Why Crypto Services Don't Always See Smart Contract Transfers

Picture this. You have USDC sitting in Polymarket, and you want XMR for quiet, private storage. You go to rabbit.io, set up an order to swap USDC on Polygon for XMR, get the deposit address, send the tokens - and nothing happens.

The wallet you use on Polymarket signed the transaction. Polygonscan shows a green checkmark, the right address, and the correct amount. But the swap service does not see the deposit.

At first glance, this seems bizarre. The blockchain is shared by everyone. If the explorer shows an incoming transfer, why can't the service just press a button and credit the tokens?

But this is something you can run into at any crypto exchange or swap service. The reason is that exchanges and swap services do not read a block explorer the way you do. They use automated deposit accounting systems. And those systems need to understand not just that something moved somewhere on-chain, but that the movement represents a genuine, final, supported, and safe deposit.

That is exactly where the problem I want to talk about today begins.

Two Addresses That Look the Same

In EVM networks, there are two types of addresses.

- A user address. Officially, it is called an EOA, or Externally Owned Account - an address whose transactions are signed somewhere outside the virtual machine. Controlling one requires a private key.

- A smart contract address. Transfers from this address are produced by code executed on-chain. In other words, the address is governed by the algorithm written into the smart contract.

Both types can receive, hold, and send coins and tokens. To an ordinary user, they look almost identical: just a long string starting with 0x. But for any system that has to account for what happens inside transactions, the difference is significant.

Let me illustrate this with Ethereum.

If you send ETH from a regular wallet, it is a straightforward transfer: address A sent funds to address B. That operation is easy to find in the main Transactions tab.

But if ETH arrives from a smart contract, it may appear as an Internal Transaction. The recipient's balance really does increase, but the transfer happened as part of the contract's execution logic, according to the rules written into that contract.

Automatically crediting funds that arrive through such transactions is not always the right call. It is hard to argue against first checking what kind of contract the funds came from and what exactly happened inside the transaction.

But USDC Always Transfers Through a Contract!

Yes - and this is an important point.

Every ERC-20 token - USDT, USDC, WBTC, LINK, and so on - moves between addresses under the rules of the smart contract that defines it. When you send USDC, you call that token's contract. The contract updates its internal balance table and writes a Transfer event to the blockchain.

For tokens, this is normal mechanics. Deposit systems are built to process these transfers. So what is the fundamental difference between this kind of token transfer, which usually goes through without a problem, and another one that cannot be processed automatically?

The answer lies in who is listed as the sender in the token transfer event.

If USDC is debited from your regular EOA address and sent to the address of an exchange or swap service, everything is likely to go smoothly. Problems can arise when the tokens are debited from the address of a bridge, vault, router, smart wallet, multisig, or trading platform contract.

Why do I say problems can arise? Because the rules for handling smart contract deposits vary across services.

Coinbase, for instance, says that it supports ETH and ERC-20 deposits via smart contracts, but does not support equivalent deposits of SOL and SPL tokens on Solana. Bybit notes in its FAQ that smart contract deposits are unsupported for all coins except ETH. Crypto.com warns that most native EVM-chain tokens deposits from smart contracts are not credited automatically.

In other words, the industry still has no single rule for which contract-based transfers should count as normal deposits, which require manual processing, and which should not be accepted at all.

What makes this worse is that users may not even realize their tokens are being sent from something other than an EOA.

Where Does an Ordinary User Even Get a Smart Contract?

If I have not entered into any contracts with anyone, how can smart contracts have anything to do with my transactions?

Unfortunately, a smart contract really can appear in the chain without any direct action on your part. Here are three common scenarios where one shows up without warning.

The first scenario is withdrawing funds from a prediction market, DEX aggregator, lending protocol, or another dApp. These apps often hold assets not at your regular address, but inside a contract - even if your Web3 wallet does not make this obvious and you think the assets have stayed with you all along.

To be precise, they may be shown in your balance, but they are not fully under your direct control. Moving those tokens is possible only under the terms of the smart contract.

So you click Withdraw, the app sends funds to the right address - but the sender on-chain turns out not to be your EOA. It is the platform's contract.

The second scenario involves a bridge.

Bridges often come into play when withdrawing from exchanges or payment services that run their own internal blockchains, such as Hyperliquid, dYdX, Paradex, Payy Network, and others. In the database of that internal blockchain, the tokens may have been at your address, so you assume you are sending them from that address - not from a smart contract.

