Ethereum Is Applying for Government Service. Will It Get the Job?

On July 1, 2026, the Ethereum Foundation published a blog post titled Ethereum for Governments and Institutions: Why neutral infrastructure matters now, along with a report aimed at officials and institutional investors. After a decade of Ethereum being live, the team behind the project has decided to turn its attention toward governments. It now pitches Ethereum as "credibly neutral" public infrastructure for trade settlement, asset issuance, digital identity, land and other registries, attestations, supply-chain tracking, and similar use cases. The report's headline numbers are meant to inspire confidence in the platform: the network is secured by $76 billion in staked ETH, the cost of attacking consensus is estimated at $50.7 billion, the ecosystem is supported by more than 11,000 developers, and the network has not gone down once since launching in 2015. Just in case, the report also notes that this sets Ethereum apart from Solana, XRP Ledger, BNB Smart Chain, Canton, and Tron, each of which has suffered between one and seven outages - including one Solana outage in 2023 that lasted almost 19 hours.

It is an ambitious pitch, but it would be naive to expect it to succeed just because the numbers look good. Ethereum itself has a track record of promises that never quite panned out. And there is no shortage of blockchains that tried to claim the role of "the government's blockchain" before it - almost none of which managed to hold that role in any serious way. To gauge how well-founded the current pitch is, I want to look at two things: the road Ethereum took to arrive at this new positioning, and what became of everyone else who tried to occupy the same niche before it.

Part 1. A Decade of Reinvention

Ethereum was not originally aimed at becoming a government blockchain. The 2014 white paper described it as "a platform for smart contracts and decentralized applications" - an environment for writing and running algorithms for currencies, financial instruments, property registries, DAOs, and applications that were hard to even imagine at the time. But there was no talk of any specific practical purpose for the platform. Anyone could find their own use for it. That is where the image of the "world computer" came from: a programmable network for anything and everything.

Even before the "world computer" label stuck, part of the community cast the young project in the role of "Bitcoin 2.0" - an improved version of Bitcoin. That label did not last long, though: the Turing-complete virtual machine, the EVM, and the smart contracts that Vitalik Buterin built into the project took Ethereum so far beyond simply storing and transferring funds that the comparison to Bitcoin stopped explaining anything. "World computer" was a more coherent, more ambitious metaphor: a decentralized machine for running any code, with no censorship and no intermediaries.

The DAO saga dealt this vision of Ethereum's purpose a serious blow. In June 2016, a hacker drained 3.64 million ETH - 15% of all ether in existence at the time - from a vulnerable contract, and the Ethereum Foundation's answer was to reverse that transaction through a hard fork. It turned out that at a moment of crisis, Ethereum was governed not by code, but by the developers. It is hard to call such a system a "world computer". Unless, of course, it is a computer with an owner - and that owner is not you. So the narrative was gradually dropped.

In 2017, the network unexpectedly found a new purpose. It became the platform for ICOs: ERC-20 tokens let anyone raise funds for a crypto project in a matter of hours. From a computer for any task, Ethereum turned into a token-minting machine. Many of those tokens turned out to be scams, and pitching the blockchain as being for token issuance became pointless, even dangerous. On top of that, the ICO boom ended - but Ethereum was still standing. It outgrew the narrative that its main purpose was minting tokens.

After hopes for ICOs collapsed, the network found a sturdier calling in DeFi: between 2020 and 2021, Uniswap, Aave, and MakerDAO drove total value locked to a peak of roughly $177 billion. And the sale of Mike Winkelmann's collage Everydays: The First 5000 Days at Christie's for $69 million turned Ethereum into the home of a new phenomenon as well: NFTs linked to digital art.

