Why is the FDIC resisting public blockchains?

Coinbase lawyer Paul Grewal revealed documents showing the Federal Deposit Insurance Corporation (FDIC) obstructed U.S. banks from adopting public blockchains. The FDIC, a key banking regulator, monitors compliance with financial regulations.

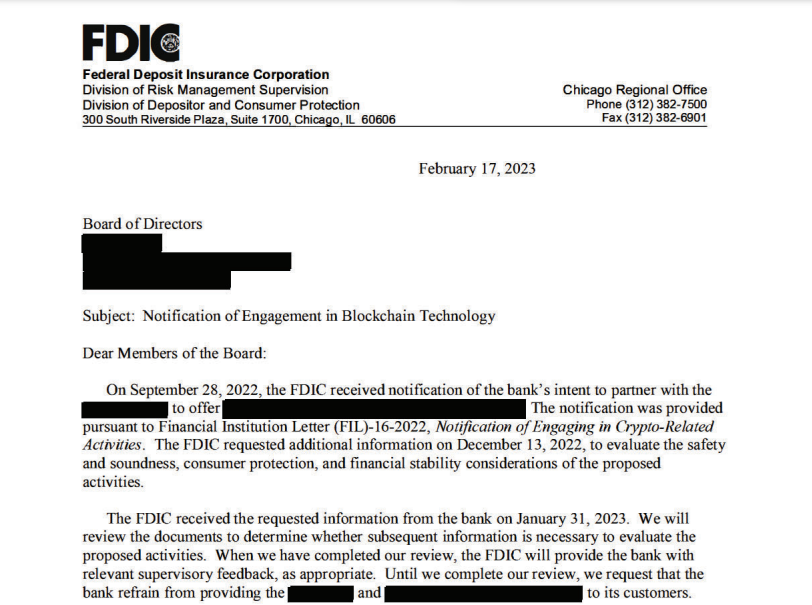

One document describes a New York bank’s attempt to launch a “Bank Digital Deposit” program on a public blockchain. The FDIC demanded additional inspections and criticized decentralized networks, where all transactions are transparent.

The FDIC’s preference for private blockchains, where data access is restricted, raises questions. Public blockchains may challenge banking secrecy, but it was the regulator - not clients - that raised objections, likely aiming to preserve its control or maintain opacity in operations.

Public blockchains limit regulators' control, as their immutable records cannot be altered or deleted. Yet, this transparency strengthens oversight: banks cannot deny deposits or fabricate false ones. It also holds regulators accountable, preventing compensation denial for verified deposits or payouts for non-existent ones.

This reflects a broader trend: central bank digital currencies (CBDCs) operate on private, opaque blockchains, restricting user control. In contrast, classic cryptocurrencies provide financial independence. And rabbit.io enables seamless exchanges between them.

The FDIC’s resistance undermines trust in regulators, as public blockchains offer society - not centralized authorities - real control over financial systems.