Hard Lessons for Bitcoin Treasury Investors

Today, many crypto and financial headlines are focused on companies that used investor money to buy Bitcoin in the hope of growing their capital.

Arkham pointed out that one of the worst-performing examples is Nakamoto. The company invested $679 million in Bitcoin at an average price of $118,000 and has held the position ever since. Its unrealized loss has reached roughly $224 million, or about 35% of the original investment. Meanwhile, its stock has lost 99.4% of its value, forcing the company to carry out a 1-for-40 reverse stock split to maintain its Nasdaq listing.

Many commentators are also discussing Strategy's recent Bitcoin transfers to Coinbase Prime. The most likely explanation is that the coins are being prepared for sale. After all, Michael Saylor, who only a couple of months ago was telling people, "Never sell your Bitcoin - sell a tooth or a kidney before you sell your Bitcoin," has noticeably softened his stance. These days, he talks about buying more than you sell rather than never selling at all.

The most interesting case, however, may be Sequans Communications. According to reports, the company sold 80% of the Bitcoin it had previously accumulated, paid off all of its creditors, and still retained 658 BTC on its balance sheet, now completely free of any encumbrances.

From the company's perspective, the strategy worked. The same cannot be said for investors who bought its stock. Anyone who purchased shares during the peak of the hype last summer is now sitting on losses of around 90%.

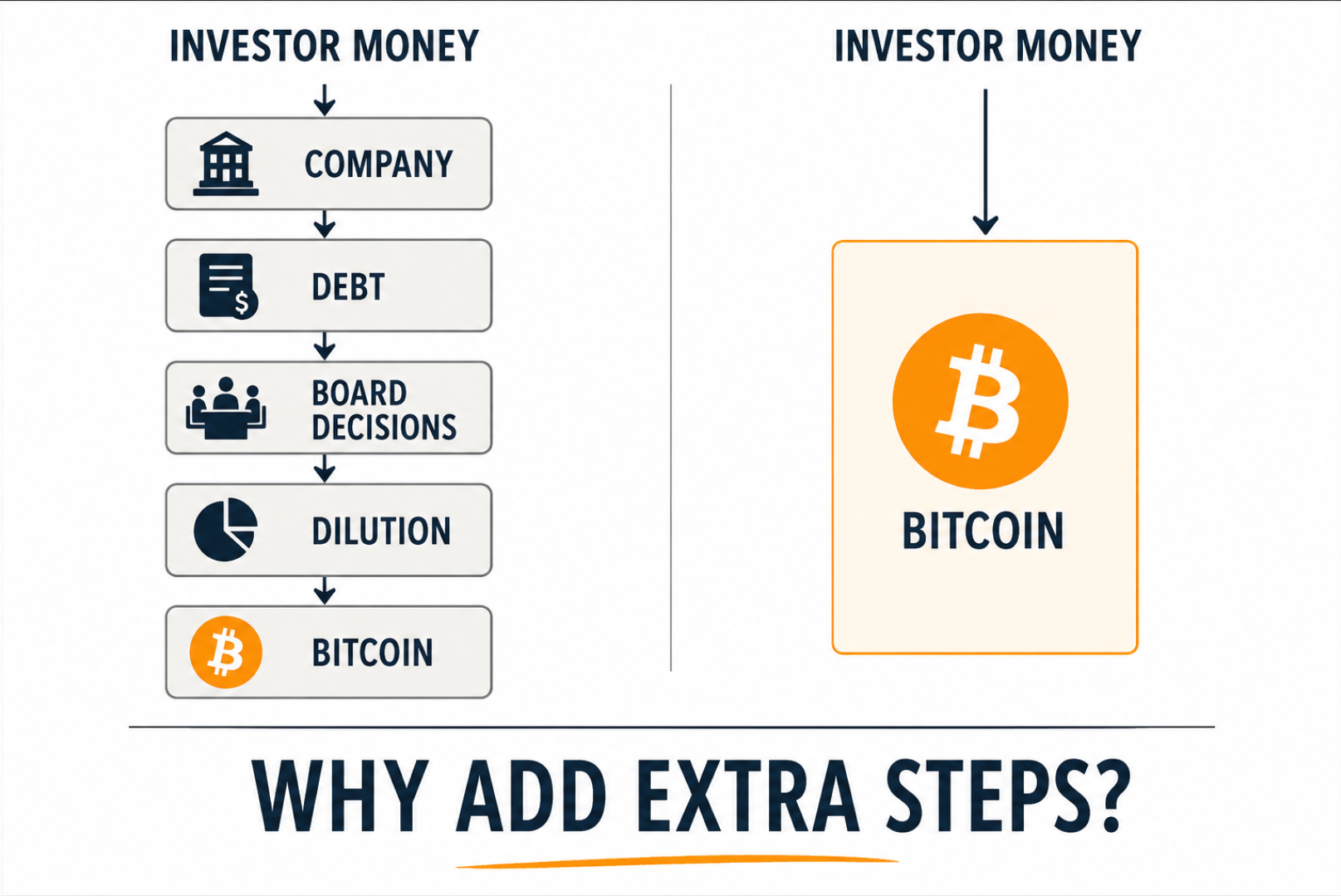

The market could hardly make the lesson any clearer: Bitcoin has proven far more resilient than the stocks of the companies that buy it. With Bitcoin, you are not dependent on management decisions, financing conditions, debt obligations, or the judgment of a board of directors. You are simply storing your savings in the most secure electronic database ever created. And the more people come to appreciate how reliable that form of storage is, the more valuable your asset becomes.