DCA Alternatives. Part II

In Part I of this article, I covered several simple alternatives to DCA - the popular strategy for accumulating Bitcoin. I discussed four approaches:

- lump-sum investing,

- value averaging,

- calendar rebalancing,

- and threshold (tolerance-band) rebalancing.

Before moving on to four more strategies, I want to add a small bonus to Part I - a look at how these strategies perform using real numbers.

What if, when rabbit.io launched in early February 2024, you had exchanged 100 USDT for Bitcoin there - and then kept doing the same at the start of every month? What would your result be today? And how would the other strategies from Part I compare?

Here’s the answer:

So if you had been exchanging 100 USDT into Bitcoin every month, by now you would have invested 2,700 USDT and be up just $19. Why so little? Because you were buying Bitcoin both at $42,580 in February 2024 and at $115,800 in August 2025. Meanwhile, every other strategy from Part I would have delivered a much more noticeable financial result on the same capital.

One important caveat: With value averaging, it’s impossible to know in advance how much capital will be required to follow the strategy strictly. So I used a scenario where the initial contribution matched DCA ($100). The total required capital turned out to be slightly higher than 2,700 USDT.

Surprising, right? Many people assume DCA is the most profitable way to invest in Bitcoin, but real data shows it underperforms every strategy discussed in Part I. So if you haven’t read it yet, you might want to go back to it and see for yourself that these strategies are no more complex than DCA. Now let’s continue with more alternatives.

5. Constant Proportion Portfolio Insurance (managing)

The idea in one sentence. Set a floor (a minimum you won’t fall below), and take leveraged risk above that floor.

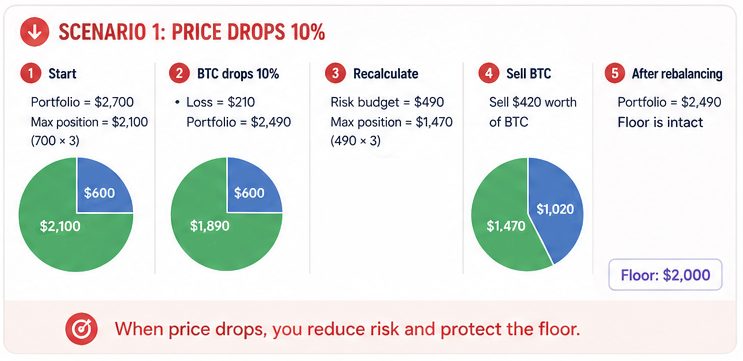

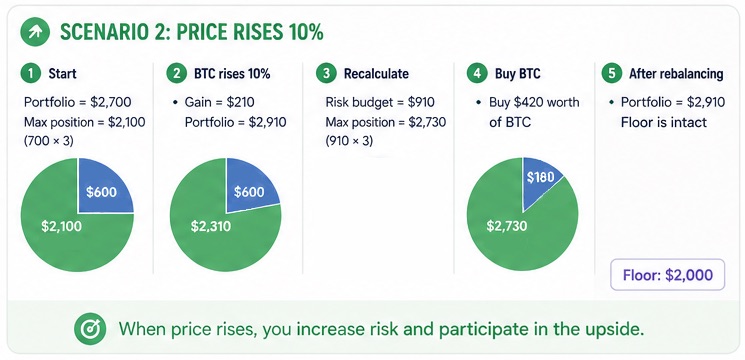

How it works. You have $2,700 and set a strict rule: your portfolio value must never drop below $2,000. That leaves $700 as your risk budget, and you choose leverage for that portion - say, 3x.

At the start, your allowable position size is $2,100 (700 × 3). You buy Bitcoin for that amount and keep $600 in stablecoins.

Now suppose Bitcoin drops by 10%, and your position loses $210 (10% of $2,100). You rebalance:

- your portfolio is now worth $2,490;

- the floor stays at $2,000;

- your risk budget is now $490;

- with 3x leverage, your maximum BTC position is $1,470 (490 × 3).

So you sell some Bitcoin to adjust your portfolio to $1,470 in BTC and $1,020 in stablecoins. Since you already had $600 in stablecoins, you need to sell $420 worth of BTC.

If instead Bitcoin rises by 10%, your capital grows by $210, and you rebalance as well:

- your portfolio is now worth $2,910;

- your risk budget becomes $910;

- with 3x leverage, your allowed position increases to $2,730;

- you buy more BTC, leaving just $180 in stablecoins (2,910 − 2,730).

In this strategy, you constantly tighten your exposure near the floor and expand it as you move away from it.

Notice how this approach lets you use leverage even in a simple crypto swapping service? You probably thought leverage was only for futures platforms. Not quite. Major crypto exchanges tend to give people the wrong idea about what leverage really is. I’ll cover this in more detail in a future article - subscribe to The Rabbit Hole so you don’t miss it.

Pros of CPPI:

- Participation in market upside.

- Protection of a minimum capital level.

- High capital efficiency during uptrends.

Cons and pitfalls:

- If the market crashes sharply overnight, the floor can be breached before you react. This requires a bot to monitor prices and readiness to act at any time.

