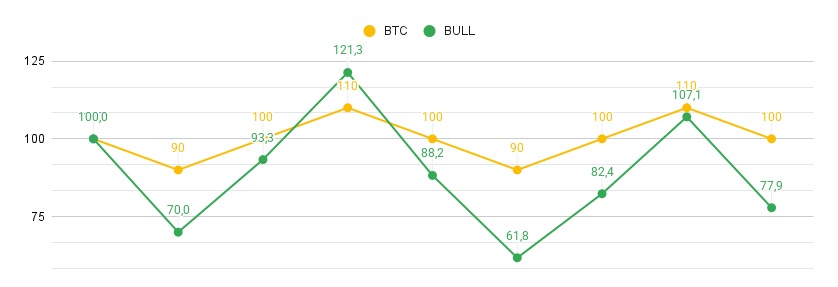

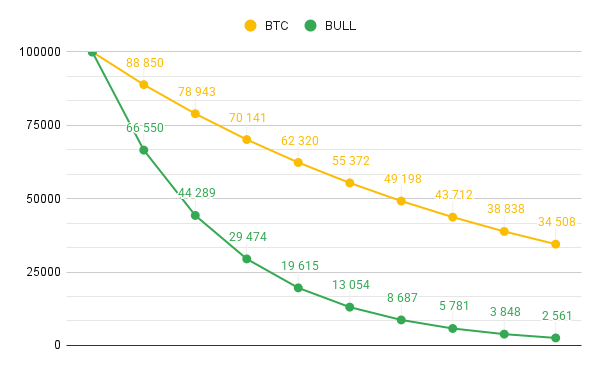

This approach made it possible to avoid the token price collapsing all the way to zero. Without rebalancing, a one-third drop in BTC would have meant a 100% drop in BULL. With rebalancing, the outcome was much less severe. Here is an example of how the price of BULL would change if BTC fell from $100,000 to $35,000, assuming BULL also started at $100,000.

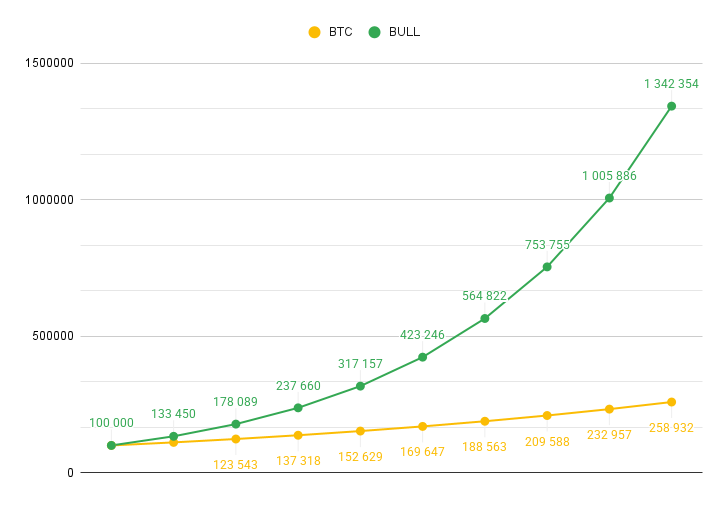

Interestingly, when BTC went up, rebalancing had the opposite effect: instead of dampening price changes, it amplified them, making BULL's upward movement sharper.

If the price did not move by 11.15% or more, rebalancing happened once per day. Every day at 2:00 UTC, FTX closed the old futures positions, realized the profit or loss, and used the updated balances to open new positions.

Rebalancing required paying trading fees. To cover those costs, FTX charged token holders 0.03% per day. That is 11% per year on top of whatever the market is doing. So the leverage was not free at all. It all looked far more professional than DX Exchange.

Binance joined the game as well by listing FTX's tokens. That was the peak of the hype: you could buy a "3x long Bitcoin" position in token form, withdraw it to your own wallet, and then sell it on another exchange like any ordinary cryptocurrency.

But on March 12, 2020, amid coronavirus panic, the crypto market crashed by tens of percent within minutes. ETHBULL on FTX behaved as designed: it lost about 75% while ETH fell 32%. But on Binance, the token dropped only 65%. The reason was that market makers were not placing fresh sell orders at current prices. Not because they did not want to, as in the DX Exchange incident, but because they could not. They had simply sold everything they had.