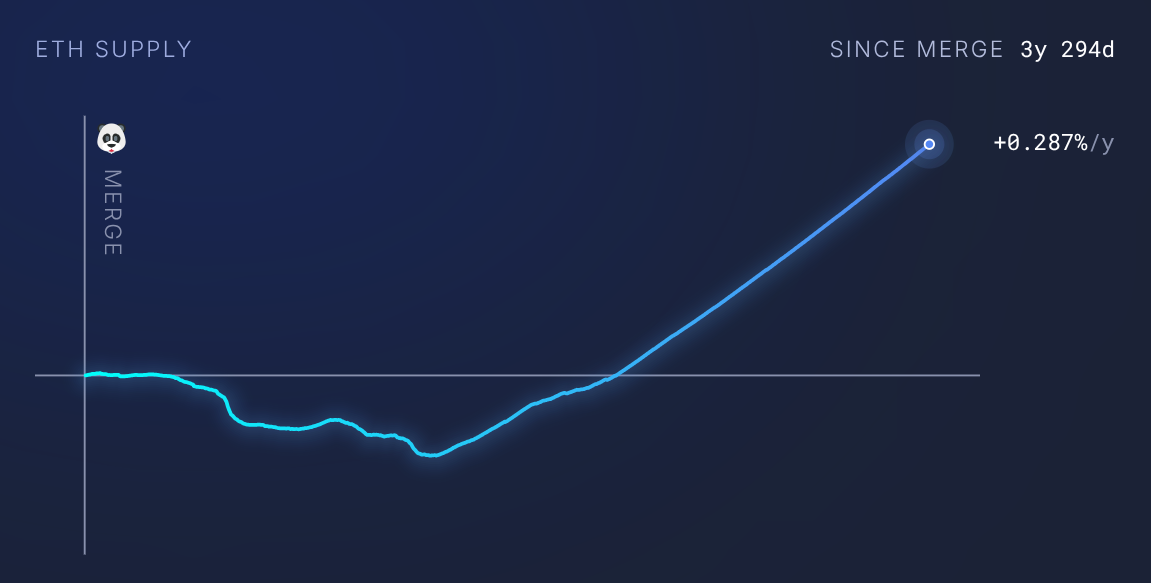

The DeFi and NFT frenzy forced a radical rethink of the network's architecture, since the sheer volume of on-chain activity outstripped its throughput. As a result, at peak load a simple ETH transaction could cost tens of dollars. The answer was the move to Proof-of-Stake, known as the Merge, and a modular architecture in which layer 1 handles security and finality while execution moves to layer-2 rollups. Around the same time, as EIP-1559 rolled out - burning part of the transaction fee and potentially making ETH a deflationary asset - the "Bitcoin 2.0" idea also made a comeback: ether as money fit for both saving and everyday spending. That did not last long either. After the 2024 Dencun upgrade, burning on layer 1 dropped sharply and ETH supply started growing again.

Recently, a new use case for the network has taken hold in earnest: tokenizing real-world assets, money in particular. Laws governing the status of stablecoins and other RWA tokens are being adopted in a growing number of countries, the US now among them. And this new use case is gaining traction for Ethereum at just the right moment: marketplaces are shutting down one after another, and the DeFi market no longer looks quite so triumphant.

So Ethereum never fully fit any of the frameworks that tried to define what it was actually for. It outgrew some of them, such as being an ICO platform, and never grew into others, such as an autonomous world computer.

Part 2. A Graveyard of Government Blockchains

The idea of turning a blockchain into a state's official information infrastructure is not new, and the experience of those who tried before offers a lesson.

The Algorand team came closest to pulling it off: in 2020, the blockchain was chosen as the technical foundation for the Marshall Islands' SOV, pitched as the world's first sovereign digital currency. Even before that choice was made, in September 2018, the IMF issued a 58-page report directly recommending that the whole SOV idea be seriously reconsidered. The government did not back down, but the currency never really launched: years later, SOV remained little more than paper. The technology was ready; what was missing was the political will and the international backing for the government of a small country that had taken on a project too big to pull off alone.

Government-level monetary settlement on blockchains did eventually become a reality elsewhere. The most striking example is El Salvador, where Bitcoin was legal tender for three and a half years. But when Ethereum reaches for a government role, it is not primarily angling to be a payment rail for financial settlement. In that context, other stories are more instructive.

Take Cardano's use in Ethiopia's education system, for instance. In October 2021, five million schoolchildren and 750,000 teachers were issued digital IDs on that blockchain for publicly verifiable tracking of academic achievement. But by June 2023, only 38,000 students were actually using the system. Civil war, a change of government, and ordinary bureaucracy got in the way. Government officials were not willing to accept educational certificates issued by an organization outside state control. In the end, in 2024, IOG, Cardano's developer, shut the project down.