- In long sideways markets, the strategy has a negative expected return (it tends to lose money over time).

If we apply CPPI to the period from February 2024 to today, the result would look like this:

- USDT invested: 2,700

- BTC now: 0.06177967

- USDT now: 0

- Portfolio value: 4,822.21

This outperforms DCA, VA, and both rebalancing strategies from Part I, because after Bitcoin rose twice by 10% in February 2024, the strategy effectively shifted the portfolio to 100% BTC. A partial sell would only have been triggered if the price had dropped to $48,500, which never happened. The result ends up very close to lump-sum investing, with a small difference: part of the capital wasn’t deployed at the initial price of $42,580, but only later, after BTC had already risen to $46,838 and $51,521.80.

6. Seasonal timing (managing)

The idea in one sentence. Buy or sell based on recurring calendar patterns.

How it works. There’s a well-known Wall Street saying: “Sell in May and go away.” It reflects a real pattern - historically, stock markets have performed better from November to April than from May to October.

Crypto has its own cycles and beliefs. Some are grounded in reality - like Bitcoin’s halving every four years. One year after a halving, Bitcoin has always been more expensive than at the moment of the halving. Others are more folkloric: the “Santa rally,” “Uptober,” or the infamous altseason - a drop in Bitcoin dominance at the final stage of a bull run, often seen as a signal of an upcoming reversal.

I’m personally skeptical of this approach. Patterns break. Black swans - pandemics, exchange collapses, geopolitical crises - can easily wipe out any seasonality. Past patterns don’t guarantee future results.

But there is one undeniably valuable aspect: understanding crowd psychology. If enough market participants believe in a “halving rally” and start buying, prices will rise simply because of that demand. Even if you don’t believe in these patterns, it’s useful to know what others believe.

Here are two of the most unusual patterns observed in the market:

- The “November 28 effect.” Major multi-year tops and bottoms in Bitcoin often occur within roughly three weeks of November 28. I listed specific dates on X - you can check them here. It sounds almost absurd, but think about it: if last year’s peak didn’t fall in that window, maybe it wasn’t the final peak - and 2026 could still bring higher prices.

- Lunar cycles. On TradingView, you can find indicators based on moon phases. Overlay them on Bitcoin’s price chart, and they generate buy/sell signals. Historically, new moons have often coincided with good buying opportunities, while full moons have aligned with good selling points.

I won’t list pros and cons here. Superstition and “magic” don’t fit neatly into rational analysis. But if, between February 2024 and April 2026, you had bought Bitcoin on new moons and sold on full moons - using your full capital each time - the result would have been:

- USDT invested: 2,700

- BTC now: 0.05188932

- USDT now: 0

- Portfolio value: 4,048.59

So even this seemingly ridiculous strategy ends up outperforming all strategies from Part I - except lump-sum investing.

7. Event-driven investing (building)

The idea in one sentence. Buy in response to specific events that trigger predictable price movements.

How it works. Let’s look at two examples:

- In August 2020, MicroStrategy became the first public company to allocate a significant portion of its capital to Bitcoin. On August 11, 2020, it bought 21,454 BTC for $250 million at an average price of around $11,650. This triggered a wave of corporate adoption and a subsequent price rally.

- In January 2024, spot Bitcoin ETFs were launched in the United States. That pushed institutional demand even further, along with the price.

Pros:

- With the right approach, returns can significantly exceed passive strategies.

- By tracking multiple assets, not just Bitcoin, you can build a diversified, fundamentally driven portfolio.

Cons:

- This strategy requires time, experience, and the ability to separate signal from noise. Beginners can easily mistake marketing hype for real catalysts. There’s also a high risk of manipulation and scams.

- Events of this magnitude are rare. Entry opportunities may appear only once every few years.

Since rabbit.io launched in February 2024, I can’t recall events of comparable significance that would justify going all-in on Bitcoin. At a stretch, one could point to the election of Donald Trump as U.S. president. It may have signaled a more favorable political climate for Bitcoin, potentially boosting demand.

If you had converted 2,700 USDT into Bitcoin on rabbit.io on that day, you would have received 0.03979366 BTC - worth 3,102.37 USDT today.

8. A hybrid approach (meta-strategy)

Experienced investors rarely stick to a single strategy. They combine them.

Here’s an example of a hybrid setup:

- Foundation: DCA for stability.

- Add elements of VA: if the market drops 15% from your average price, double your contribution; if it drops 30%, triple it. If the market is euphoric and up 20%+, cut your contribution in half.

- Add periodic or threshold-based rebalancing.

- Include CPPI elements: maintain a minimum amount in stablecoins that you don’t touch.

- Occasionally act on major events - if they truly matter.

- And always keep an eye on psychology. If everyone is buying, prices can rise simply because of that collective behavior.

This setup isn’t much more complex than DCA, but it’s far more flexible.

Conclusion

All the strategies discussed across Parts I and II outperform DCA over the same time period. That means DCA is a good first step - but it’s not where you should stop.