New tokens could be created only on FTX, and then had to be transferred to Binance over the Ethereum network, which was severely congested because of the panic. Binance management learned the same lesson that DX Exchange traders had learned six months earlier: nobody can guarantee that token prices will match what the algorithm says they should be. Two weeks later, Binance removed all FTX's leveraged tokens from its platform.

Where are all those tokens now?

FTX was not the last exchange to offer leveraged tokens. Similar products also existed on KuCoin, Bybit, and Gate. Even Binance made one more attempt - this time launching such tokens on its own platform, where new tokens could be issued quickly if needed so that the market maker could keep doing its job.

But on May 19, 2021, history repeated itself. That day, Bitcoin fell by about 30%, and the bearish BTCDOWN token should, in theory, have exploded higher. Instead, it rose only 10%. Shocked holders complained about decoupling: the instrument failed to do the one thing it had been designed to do, exactly when it was needed most.

Binance never gave traders a clear explanation. And the whole idea of leveraged tokens seemed to have been buried. If you go to CoinGecko's Leveraged Token category today, the picture is bleak. The capitalization of the entire sector is only about $1.8 million.

- FTX's tokens disappeared along with the collapsed exchange.

- In spring 2024, Binance delisted all of its UP and DOWN tokens under the pretext of "protecting users."

- Bybit shut down its similar product in June 2025.

- KuCoin completed the delisting of most of its tokens by the end of 2025.

- Among major players in the centralized leveraged-token market, Gate is effectively the only one left.

Some decentralized tokens survived - those whose price formation is governed by smart contracts rather than by a market maker who can walk away at any moment.