But when you move them to another blockchain, such as Arbitrum, Polygon, or Ethereum, the recipient may receive the tokens from an entirely different address. Your address on the destination network never held those tokens. They were held by the bridge contract or bridge-related infrastructure, while the internal chain represented your balance on the other side.

None of this means every such transfer will necessarily get lost. But it does mean it may not look like a simple transfer to the automated system of the receiving exchange or swap service.

The third scenario involves account abstraction wallets.

They are genuinely useful: they let you batch payments, pay gas in stablecoins, have a third party cover your gas fees, set up custom wallet recovery conditions, and use other convenient features. But that convenience is often achieved by turning your wallet into a smart contract.

Worth noting: the developers of one of the most popular wallets of this type - OKX Wallet - explicitly point out that such wallets are smart contracts and cannot be imported into another app via a seed phrase or private key.

To the user, it looks like their personal wallet. To the receiving service, the sender may be a smart contract.

Why Exchanges and Swap Services Are Wary of These Transfers

The simplest reason is technical. An automated deposit scanner may not track non-standard blockchain events.

This limitation could be fixed. But it did not arise by accident. Behind it is a deeper security concern.

You cannot trust every Transfer event just because it looks good in an explorer. Crypto history already includes fake deposit attacks, where an attacker creates the appearance of a deposit and the recipient mistakenly treats it as real.

The DEPOSafe research, published six years ago, found more than 7,000 contracts potentially vulnerable to such attacks. Those contracts have not gone anywhere. They are still deployed on Ethereum. And over the past six years, new vulnerable contracts have almost certainly been added, including in other networks.

The essence of these attacks is trusting the wrong signal.

The recipient sees an event that looks like tokens arriving and assumes the funds are now theirs. But contract logic can make the real outcome very different: the funds may be returned, burned, redirected elsewhere, or never actually end up under the recipient's control in the way the deposit system expected.

So the caution shown by exchanges and swap services is not bureaucracy, and it is not laziness about dealing with awkward transactions. Smart contracts are complex, and telling a reliable deposit from a fake deposit attack is not always straightforward.

How to Tell Whether You Are Sending from a Smart Contract

The interface of the app you are sending from sometimes gives you no clue at all about which type of address the funds will actually leave from. You can often assess this only after the fact, by checking what happened in the explorer.

