Crypto's Transparency Narrative Is Gaining Momentum

Yesterday, I wrote that Hyperliquid's claim about onchain exchanges being more transparent than exchanges with closed internal ledgers could become a turning point in how the crypto industry is perceived. And it seems I'm not the only one thinking along those lines. The next wave of this narrative arrived almost immediately.

Today, Binance Research published a tweet highlighting the same issue, but from a different angle.

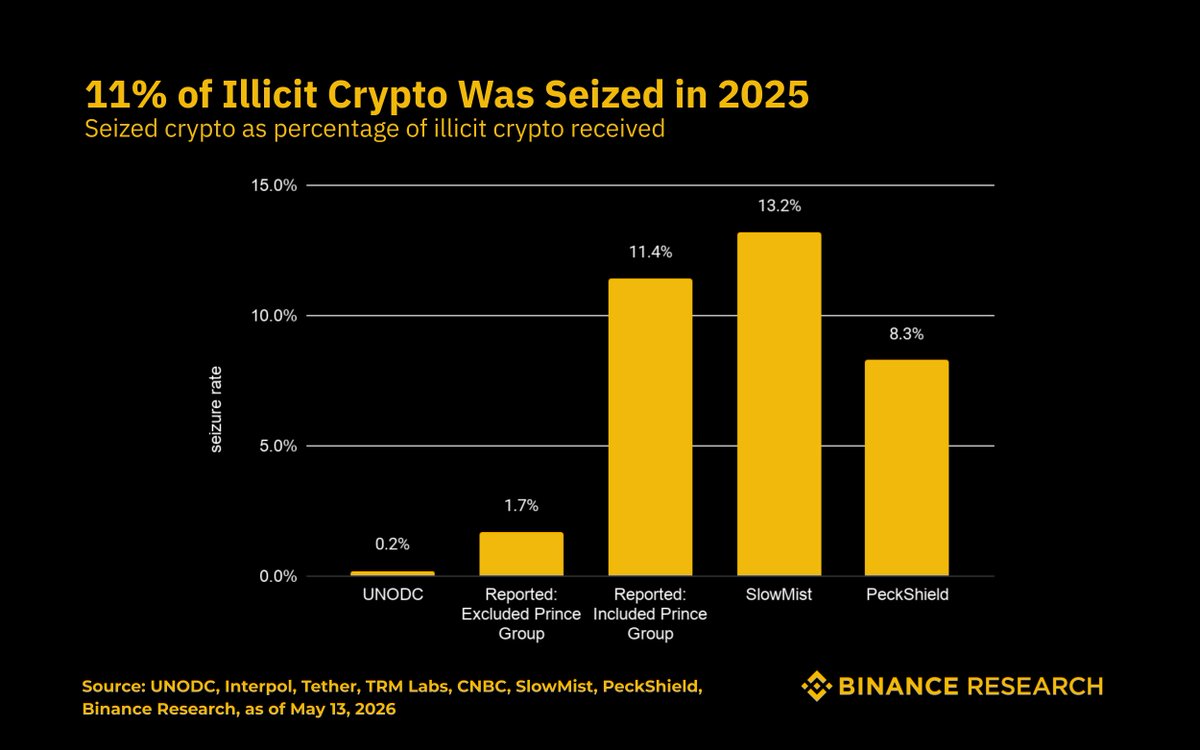

Their post focuses on the idea that cryptocurrency is no longer a safe haven for illicit financial activity. They cite a rather striking statistic: in 2025, law enforcement agencies managed to seize roughly 11% of the total volume of criminal crypto transactions. To put that into perspective, that's 55 times higher than the recovery rate for stolen funds moved through traditional financial channels. And these are not vague estimates from some analytics firm - they are hard figures based on publicly documented operations involving Tether, Interpol, and the T3 Financial Crime Unit.

(By the way, T3 FCU is the joint initiative created by TRON, Tether, and TRM Labs - the same group that reported just days ago that it had frozen $450 million worth of illicit assets worldwide.)

In other words, the message is simple: blockchain has become too transparent - and too risky - for effective money laundering.

What's interesting here is that the emphasis is not on the properties of cryptocurrencies themselves, but on the willingness of crypto-related organizations to enforce freezes and restrictions. From the perspective of the average crypto enthusiast, freezes are obviously seen as a negative. Nobody likes them - and we at rabbit.io don't like them either. But in situations like this, even such measures end up benefiting the crypto industry by demonstrating just how transparent and clean it has become compared to traditional finance.