Are We the Owners of Our Cryptocurrency?

Recently, a client of Rabbit Swap encountered trouble while trying to exchange Bitcoin for another cryptocurrency. They got an address from our liquidity provider for the Bitcoin transfer but mistakenly sent Bitcoin SV (BSV) instead. Upon realizing the error, the client requested the return of the BSV. Technically, this was possible because a private key for a Bitcoin address can also access coins in Bitcoin forks, such as BSV. However, the liquidity provider declined, citing a lack of operational compatibility with the BSV blockchain and no access to its funds.

We explained to the liquidity provider that accessing the BSV would simply require importing the Bitcoin private key (or its corresponding seed phrase) into a wallet that supports BSV. Yet, the provider hesitated. They believed Craig Wright, BSV’s creator, to be a fraud and distrusted all wallets associated with this blockchain. Therefore, they were not willing to input their seed phrase into such wallets, as it granted access to their Bitcoin addresses. These addresses were actively used for swaps, and they did not want to jeopardize their security.

The client argued that cryptocurrency ownership comes down to possession of the private key. If funds were accidentally sent, the key holder had no rightful claim to them and was obligated to return the assets.

Both perspectives made sense. This raised the fundamental question: does having a private key make someone the owner of the associated cryptocurrency? From this flowed deeper inquiries:

- What does it mean to “own” cryptocurrency?

- Can cryptocurrency truly belong to anyone?

- Do traditional property concepts even apply to cryptocurrency?

What Is Ownership?

A glance at the Wikipedia article on “Ownership” reveals that there are many models and types of ownership which vary across societies and traditions. Ownership depends entirely on social agreements.

For instance, companies sell certificates granting ownership of plots on the Moon. Does holding such a certificate mean you own lunar land? Could you prohibit astronauts from trespassing? Only if they accept the rules set by the certificate’s issuer.

To our liquidity provider, the Bitcoin SV blockchain was akin to such a certificate — a set of symbols with no practical meaning to them. Transactions outside the Bitcoin blockchain didn’t align with the provider’s accepted rules. Forcing them to adhere to another set of rules seemed unreasonable.

Some rules are subordinate to others. For instance, if a group of friends is playing basketball on the street and the ball accidentally rolls over to a passerby who is not part of the game, that passerby is not obligated to follow the game’s rules. However, they also cannot keep the ball for themselves — they are expected to return it to the players.

Our client argued that the cryptocurrency had accidentally ended up with the liquidity provider, and according to general rules of property ownership, it should be returned. However, the general principles of ownership are difficult to apply to cryptocurrency, and here’s why.

Private Key: Ownership Certificate or Encryption Tool?

In blockchain ecosystems, private keys grant control over cryptocurrency. Superficially, this seems straightforward:

- My private key is my tool for transactions.

- Therefore, assets controlled by my key are my property.

But in what sense is the private key truly “mine”? It’s “mine” in the same way my language, hometown, or friends are — they’re connected to me, but not exclusively. Others can lay equal claim.

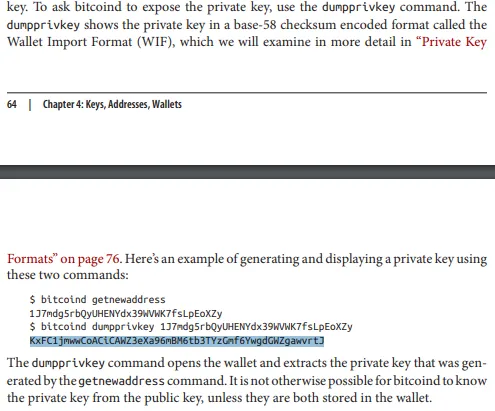

Andreas Antonopoulos published in Mastering Bitcoin some real private keys.

Here you can see the private key for the address 1J7m…oXZy. Can we say that any coins sent to this address would become yours? Hardly. It’s almost certain that specialized draining bots are already monitoring all such addresses. If anything is sent there, the fastest bot will immediately transfer it to another address.

Modern users rarely interact directly with private keys, relying instead on seed phrases — mnemonic representations of keys comprising 12 to 24 words. However, simplistic seed phrases (e.g., easily guessed “brain wallets”) are vulnerable to theft. Whoever’s bot acts first becomes the de facto “owner.”