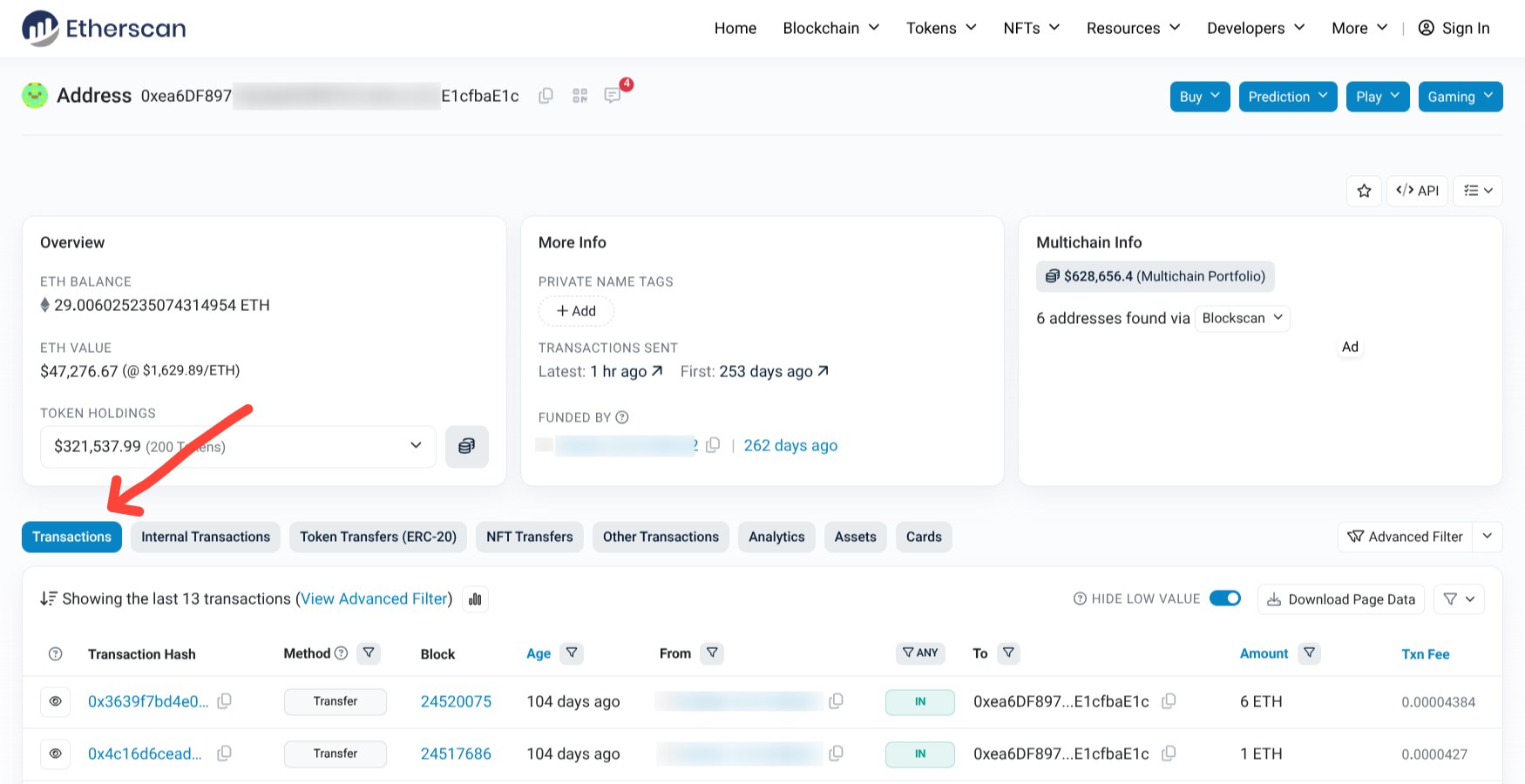

If you are sending a native asset like ETH, AVAX, BNB, or HYPE, check where the incoming transfer appears. If it shows up under Transactions, you are probably fine. But if the movement is in the Internal Transactions or Internal Transfers tab, that is already a contract-based scenario.