Another important example is Hedera, which was deliberately designed as a blockchain for institutions and governments. The network has some notable projects, but they remain one-offs. That is because Hedera's development is governed by a council of several dozen corporations - Google, IBM, and Boeing among them - each running its own node and voting on protocol changes. For governments, that means critical infrastructure ultimately depends on decisions made by the boards of private companies, some of them foreign. Interestingly, the Ethereum Foundation clearly understands this fundamental tension between blockchain technology and governments' desire to hold onto maximum control, and its pitch to governments promises to help them escape exactly that kind of corporate counterparty risk.

There have been other corporate initiatives that tried to break into government-level use, too.

- In 2022, Maersk and IBM shut down TradeLens, infrastructure meant to connect international trade, ports, customs, carriers, and the government agencies involved in clearing cargo. Here the obstacle was not government resistance but competitors' unwillingness to share data on a system controlled by one of the players in the market.

- Australia's national clearing system was supposed to move onto blockchain, but the project was scrapped in 2022 by its developer, the ASX exchange, because the work dragged on for too long and cost too much. This is a rare case of a blockchain's bid for government-level use failing because of technical unreadiness, rather than political or economic resistance.

- And perhaps the most telling example is the Central Bank of Brazil's 2025 decision to drop blockchain from its CBDC project, Drex. The official reason was that it proved impossible, at an acceptable cost and speed, to reconcile transaction privacy with the regulator's need for full visibility.

Why do I find this last example so telling? Because it aired publicly an idea rarely said out loud: that even central bank digital currencies - a form of money whose very existence was prompted by crypto technology - might not need blockchain at all. Until then, governments had still tried to position CBDCs as something just as trustworthy and immutable as a blockchain. And even when governments did not actually use blockchain in their digital currency infrastructure, as in China and Russia, they tended not to advertise that too loudly.

The takeaway from all these stories is that blockchain - even a private one, not necessarily a public one - simply is not what governments need for recording what happens within their borders. Blockchains are hard to control, hard to hide anything on, and governments are not ready for that kind of transparency and accountability.

Conclusion. Has the Ethereum Team Learned These Lessons?

Comparing these stories with the report Ethereum.org published on July 1, it is clear the Ethereum Foundation is answering precisely the objections that doomed its predecessors' attempts to claim a place in government.

- Against a corporate consortium like Hedera, it offers the argument that there is no operator, and that validators are spread across continents and jurisdictions with no single dominant country, with the protocol-level threshold for solo validation starting at an ordinary computer and 32 ETH. I would add that this is also a strong argument against Bitcoin, which, although it did carve out a government niche in El Salvador, cannot claim as low a technical barrier to entry. As a result, the function of adding new blocks to the Bitcoin blockchain is concentrated in the hands of a few large pools.

- Against an opaque offshore contractor like Cardano, Ethereum has more than 11,000 developers and at least five independent client implementations, so no single team behind any of them can unilaterally shut the network down.

- Against the risks that tripped up the Marshall Islands' SOV, there are already working systems: digital IDs in Bhutan, used by roughly 800,000 of the country's residents, and a similar project in Buenos Aires with 3.6 million users.

The Ethereum Foundation's report speaks directly to the three reasons Algorand, Cardano, and Hedera all failed to fully establish themselves at the government level — and positions Ethereum as the opposite on each count: years of uninterrupted uptime, no single controlling party to depend on, and an ecosystem mature enough to support a project for decades. And Ethereum's own history of lurching between "Bitcoin 2.0", "world computer", ICOs, DeFi, and institutional money actually works in its favor here: the network has accumulated a wide range of experience along the way. What is more, the fact that for years Ethereum was the only major public blockchain to have actually reversed a transaction in practice may also be working in its favor.

On objective criteria - uptime, validator decentralization, the declared absence of a controlling party, ecosystem maturity - Ethereum today reasonably looks stronger than Algorand, Cardano, or Hedera did at a comparable point in their own histories, and the Ethereum Foundation has built its case around exactly the reasons those projects failed. But the real question is not whether Ethereum is ready. It is whether governments are ready to entrust a public ledger with what currently lives in closed databases.

Ordinary users genuinely do choose between blockchains: some prefer Bitcoin, some Ethereum, some Cardano, some Algorand, and some even Hedera. I am not joking: on rabbit.io, swapping HBAR for stablecoins or other cryptocurrencies is far from rare. But for governments, there is probably little real difference between the solutions available in Ethereum's ecosystem, Bitcoin's, or any other blockchain's. What actually matters to them is how much authority the state itself retains over the registry. And it's hard to see what Ethereum has to offer governments on that front today that would set it apart.