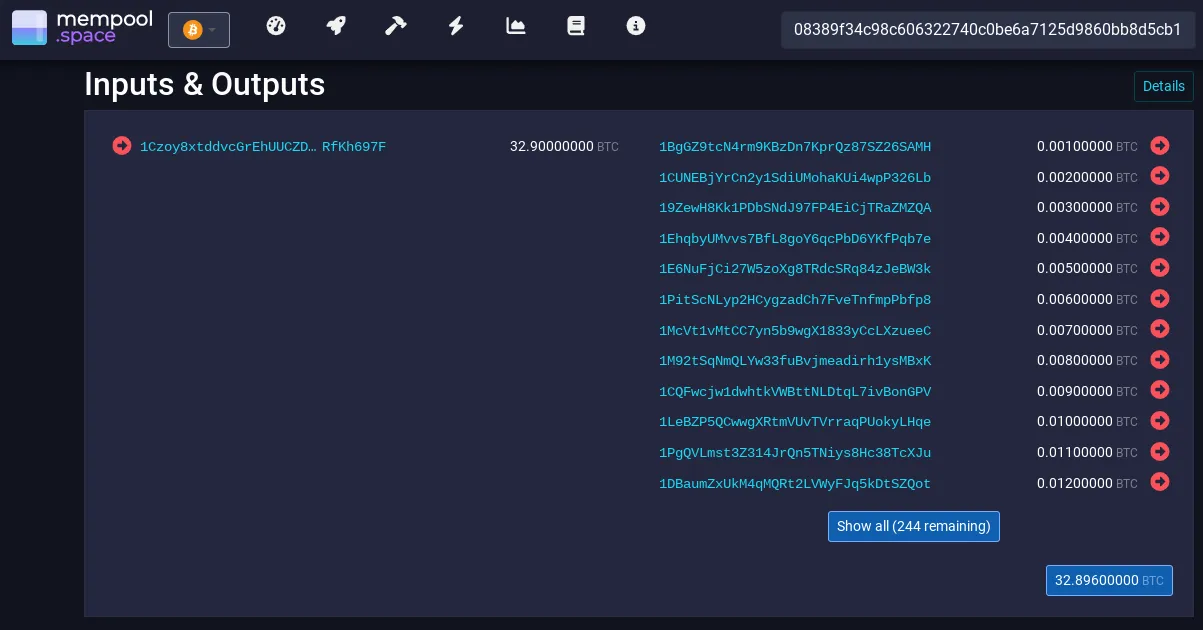

On January 15, 2015, an unknown enthusiast created a puzzle transaction in the Bitcoin blockchain.

In this transaction, Bitcoin was sent to 256 addresses:

- 0.001 BTC to the first address,

- 0.002 BTC to the second address,

- …

- 0.256 BTC to the final address.

The private key for the first address was very easy to guess (it was a known brain wallet). The private key for each subsequent address was twice as difficult to find as the previous one, with the reward increasing by 0.001 BTC each time.

The first 20 private keys were found immediately after the puzzle transaction was broadcast. The Bitcoins from these addresses were transferred in the same block as the original transaction.

The 21st key was found an hour later. The 22nd key took three hours, and the 23rd took 25 hours.

Nearly a decade later, the first 66 outputs of the puzzle transaction are spent, along with some outputs from the 70th to the 130th. The most recent of these was spent on September 23, 2024. This means that it took someone 9 years, 9 months, and 8 days to find one of these keys. Despite the difficulty, someone completed the task and claimed the 0.13 BTC reward.

Undoubtedly, the work continues, and someone is still trying to find the remaining keys from that transaction right now. Moreover, it’s likely that all these keys remain in the possession of the person who originally sent the transaction. But does this person actually own the coins? If they do, are those finding the keys and transferring the funds stealing from the owner? Hard to say. It’s impossible to determine whether different individuals are using the keys for various outputs of the latter transactions, or if it’s all the work of a single person (possibly even the original sender of the transaction).

If two people know the same private key, Bitcoin network nodes do not distinguish between them. Nodes that verify transactions do not ask for a receipt or contract to confirm the legitimacy of cryptocurrency ownership. They treat the private key not as a certificate of ownership but as an encryption tool. If the cryptographic signature is valid, the transaction is deemed legitimate, regardless of which of the potentially many people who know the private key signed it.

Broadly speaking, the concept of ‘ownership’ of cryptocurrency is only relevant at the moment a transaction is created. As the transaction propagates through the cryptocurrency network, nodes check whether the sender has the authority to manage the cryptocurrency. Outside of a transaction, it is inaccurate to speak of ownership of cryptocurrency.

If our liquidity provider neither used the private key in the Bitcoin SV network nor intended to use it, it would be incorrect to claim that they had taken possession of cryptocurrency in that network.

Mining Private Keys

There are programs that allow users to generate aesthetically pleasing cryptocurrency addresses. In the Bitcoin network, popular examples of such tools include VanityGen, VanitySearch, VanityBTC, and others. When you run these programs, you specify a sequence of characters that you want to see in the address, and the program starts generating private keys and checking whether a randomly created private key matches an address containing the desired character sequence.