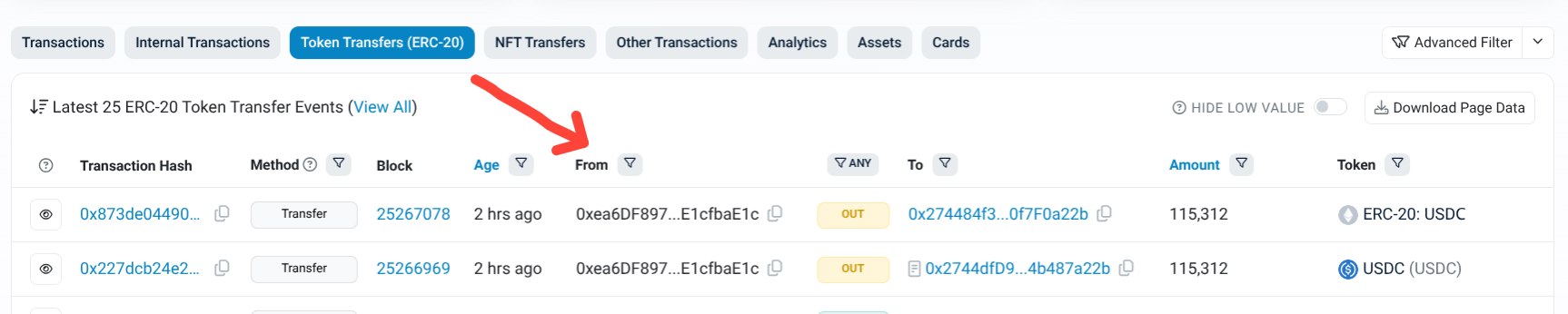

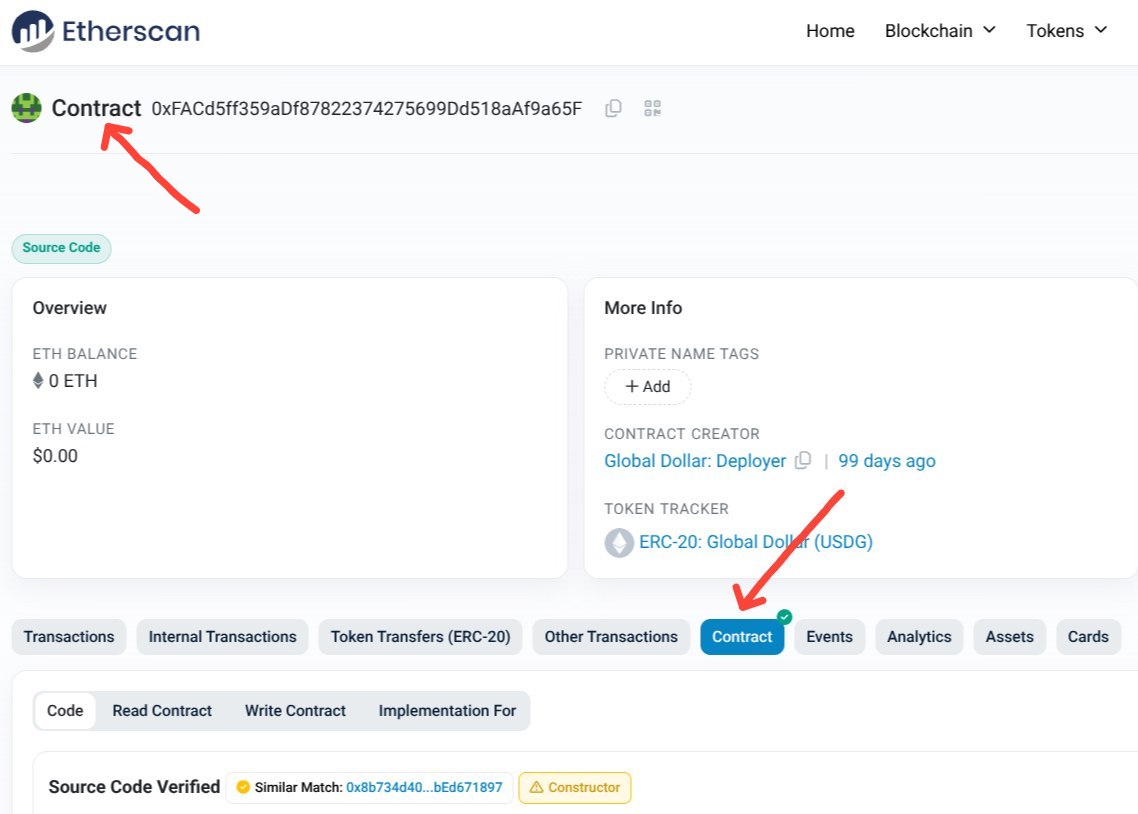

If you are sending an ERC-20 token, open Token Transfers and look at the From field. Visit the address listed there. In Etherscan and similar explorers, smart contracts usually have a Contract tab, verified code, a contract name, or a label. The address may also be tagged as Contract, Bridge, Router, Proxy, Safe, Vault, EntryPoint, Settlement, and so on.

All of this is only visible once a transaction already exists. So before sending a meaningful amount from a new platform, make a small test transfer to yourself first and check whether it came from a smart contract address. If it did not, subsequent transfers from that platform will most likely go through as ordinary transactions or token transfers.

There are also cases where you can spot a smart contract send in advance. The most obvious one is when your wallet lets you pay gas in stablecoins. Without smart contract logic, that is not possible.

One more useful warning sign: if you withdrew funds from an app through a bridge, the sender in the destination network may be a bridge contract or bridge-related infrastructure, not your own EOA.

What Can Happen If You Send from a Smart Contract

The first possibility: the transfer gets processed automatically. A transfer coming from a smart contract does not have to be a problem in itself. Many well-known, trusted contracts are whitelisted by exchanges and swap services, and automated deposit scanners can handle these transfers correctly.

The second possibility: the deposit is not processed automatically, but can be found and handled manually. That said, the credit may not arrive as quickly as you would like, since safe manual processing requires a careful review of the smart contract and the internal structure of the transaction.

A user on Bitcointalk recently shared that HTX gave them a 40-business-day timeline to manually credit 15,759 USDT sent from Polymarket.

The third possibility: after reviewing the transaction, the recipient decides the risks are too high and declines to credit the tokens. In that case, they may return the funds to you.

Finally, there is a fourth possibility: the funds reach the recipient, but the smart contract prevents the recipient from using or moving the tokens in the expected way. In that case, even a refund may be impossible - not because the recipient is dishonest, but because of how the sender's smart contract is structured.

That is exactly why, before your first transfer to an exchange or swap service, it is worth taking a moment to figure out who the actual on-chain sender will be.

If you are unsure whether the transaction will be a plain transfer from your own address, find a previous outgoing transaction in your history and confirm in the block explorer that it did not originate from a smart contract. If there is no transaction history to check, send a test amount first to make sure everything goes through smoothly.

At rabbit.io, even if you make a mistake and accidentally send us crypto assets from a smart contract, rest assured that we will do everything in our power to process the transfer as quickly as possible - or, in the worst case, return the funds to you.