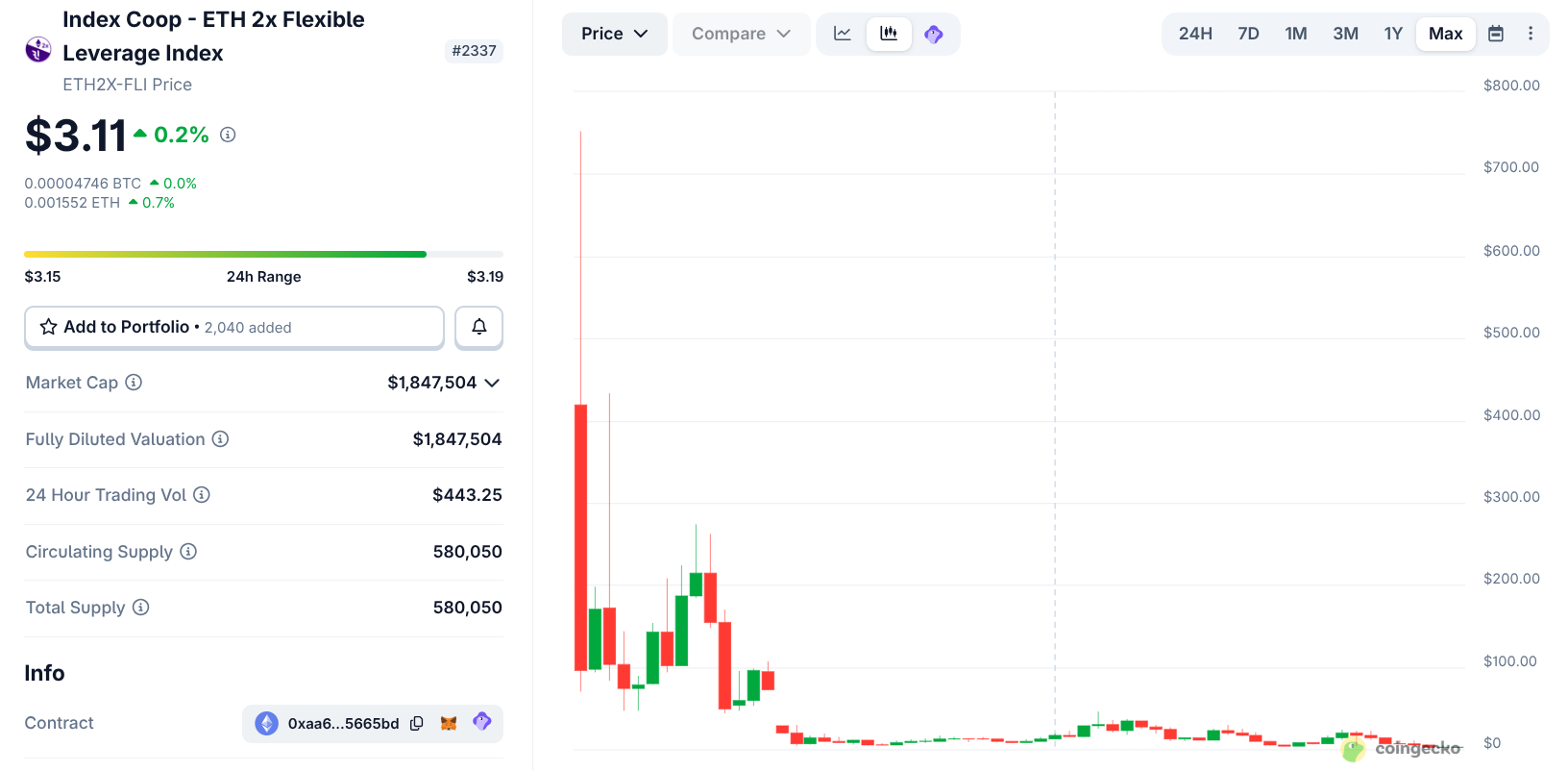

One surviving token from the first wave is ETH2x-FLI, with daily trading volume of $443. At its 2021 peak, it traded at $751. Today it is around $3. That is a 99.6% decline, even though Ether itself has gone up over that period.

The math of a serial killer

Why do even honest DeFi tokens like ETH2x-FLI get ground into dust? The answer lies in the mechanism of daily rebalancing.

To keep the token delivering exactly 3x or 2x exposure at all times, the smart contract or the exchange recalculates the position every day: buying more after price rises and selling after price falls. This works very well for the trader if the market moves steadily upward or downward without pullbacks or rebounds. But here is how it destroys capital in a sideways market:

- The trader buys a 3x token for $100.

- Bitcoin drops 10% in one day.

- The token falls 30% and is now worth $70.

- The next day, Bitcoin rises 11.1% and returns to its original price.

- The token gains 33.3%. But 33.3% of $70 is only $23.3. So the token rises only to $93.3.

- In the end, Bitcoin is back where it started, but the token has lost 6.7%.

If Bitcoin rose first and then fell, the effect would still be the same. Today BTC rises by 10%, and tomorrow it falls by 9.09% - so it ends up exactly back at the starting point. But BULL rises from $100 to $130 on the first day, then drops 27.27% on the second, leaving only $94.55 out of the original $100.

And that happens with every up-and-down cycle, every pullback, every flat patch. The longer you hold, the deeper the hole gets. This is called volatility drag. The mathematical fact is that this "volatility tax" grows in proportion to the square of the leverage. The higher the leverage, the faster the decay eats up capital. In the crypto market, where prices are constantly jumping around, this math reliably wipes out long-term holders.

This is not a scam. Anyone who understands that the geometric mean is always lower than the arithmetic mean when there is dispersion - will not buy leveraged tokens. On the contrary, they will issue them and sell them to users, then buy them back later at a lower price. Everyone who had that opportunity did exactly that: DX Exchange, FTX, and Binance. Gate is still doing it now, except that now hardly anyone wants these tokens anymore.

From what I have seen, interest in these tokens faded a long time ago. Until autumn 2025, Rabbit.io supported several tokens of this kind: users could exchange them for any cryptocurrency, as well as exchange any cryptocurrency for them. But even though we offered the best available exchange rates for those routes - just like for all the others - nobody was interested.

And at precisely this moment, when the crypto market had already forgotten about leveraged tokens, Hyperzion appears on the scene with its own reincarnation of the idea.

Well, I remember that this kind of product can be profitable for Hyperzion itself. But what about users? Can bullHYPE actually be profitable for ordinary holders too? We will talk about that in more detail in the second part of the article, which will be published in The Rabbit Hole exactly one week from now. Subscribe so you do not miss it.