But what happens to the addresses discarded as unsuitable? Why not compile a database of ‘private key — public address’ pairs and let a draining bot manage this database? It’s entirely possible that someone, at some point, might randomly generate the exact same private key and begin using the corresponding address. If coins are sent to that address, you could take control of them.

Some might say that this is unethical because the address belongs to someone else. But does it really? If you were the first to generate it, can you not claim it as yours?

There’s a ‘mining’ pool called the Large Bitcoin Collider, which unites the efforts of individuals generating Bitcoin private keys on an industrial scale. The pool’s goal is to consolidate all these keys into a single database and monitor whether any non-empty addresses, whose keys are in this database, appear in the blockchain. If such an address is found, the pool redistributes the Bitcoin it contains proportionally to the contributions of each participant in building the database.

The creators of the pool are transparent about their activities. They argue that their work strictly adheres to Bitcoin’s existing consensus rules. A similar discourse emerged in the Ethereum community in 2016, when a hacker drained 3.6 million ETH from a smart contract and demanded that the Ethereum Foundation stop calling them a thief because his action was fully compliant with United States criminal and tort law, as well as the terms of The DAO.

Legally, there was no counterargument to this claim. The only way to return the lost funds was to reverse the transaction in the blockchain, which the Ethereum Foundation ultimately did.

In the case of private key mining, too, there are no legal grounds to prohibit this activity. If people want to do this, they do. The probability of generating a private key already created by someone else is infinitesimally small. However, the longer this mining continues, the higher that probability will become.

This introduces another dimension to our client’s situation, where Bitcoin SV was mistakenly sent instead of Bitcoin. Even if the private key were presented and the coins transferred to another address, no one could be certain that the transfer was made by our liquidity provider.

Is Cryptocurrency Ownership Impossible?

Many jurisdictions recognize cryptocurrency as property, but contradictions remain. Multiple unrelated individuals can control the same funds if they all know the same private key. A unique solution is offered in Russia: cryptocurrency ownership is legally recognized only if declared in advance. Whoever first declares their claim is considered the owner.

Knowing this, one might suggest to Craig Wright, who claims to be Satoshi Nakamoto, that he should file a declaration with the Russian authorities asserting that the Bitcoins in Satoshi’s addresses belong to him.

However, the real Satoshi, if they wanted to ridicule Craig Wright, could send a small amount from one of these addresses to an address flagged for involvement in terrorism. Craig Wright would then have to prove that he is not behind such activities.

Ultimately, cryptocurrency’s permissionless nature conflicts with traditional property concepts. Key holders may not always control the cryptocurrency.

Practical Implications

It’s worth returning to the analogy we used at the very beginning: people playing basketball on the street.

One of them brings a ball from home. That ball belongs to them, and its owner can reasonably expect that no one will take it away against their will. After all, seizing someone else’s property without the owner’s consent goes against established societal rules.

But once the owner uses the ball in the game, the rules change entirely. The game allows players to take possession of another’s ball. Anyone can attempt to take the ball from an opponent, and this is considered a completely legitimate action.

When we convert our savings into cryptocurrency, we enter a game where the rules permit anyone with a private key to our address to control our cryptocurrency. No one can verify whether it is us presenting the private key or someone else.

The likelihood that someone accidentally or deliberately guesses our private key is minuscule, but it’s not zero. The more popular a cryptocurrency becomes, the more people will want to join pools like the Large Bitcoin Collider.

This issue is especially relevant for blockchains like:

- Bitcoin (due to its popularity, as well as the fact that finding the private key for an address in Bitcoin automatically provides access to similar addresses in Bitcoin forks like Bitcoin Cash, Bitcoin SV, and others);

- Ethereum (access to an address here not only grants control over all its forks, such as Ethereum Classic, EthereumPoW, etc., but also extends to other EVM-compatible blockchains, such as BNB Smart Chain and Rootstock, as well as Layer 2 networks like Optimism, Arbitrum, and others).

To mitigate this risk, you can use multi-signature addresses or store funds in smart contracts with complex withdrawal conditions. However, the simplest method is to distribute your savings across multiple addresses that are not tied to the same seed phrase.

In Bitcoin, Lightning channels can serve this purpose. This approach also has practical benefits: the more channels the network has, the higher its throughput. By doing this, you not only protect yourself but also contribute to the development of decentralized money.

—

In the case of the Rabbit Swap client who accidentally sent BSV instead of BTC, the story had a happy ending. All our partners are professionals, and they fully understand that their decisions directly impact the well-being of clients. Once all other swaps involving the addresses associated with our liquidity provider’s seed phrase were completed and there was no longer a risk of financial loss from a potential leak of private keys, the provider entered the seed phrase into a wallet that supports BSV and transferred the coins back to the sender.